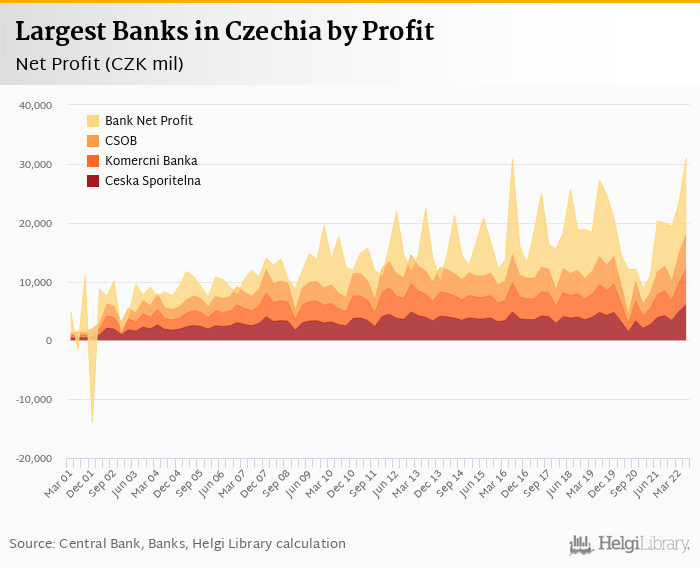

Czech banks increased net profit 53.7% yoy to CZK 31,133 mil in the second quarter of 2022 and generated ROE of 18.2%.

Operating income rose 26.3%, cost to income dropped to 40.3% and banks' share of bad loans fell to 2.27%.

Ceska Sporitelna generated the biggest profit while Max banka produced the biggest loss in 2Q2022.

Czech banks reported a net profit of CZK 31,133 mil in the second quarter of 2022, up 53.7% when compared to previous year. This implies ROE of 18.2% in 2Q2022. In the last twelve months, profits rose 80.7% yoy to CZK 93,891 mil and ROE reached 13.5%.

Ceska Sporitelna generated the largest net profit in the last quarter (CZK 6,084 mil) followed by CSOB and Komercni Banka. At the other end of the scale was Max banka with a reported loss of CZK 38.4 mil:

Revenues increased 26.3% yoy to CZK 58,487 mil in the second quarter of 2022:

| 2Q2021 | 2Q2022 | Change | 1-6/2021 | 1-6/2022 | Change | |

| Revenues | 46,318 | 58,487 | 26.3% | 87,516 | 117,698 | 34.5% |

| Net Interest Income | 29,346 | 43,482 | 48.2% | 58,644 | 85,314 | 45.5% |

| Net Fee Income | 9,031 | 9,453 | 4.67% | 17,116 | 19,329 | 12.9% |

| Other Income | 37,287 | 49,034 | 31.5% | 70,400 | 98,369 | 39.7% |

| Costs | 23,151 | 23,554 | 1.74% | 48,131 | 50,749 | 5.44% |

| Staff Cost | 10,740 | 10,993 | 2.36% | 21,366 | 22,232 | 4.05% |

| Operating Profit | 23,167 | 34,933 | 50.8% | 39,385 | 66,949 | 70.0% |

| Cost of Risk | -0.015% | -0.078% | -0.063 pp | 1,804% | 1,776% | -28.0 pp |

| Pre-Tax Profit | 24,493 | 36,867 | 50.5% | 37,501 | 65,337 | 74.2% |

| Net Profit Bank | 20,258 | 31,133 | 53.7% | 31,063 | 54,610 | 75.8% |

| ROE | 11.8% | 18.2% | 6.42 pp | 9.07% | 16.0% | 6.94 pp |

| NIM | 1.34% | 1.81% | 0.475 pp | 1.85% | 3.88% | 2.02 pp |

| Cost To Income | 50.0% | 40.3% | -9.71 pp | 55.0% | 43.1% | -11.9 pp |

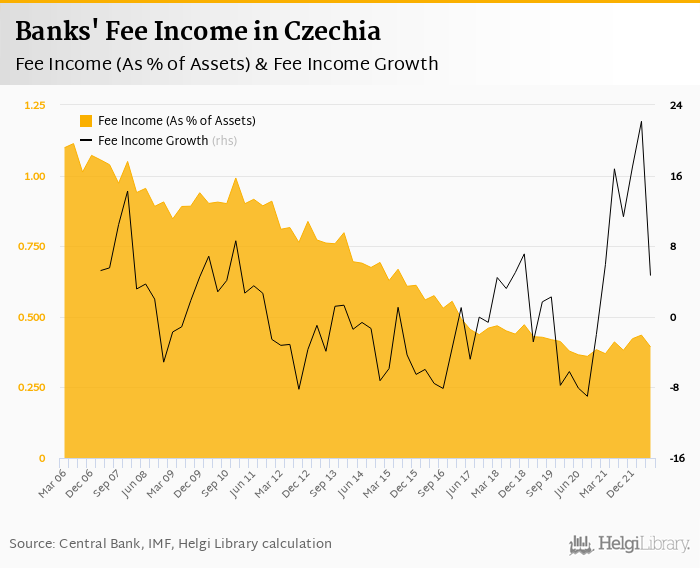

Net interest margin increased 0.475 pp to 1.81% as asset yield grew by 2.42 bp to 4.27% and cost of funding increased by 2.09 bp to 2.64%. Fees added 16.2% to total revenues and increased by 4.67% when compared to last year:

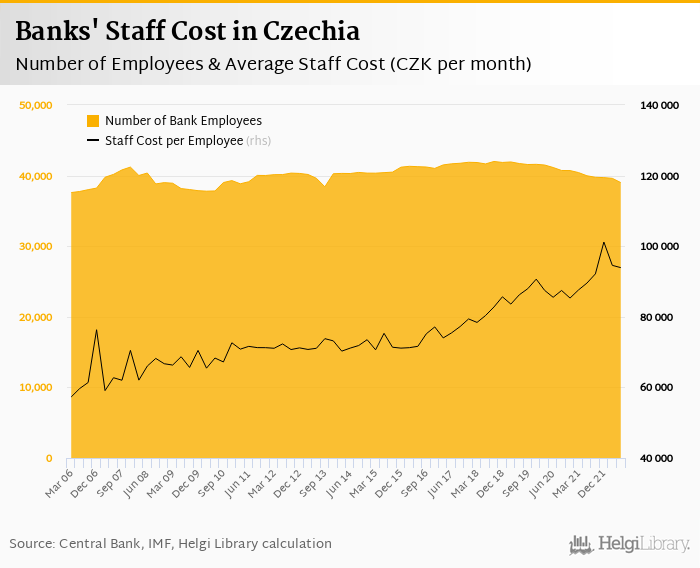

Banks operated with average cost to income of 40.3% in the last quarter as operating costs rose 1.74% yoy. Staff accounted for 46.7% of operating expenditure with a total of 39,012 employees in the sector. Banks paid their staff 4.88% more than last year with the average monthly cost of CZK 93,928 per person:

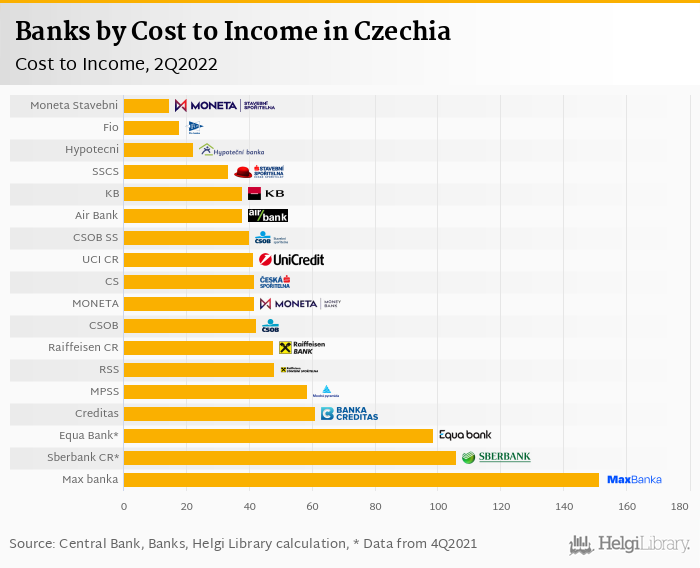

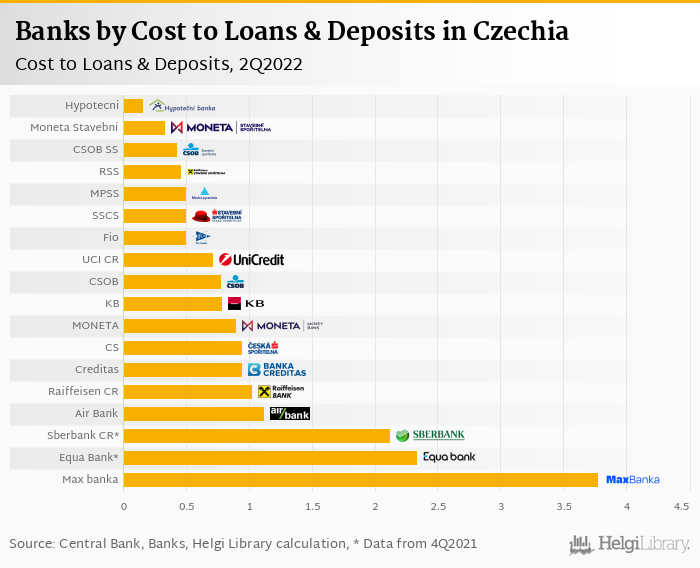

While Moneta Stavebni Sporitelna was the most cost efficient based on the cost to income ratio in the second quarter of 2022 (with 14.6%), Hypotecni Banka operated with the lowest operating costs when compared to a sum of loans and deposits, i.e. when utilization of both assets as well as liabilities is taken into account (0.159%):

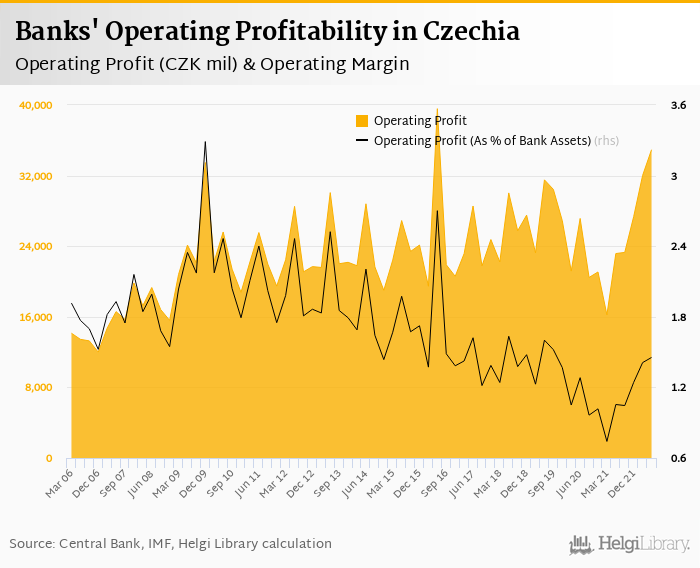

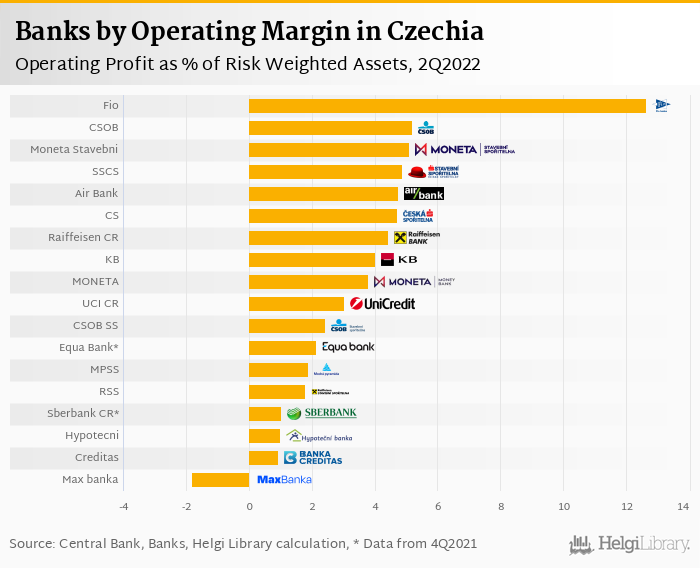

Commercial banks generated operating profit before provisioning of CZK 34,933 mil in the second quarter of 2022, up 50.8% when compared to last year. Ceska Sporitelna generated the largest operating profit in the second quarter of 2022 (CZK 7,332 mil), whilst Fio banka was operating with the highest operating margin when compared with risk weighted assets (12.6%):

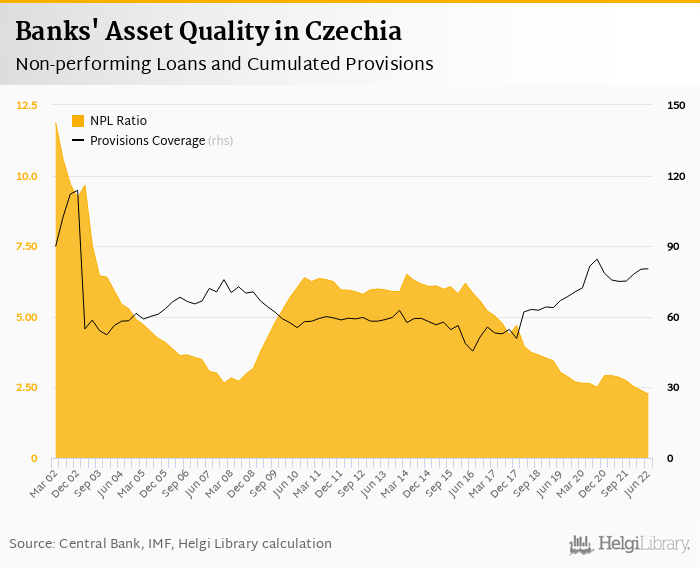

Provisions have "eaten" some -4.63% of operating profit in the second quarter of 2022 as cost of risk reached -0.078% of average loans. The volume of non-performing loans decreased by 15.1% qoq to CZK 89.8 bil and represented 2.27% of total loans at the end of June. Provisions covered 80.4% of NPLs, up from 75.0% a year ago:

Within the sector, Fio banka had to create the most provisions in the second quarter of 2022 relative to its loans (1.40%) and Moneta Stavebni Sporitelna the least (-1.98%). In terms of overall asset quality, Fio banka was operating with the highest share of non-performing loans, some 8.79% of customer loans at the end of June:

The three largest banks created 52.7% of sector's total profit in the second quarter of 2022, down when compared to 54.4% seen three years ago. In terms of revenue and operating profit, the trio generated 57.6% and 57.1% of the total:

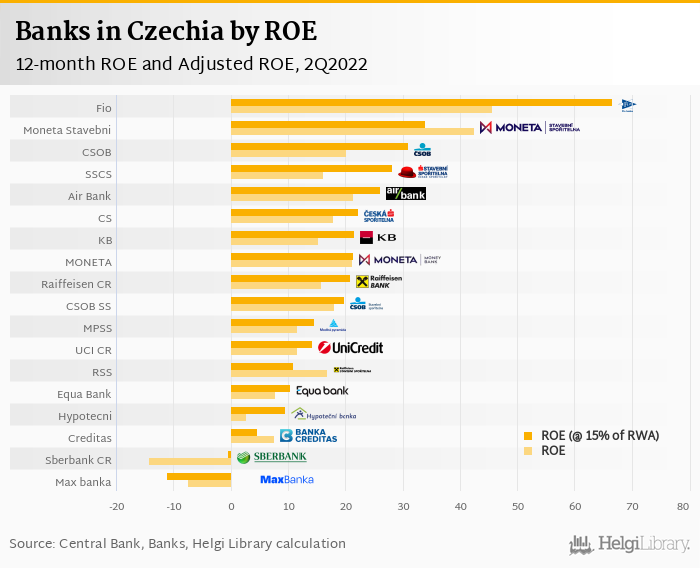

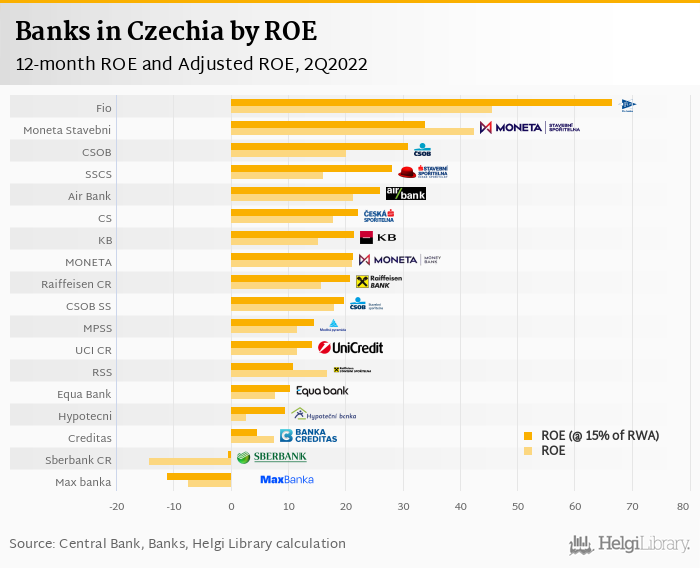

Overall, Czech banks generated its shareholders an annualized return on equity of 18.2% in the second quarter of 2022 and 13.5% return in the last four quarters. When equity "adjusted" to 15% of risk-weighted assets, the return on equity would have reached 29.3% in 2Q2022 and 22.6% in the last twelve months.

Fio banka generated its shareholders the highest return in the last quarter (ROE of 45.6%) followed by Moneta Stavebni Sporitelna (42.5%) and Air Bank (21.4%). When adjusted for the same level of equity (i.e. 15% of RWA), Fio banka, Moneta Stavebni Sporitelna and CSOB would have made it to the top of the list:

Loans increased by 0.834% qoq to CZK 3,958 bil during the second quarter of 2022. This implies an annual growth rate of 6.93% in the last 12 months:

Mortgage loans grew 8.80% yoy in the last 12 months and were up 0.673% qoq in the last quarter. At the end of June, mortgages formed 41.4% of total loans. Consumer loans increased 0.846% qoq (up 6.44% yoy) and represented 11.7% of total bank loans while corporate loans fell 0.112% qoq and were up 7.71% yoy to CZK 1,221 bil (or 30.8% of loans).

Raiffeisen Stavebni Sporitelna has grown the fastest in relative terms within the last quarter (19.5%% qoq), followed by Banka Creditas and Stavebni Sporitelna Ceske Sporitelny. In absolute terms, however, Ceska Sporitelna the largest piece of the pie when compared to the previous quarter (CZK 24,835 mil or 75.9% of the market net increase) followed by CSOB and Komercni Banka:

Overall, CSOB remains the largest lender with 27.4% of the market followed by Ceska Sporitelna with a 21.9% market share and Komercni Banka (19.1%). At the end of June 2022, most of CSOB's loans came from residential mortgages (46.1% of total). Corporate loans formed 30.8% and consumer loans represented a further 3.34% of the total loan book:

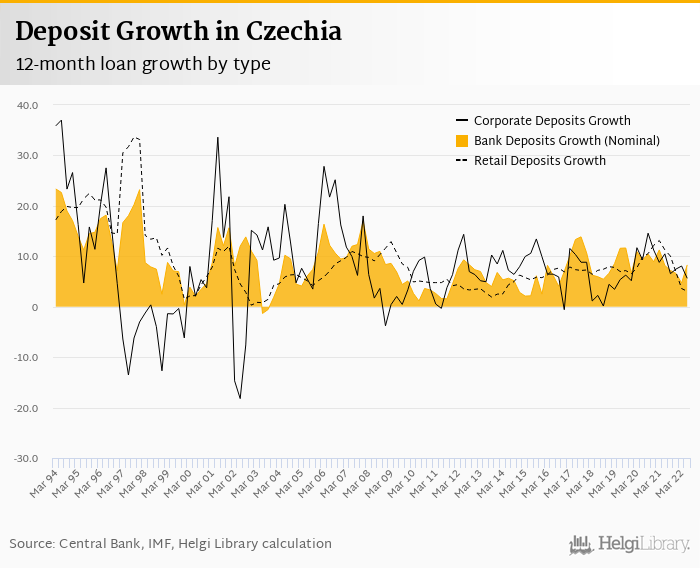

Customer deposits increased 2.73% qoq to CZK 6,340 bil during the second quarter of 2022. This means an annual growth rate of 8.29%, which is above the average growth of 7.50% we have seen in deposits in the last decade:

As partly seen above, households deposits grew 1.28% qoq and 3.05% yoy in the last 12 months and represented 52.4% of total customer deposits at the end of June 2022. Corporate deposits decreased by 0.868% qoq (or 5.63% yoy) and made up 20.9% of total.

Banka Creditas appears to have grown the fastest in deposits in relative terms last quarter compared to the next bunch of Czech banks (22.6% qoq), followed by CSOB and Raiffeisenbank Czech Republic. In absolute terms, when compared to the previous quarter, however, most new deposits went to Komercni Banka (CZK 52,350 mil) followed by CSOB and Raiffeisenbank Czech Republic:

Overall, CSOB is the largest deposit collector with a 22.1% market share followed by Ceska Sporitelna (21.2%) and Komercni Banka (17.4%):

At the end of June 2022, customer deposits in Czechia reached 94.5% of GDP, up from 75.3% seen a decade ago. Loan to deposit ratio accounted for 62.4% in Czechia at the end of second quarter of 2022, down from 63.2% a year ago and 76.1% in 2012. When comparing only household loans and deposits, the ratio was 63.2% at the end of June 2022:

Czech banks operated with capital adequacy ratio of 21.6% at the end of the second quarter of 2022, down 3.00 bp when compared to the same period of last year. Sector's Tier 1 ratio reached 20.9% and equity accounted for 16.5% of loans. This is up 3.11 bp and down %down bp when compared to five years ago.

Hypotecni Banka reported the highest capital adequacy ratio (45.3%) followed by Max banka (30.2%) and Stavebni Sporitelna Ceske Sporitelny. Moneta Stavebni Sporitelna and Raiffeisen Stavebni Sporitelna managed to operate with relatively low capital ratios of 13.1% and 16.4%, respectively:

Fio banka achieved the highest ROE in the last three years (34.7%) followed by Moneta Stavebni Sporitelna (20.8%) and Air Bank (15.6%). When adjusted to the same level of capital (15% of risk-weighted assets), Fio banka would be the most profitable with a ROE of 66.6% in the last twelve months:

Helgi Library

Helgi Library