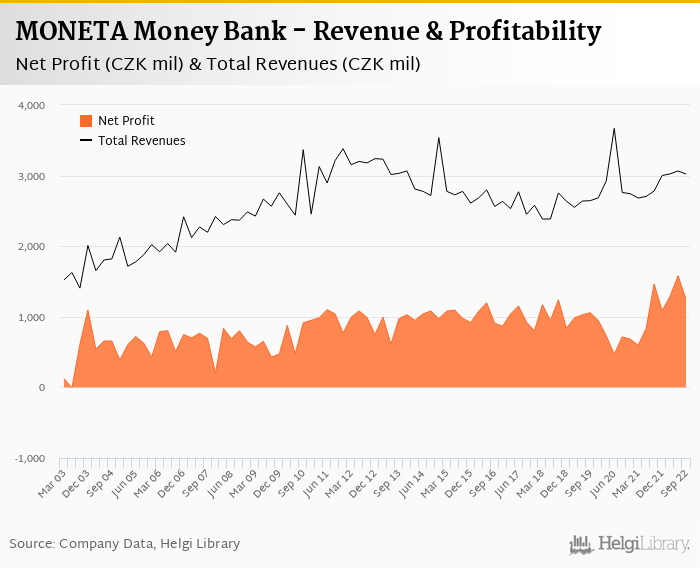

MONETA Money Bank decreased its net profit 14.7% to CZK 1,251 mil in 3Q2022 and generated ROE of 17.0%.

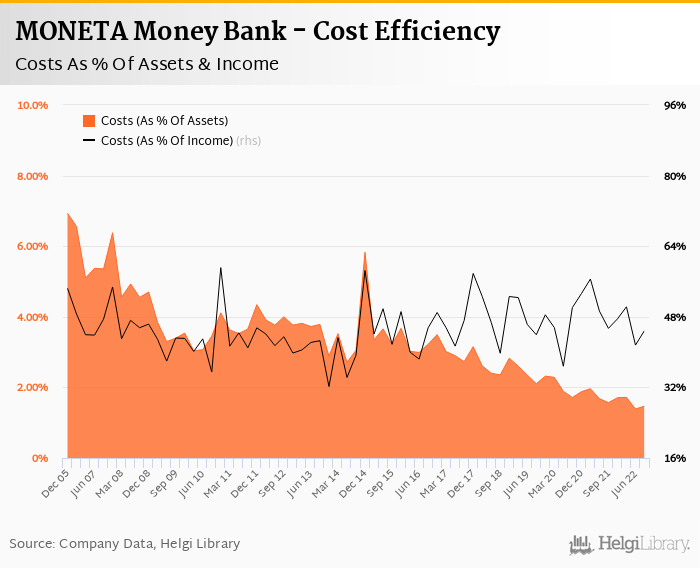

Revenues increased 8.67% yoy and cost rose 7.45%, so cost to income decreased to 44.9%

Bad loans fell to 1.40% of total loans and cost of risk amounted 0.186%.

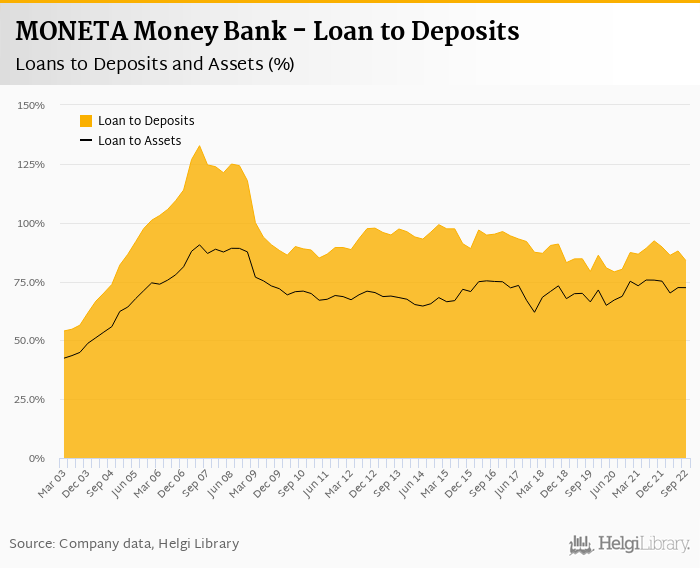

Loan to deposit ratio decreased to 83.8% and capital adequacy decreased to 17.0%

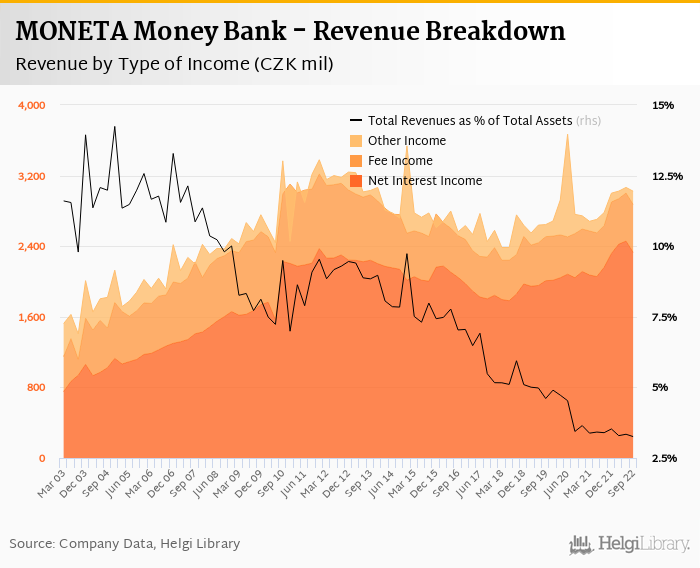

Revenues increased 8.67% yoy to CZK 3,022 mil in the third quarter of 2022. Net interest income rose 7.68% yoy and formed 77.0% of total with net interest margin decreasing 0.164 pp to 2.52% of total assets. The reduction in margin is a difference compared Komercni Banka or Ceska Sporitelnas' performance that quarter. Fee income grew impressive 14.8% yoy and added a further 18.0% to total revenue. When compared to three years ago, revenues were up 14.3%:

Average asset yield was 4.34% in the third quarter of 2022 (up from 2.95% a year ago) while cost of funding amounted to 1.97% in 3Q2022 (up from 0.296%).

Costs increased by 7.45% yoy and the bank operated with average cost to income of 44.9% in the last quarter. Staff cost rose 4.62% as the bank employed 2,799 persons (down 7.26% yoy) and paid CZK 78,242 per person per month including social and health care insurance cost:

MONETA Money Bank's customer loans grew 1.09% qoq and 8.56% yoy in the third quarter of 2022 while customer deposit growth amounted to impressive 6.09% qoq and 19.5% yoy. That’s compared to average of 22.6% and 21.0% average annual growth seen in the last three years.

At the end of third quarter of 2022, MONETA Money Bank's loans accounted for 83.8% of total deposits and 72.4% of total assets.

Retail loans grew 1.06% qoq and were 9.32% up yoy. They accounted for 69.3% of the loan book at the end of the third quarter of 2022 while corporate loans increased 1.28% qoq and 9.02% yoy, respectively. Mortgages represented 49.3% of the MONETA Money Bank's loan book, consumer loans added a further 19.9% and corporate loans formed 31.3% of total loans:

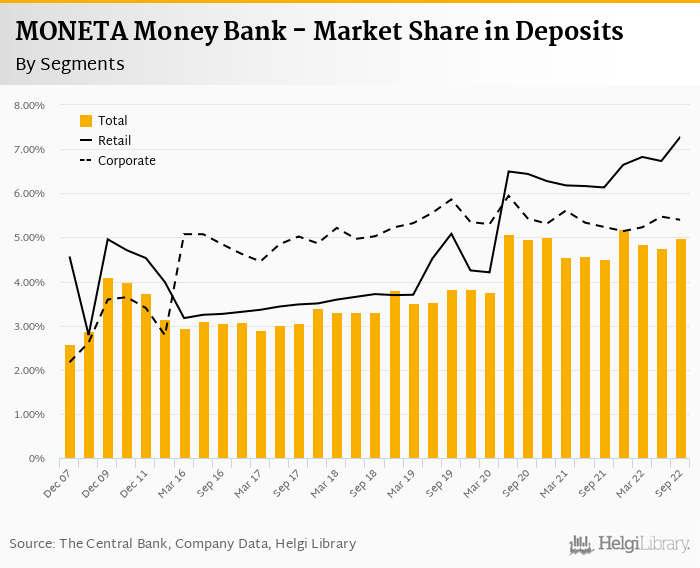

We estimate that MONETA Money Bank has gained 0.058 pp market share in the last twelve months in terms of loans (holding 6.61% of the market at the end of 3Q2022). On the funding side, the bank seems to have gained 0.486 pp and held 5.00% of the deposit market. The largest gains so far this year have been seen in residential mortgage lending and household deposits, which could partly explain smaller increase in margin improvement when compared to bank's larger peers:

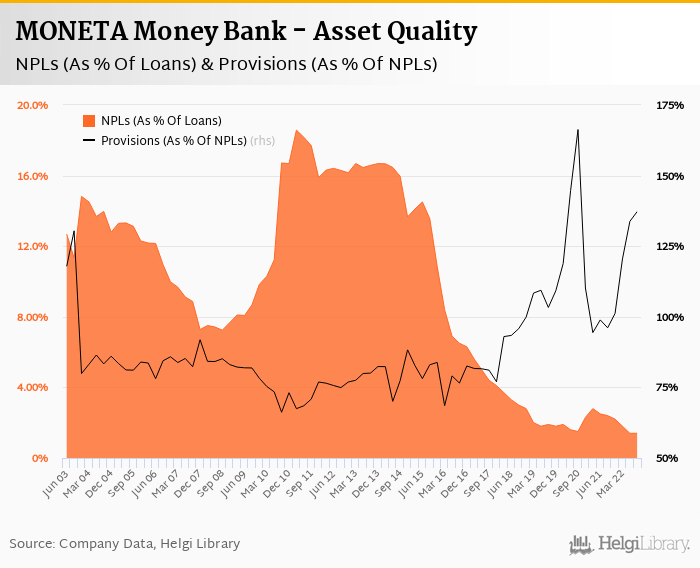

MONETA Money Bank's non-performing loans reached 1.40% of total loans, down from 2.40% when compared to the previous year. Provisions covered some 137% of NPLs at the end of the third quarter of 2022, up from 96.1% for the previous year.

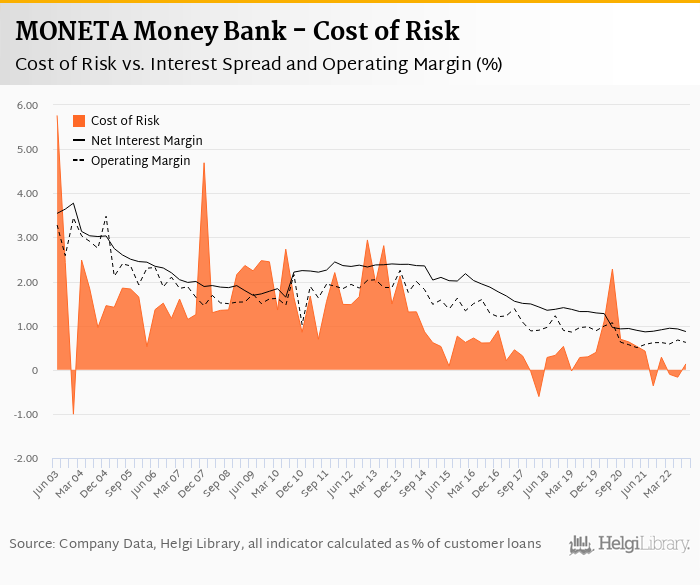

Provisions have "eaten" some 7.44% of operating profit in the third quarter of 2022 as cost of risk reached 0.186% of average loans:

MONETA Money Bank's capital adequacy ratio reached 17.0% in the third quarter of 2022, down from 18.7% for the previous year. The Tier 1 ratio amounted to 14.3% at the end of the third quarter of 2022 while bank equity accounted for 11.2% of loans:

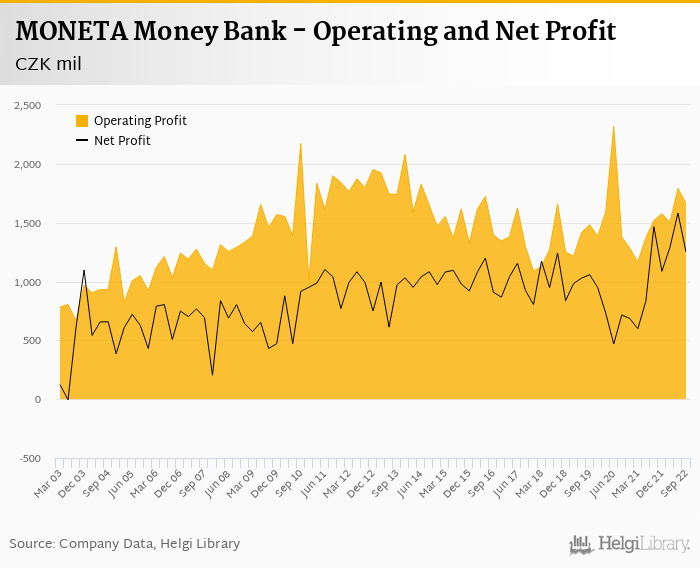

Overall, MONETA Money Bank made a net profit of CZK 1,251 mil in the third quarter of 2022, down 14.7% yoy. The relatively weak result this quarter is due to a one-off release of CZK 299 mil provisions inflating last year's bottom line. On the operating level, bank's profit has risen solid 9.7% yoy.

The net profit implies an annualized return on equity of 17.0%, or 20.2% when equity "adjusted" to 15% of risk-weighted assets:

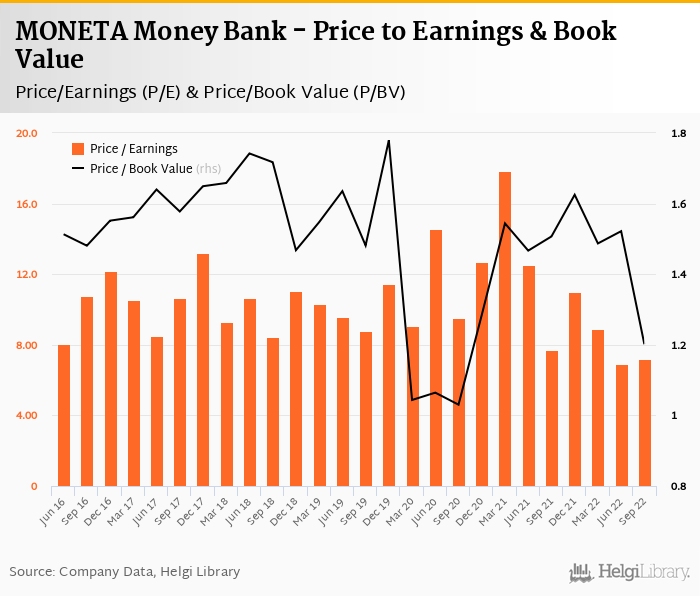

MONETA Money Bank stock depreciated 17.6% in the last third quarter of 2022 and was 3.22% down when compared to three three years ago. This put stock at a 12-month trailing price to earnings of 7.21x and price to book value of 1.20x as of the end of 3Q2022.

Over the previous five years, the PE multiple reached a high of 17.8x in 1Q2021 and a low of 6.92x in 2Q2022 with an average of 10.5x.

Solid set of results when adjusted for the one-off positive effect from a release of provisions last year. Revenue growth was supported by rising interest rates, though somewhat lower when compared to Komercni banka and Ceska Sporitelna. Very good cost control and no major pressure from asset quality deterioration have further supported bank's bottom line. The Bank continues gaining market share in residential mortgages and household deposits.

Interest margin and market share development remain the main key areas to watch for in the coming months apart from the general development on the cost side and overall volume growth.

Helgi Library

Helgi Library