This report analyses the performance of the Bank for the 3Q2014. You will find all the necessary details regarding volume growth, market share, margin and asset quality development in the Bank.

The key highlights are:

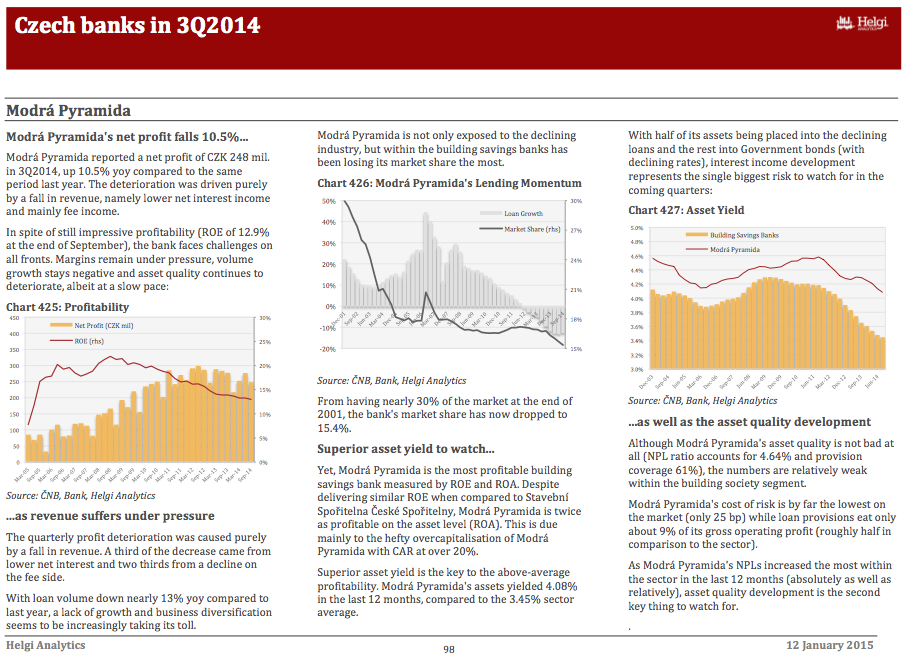

Modrá Pyramida's net profit falls 10.5%...

Modrá Pyramida reported a net profit of CZK 248 mil. in 3Q2014, up 10.5% yoy compared to the same period last year. The deterioration was driven purely by a fall in revenue, namely lower net interest income and mainly fee income.

In spite of still impressive profitability (ROE of 12.9% at the end of September), the bank faces challenges on all fronts. Margins remain under pressure, volume growth stays negative and asset quality continues to deteriorate, albeit at a slow pace:

...as revenue suffers under pressure

The quarterly profit deterioration was caused purely by a fall in revenue. A third of the decrease came from lower net interest and two thirds from a decline on the fee side.

With loan volume down nearly 13% yoy compared to last year, a lack of growth and business diversification seems to be increasingly taking its toll.

Modrá Pyramida is not only exposed to the declining industry, but within the building savings banks has been losing its market share the most.

From having nearly 30% of the market at the end of 2001, the bank's market share has now dropped to 15.4%.

Superior asset yield to watch...

Yet, Modrá Pyramida is the most profitable building savings bank measured by ROE and ROA. Despite delivering similar ROE when compared to Stavební Spořitelna České Spořitelny, Modrá Pyramida is twice as profitable on the asset level (ROA). This is due mainly to the hefty overcapitalisation of Modrá Pyramida with CAR at over 20%.

Superior asset yield is the key to the above-average profitability. Modrá Pyramida's assets yielded 4.08% in the last 12 months, compared to the 3.45% sector average.

With half of its assets being placed into the declining loans and the rest into Government bonds (with declining rates), interest income development represents the single biggest risk to watch for in the coming quarters.

...as well as the asset quality development

Although Modrá Pyramida's asset quality is not bad at all (NPL ratio accounts for 4.64% and provision coverage 61%), the numbers are relatively weak within the building society segment.

Modrá Pyramida's cost of risk is by far the lowest on the market (only 25 bp) while loan provisions eat only about 9% of its gross operating profit (roughly half in comparison to the sector).

As Modrá Pyramida's NPLs increased the most within the sector in the last 12 months (absolutely as well as relatively), asset quality development is the second key thing to watch for.

You will find more details about the bank at www.helgilibrary.com/companies

Helgi Library

Helgi Library