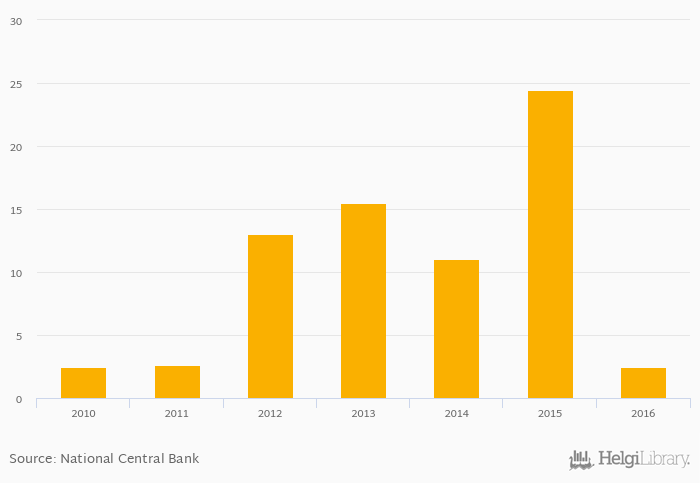

Fee income as a share of bank assets fell 89.9% to 2.46% in Cameroon in 2016, according to the National Central Bank.

Historically, fee income as a share of bank assets in Cameroon reached an all time high of 24.5% in 2015 and an all time low of 2.46% in 2016. When compared to Cameroon's main peers, fee income as a share of bank assets in Central African Republic amounted to 6.29%, 2.89% in Chad, 6.69% in Gabon and 3.08% in Nigeria in 2016.

Cameroon has been ranked 12th within the group of 81 countries we follow in terms of fee income as a share of bank assets, 12 places below the position seen 10 years ago.

| Fee Income (As % of Bank Assets) | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Angola | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.22% | 1.13% | ... | ... | ... | ... | ... | ||||

| Benin | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| Cameroon | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 11.0% | 24.5% | 2.46% | 2.32% | 2.75% | ||||||

| Central African Republic | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 7.68% | 17.1% | 6.29% | 2.97% | 2.32% | ||||||

| Chad | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 3.30% | 3.37% | 2.89% | 2.22% | 2.54% | ||||||

| Congo | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2.21% | 2.39% | 4.37% | 2.28% | 4.21% | ||||||

| Dem. Republic of the Congo | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| Equatorial Guinea | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2.61% | 2.65% | 2.20% | 1.67% | 1.50% | |||||

| Gabon | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4.50% | 8.67% | 6.69% | 2.15% | 2.38% | ||||||

| Niger | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| Nigeria | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2.69% | 3.10% | 3.08% | 0.578% | 0.429% | ||||||

| Sudan | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

Helgi Library

Helgi Library