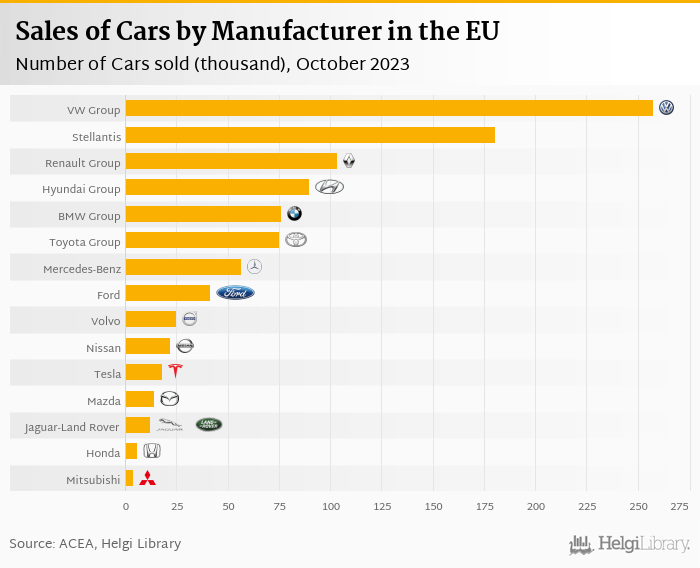

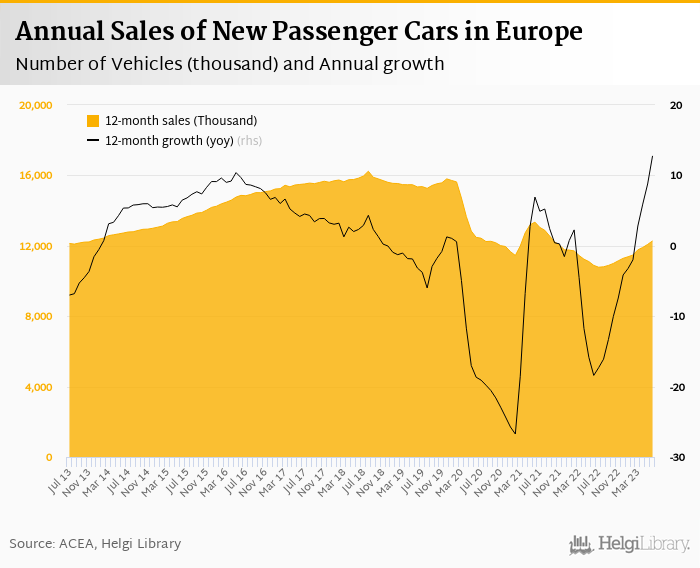

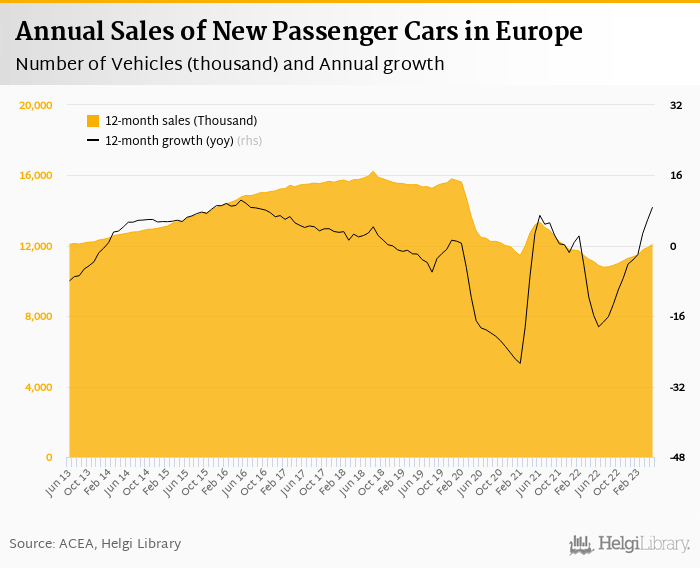

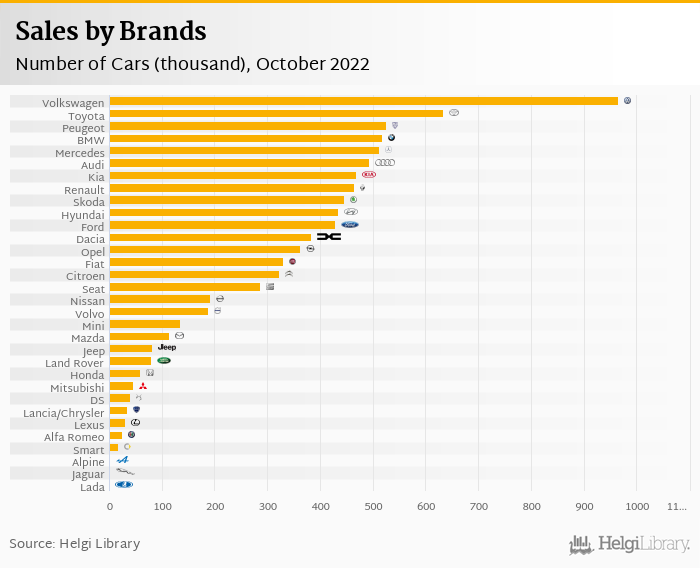

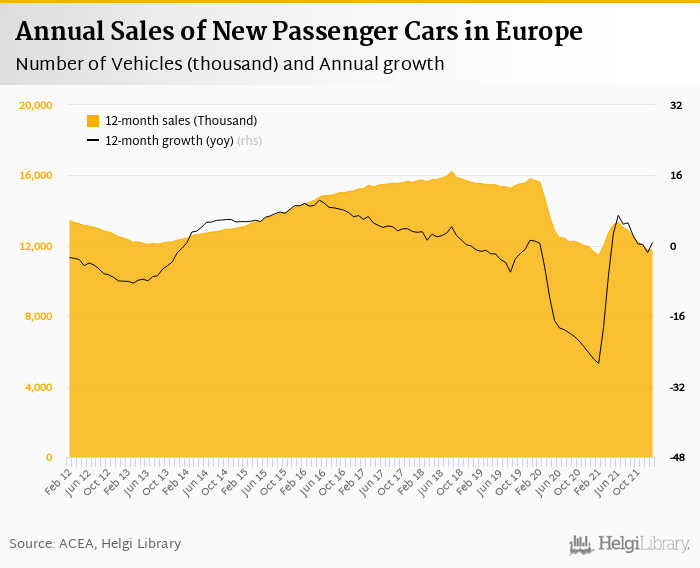

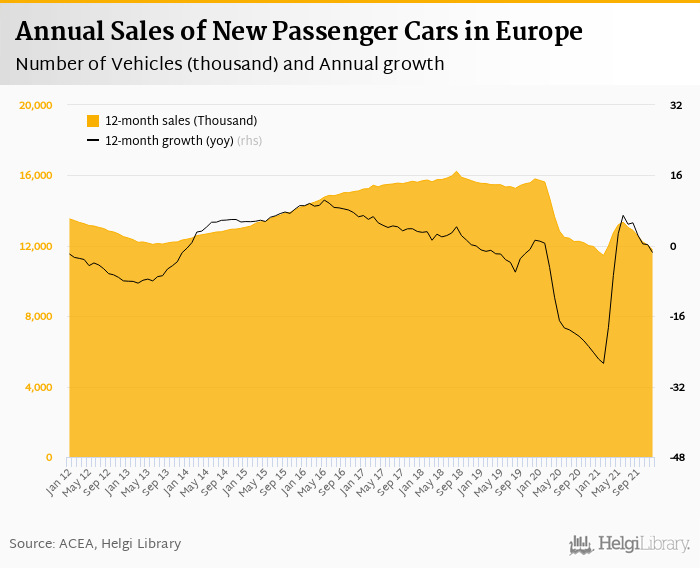

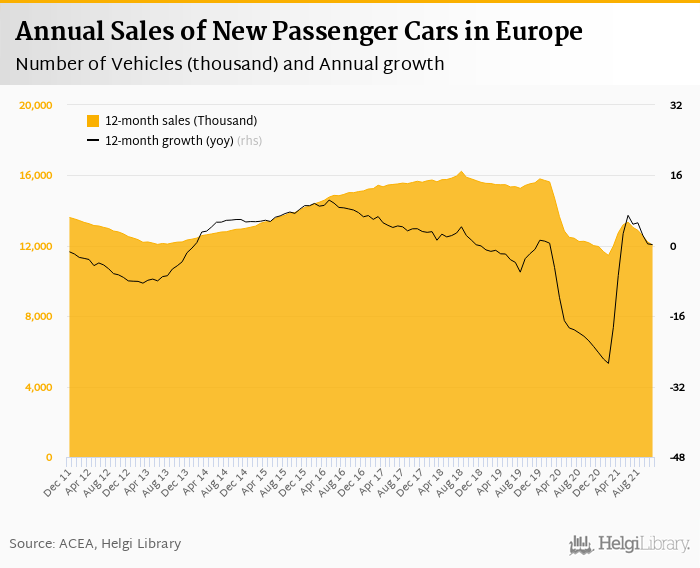

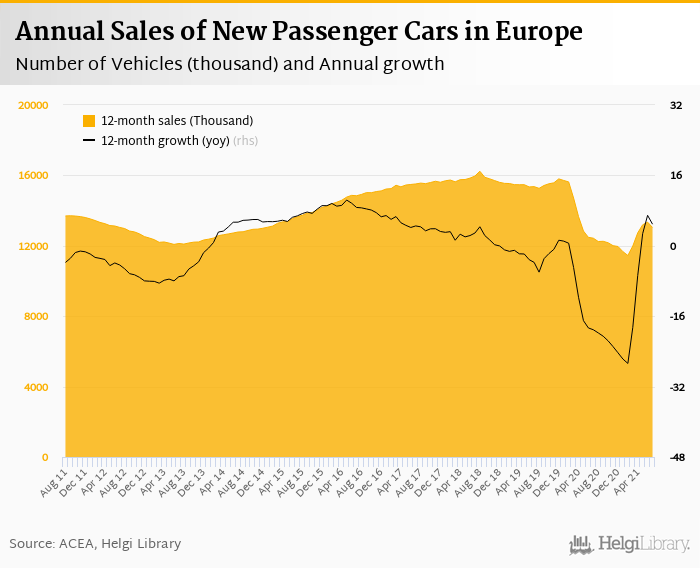

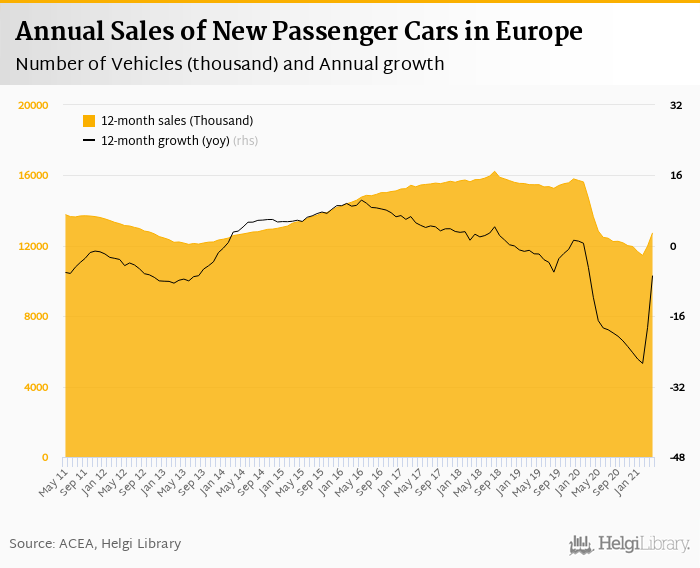

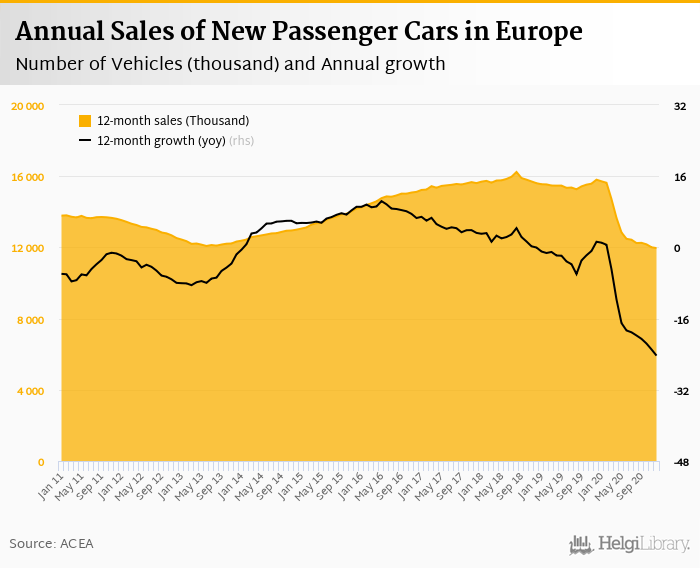

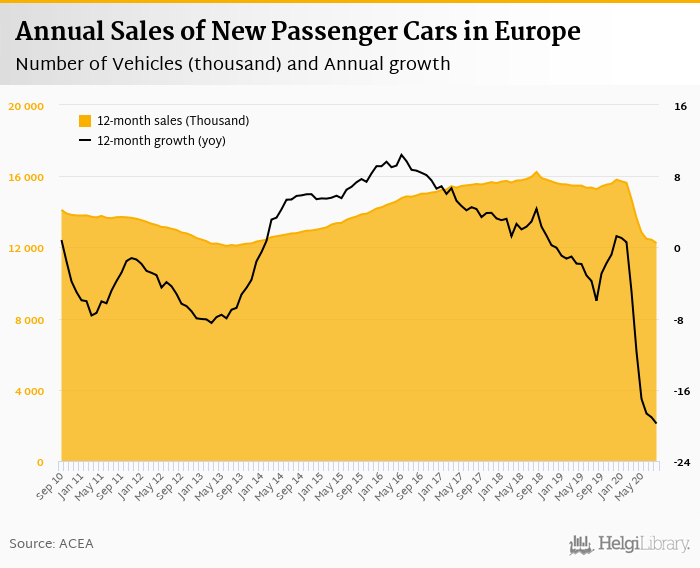

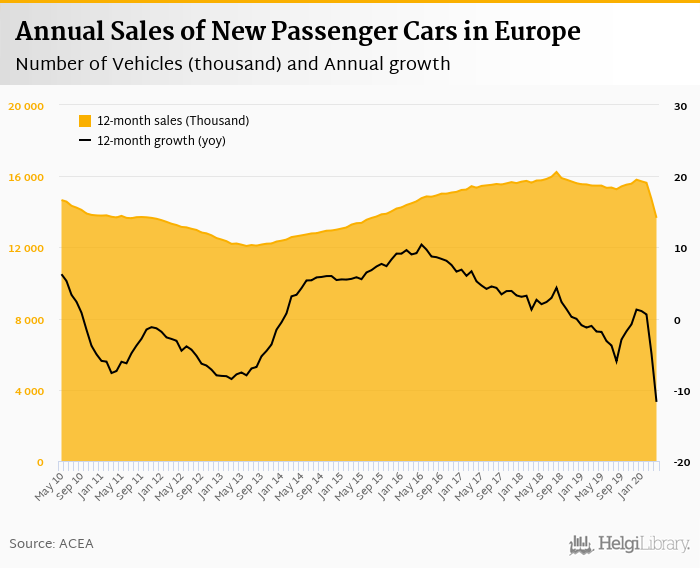

Sales of new cars increased by 129 thousand in October compared to last year

In the first ten months of the year, the growth reached 16.8% yoy

Greece performed relatively the best (up 44.8% yoy) while sales in Norway showed the weakest change compared to the last year (down 28.9% yoy)

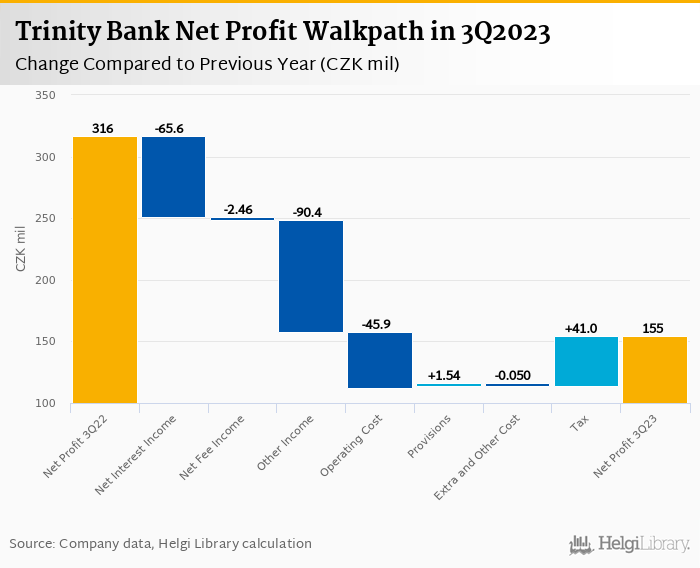

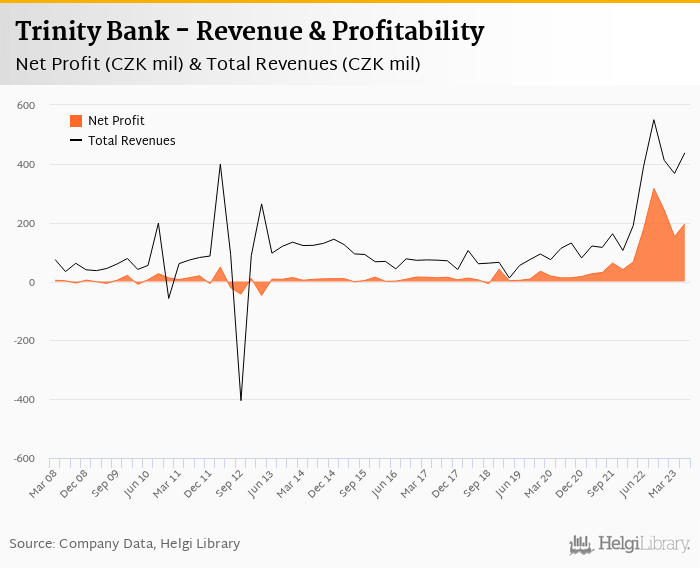

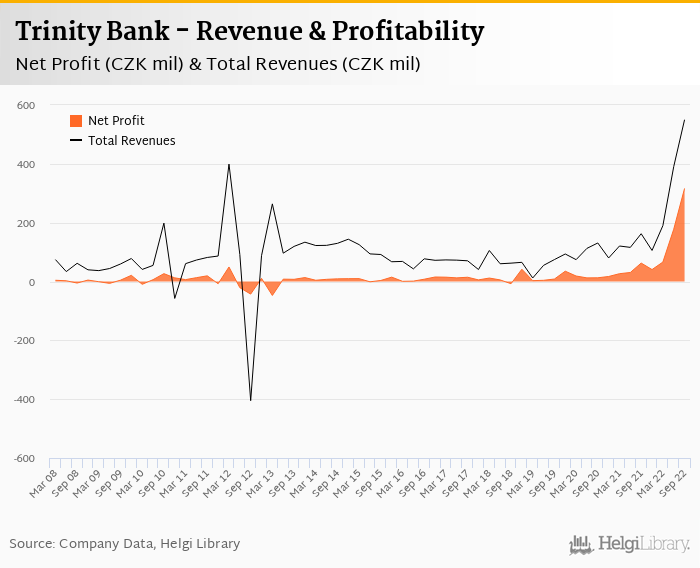

Trinity Bank decreased its net profit 51.2% to CZK 155 mil in 3Q2023 and generated ROE of 11.6%.

Revenues decreased 28.8% yoy and cost rose 31.8%, so cost to income increased to 48.6%

Asset quality appears good with cost of risk at 0.19% and provisions "eatening" only 4.4% of operating profit

Both revenues and profits have been under pressure when compared to last year's record profitability, though 3Q2023 numbers suggest good trends in terms of volume growth and stabilisation of interest margin, two key profit drivers of the Bank.

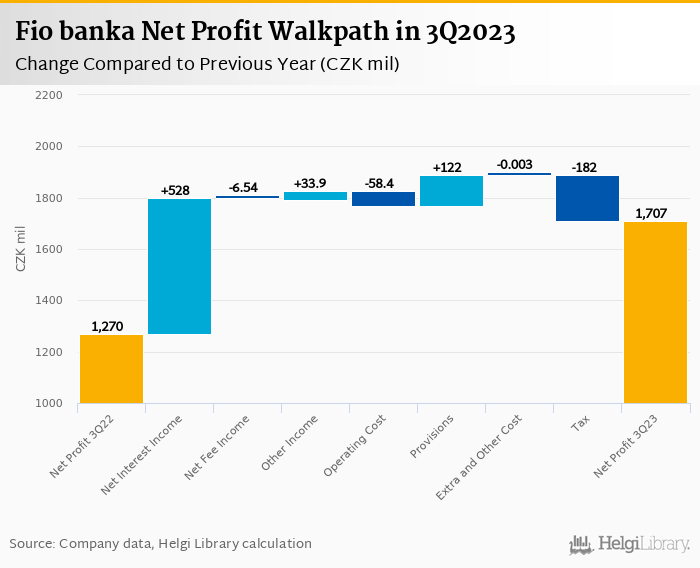

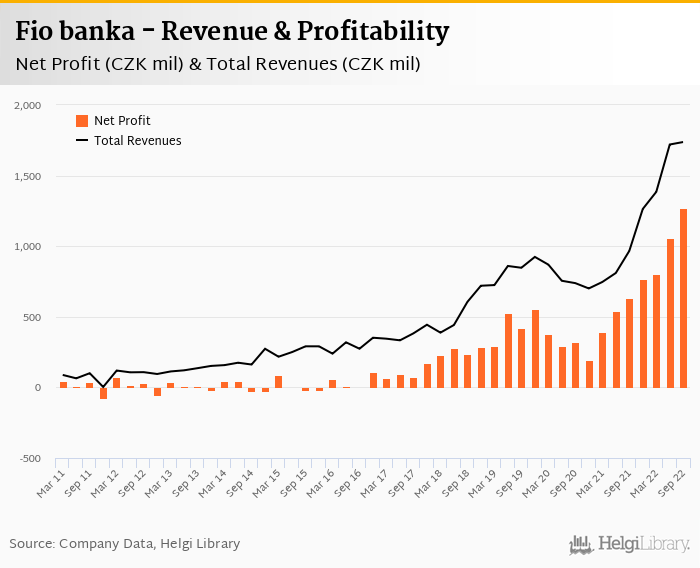

Fio banka rose its net profit 34.4% to CZK 1.71 bil in 3Q2023 and generated ROE of 42.1%.

Revenues increased 32% yoy driven by higher interest margin and cost rose 19.7% due mainly to personnel. Cost to income decreased to impressive 15.5%

Provision write-back of CZK 73 mil further supported Bank's bottom lines, so we assume asset quality further improved last quarter

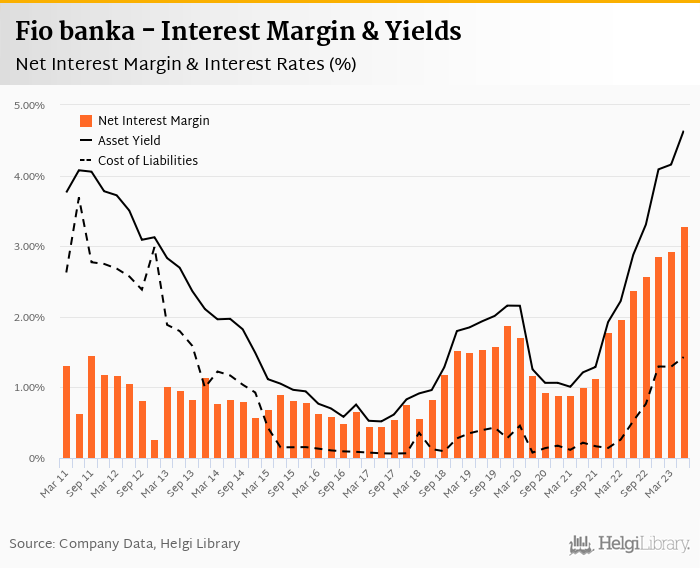

Another record quarterly results announced in the 3Q2023, both in absolute as well as relative terms. With the lowest cost of funding on the market, Fio banka is one of the winners from the higher interest rate environment.

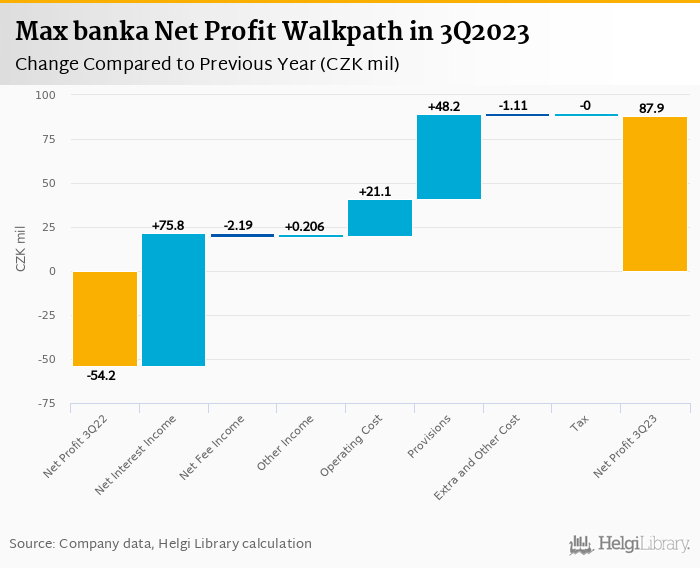

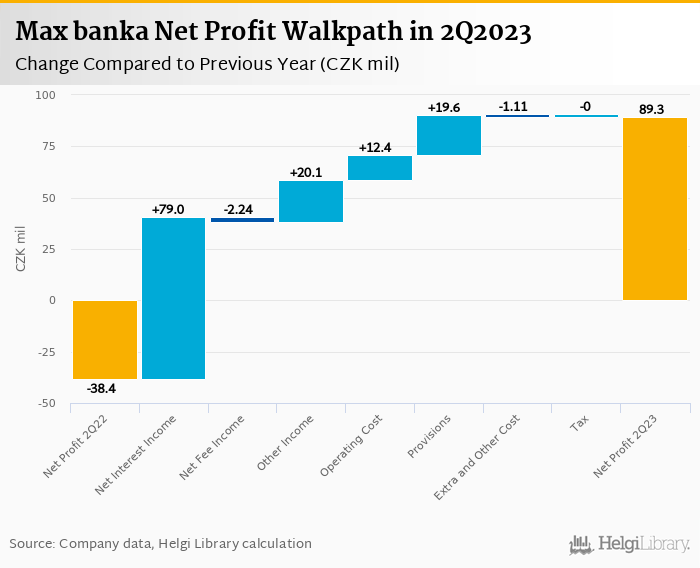

Max banka achieved a third consequtive quarterly profit of CZK 87.9 mil in 3Q2023 and generated ROE of 12.5%.

Revenues increased 76.2% yoy amid five-fold increase in deposits, though cost of funding starts biting. Costs have been cut further 15.1%, so cost to income decreased to 69.5%

Another provision write-back of CZK 36 mil and zero effective tax rate again supported Bank's bottom line in the third quarter.

With 100% of deposits placed with the Central Bank and all the revenues coming from interest income, Max banka is heavily exposed to interbank-rate development, something to watch closely in the coming quarters.

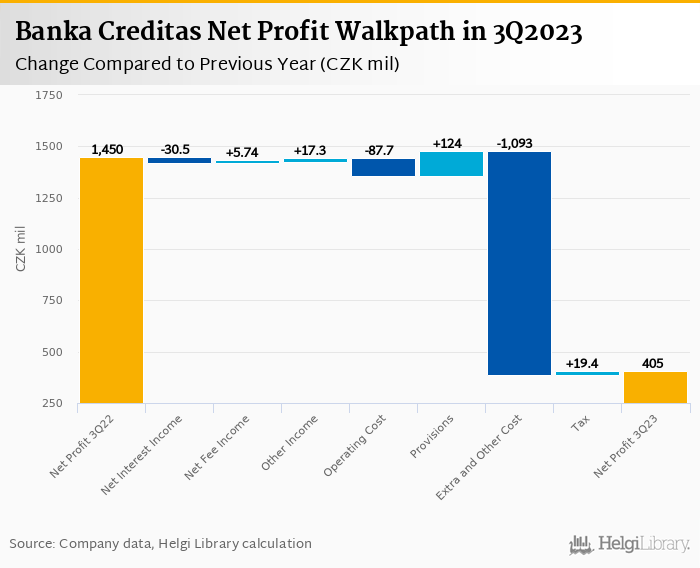

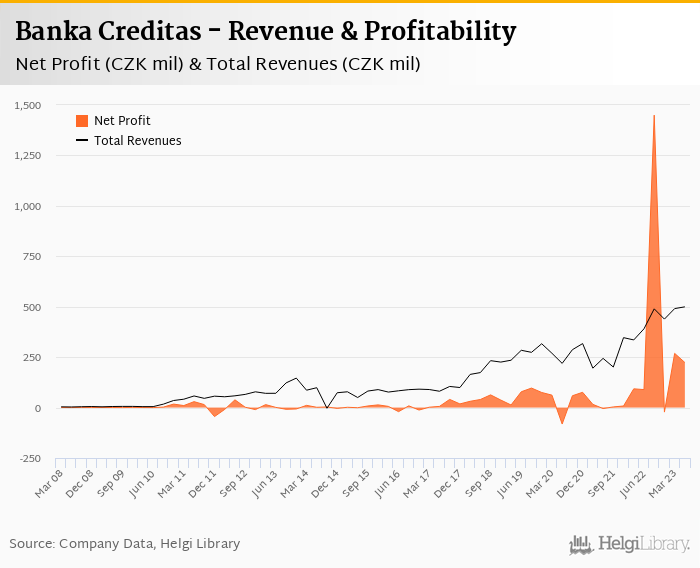

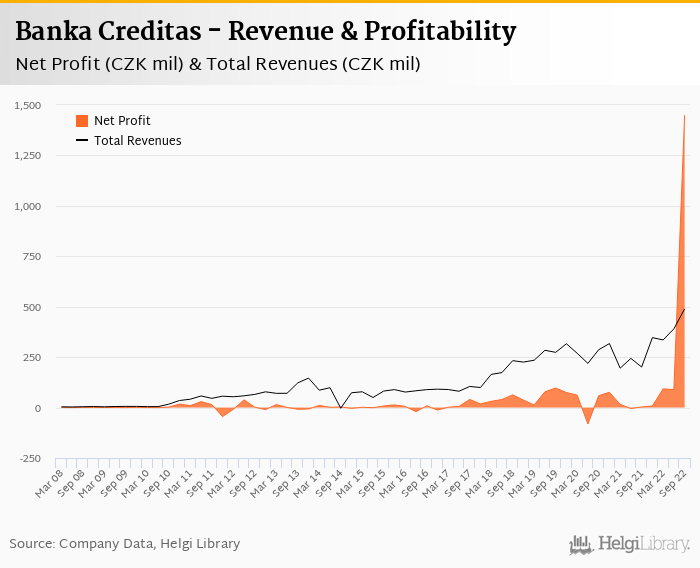

Banka Creditas decreased its net profit 72.1% to CZK 405 mil in 3Q2023 and generated ROE of 20.6%.

Revenues decreased 1.5% yoy as interest margin peaked while costs rose 37% due partly to fast expansion, so cost to income increased to 67%

Operating profit fell 37.5%, so Bank'sbottom line has been supported by CZK 95 mil provision write-back and contribution from subsidiaries

The 3Q23 numbers suggest peaking interest margin amid further slowdown in loan and deposit growth, cost pressure and a good asset quality, though we have to wait for full-year results to see the details.

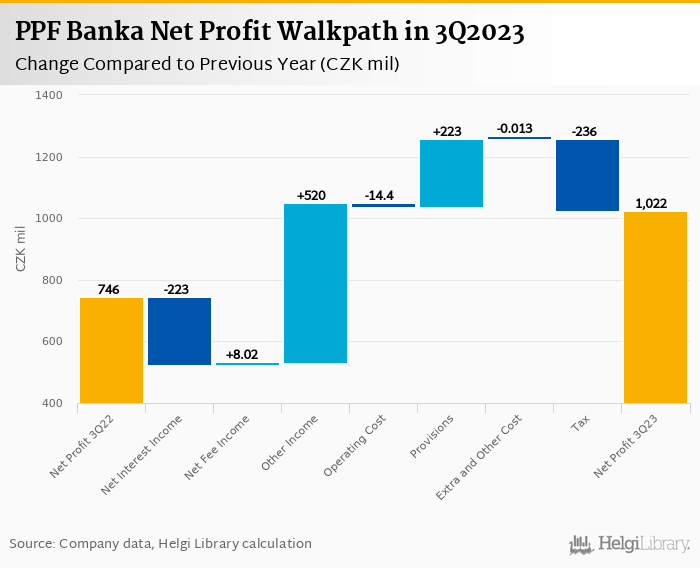

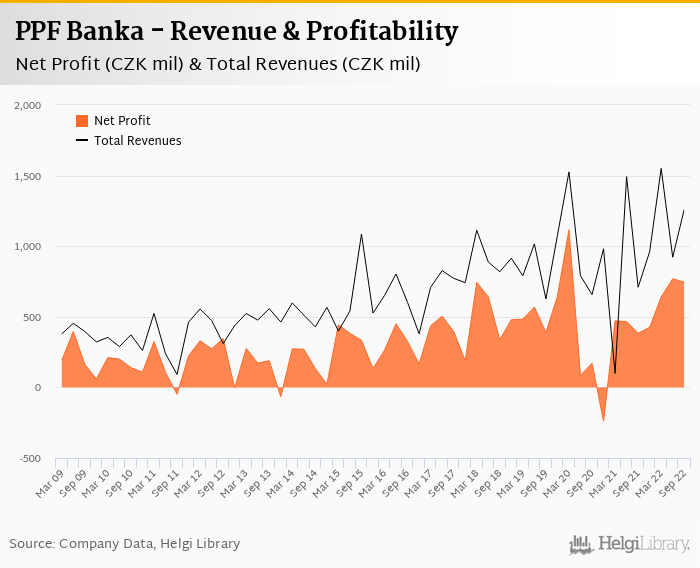

PPF Banka rose its net profit 37.1% to CZK 1.02 bil in 3Q2023 and generated ROE of 21.4%.

The results were driven by an absence of revaluation losses and provision write-backs when compared to last year

Revenues increased 24.1% yoy and cost rose 4.46%, so cost to income decreased to impressive 21.6%

Provision write-back of CZK 43.8 mil further boosted bottom line, so we assume asset quality remains good with NPLs at aroud 1.1-1.2%

A quarter heavily affected by one-offs, though stabilisation of interest margin, solid fee growth and good cost control are positives to point out

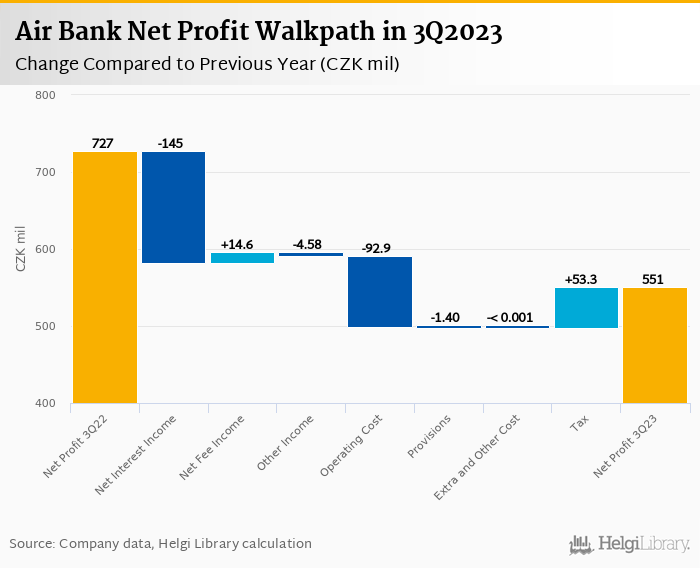

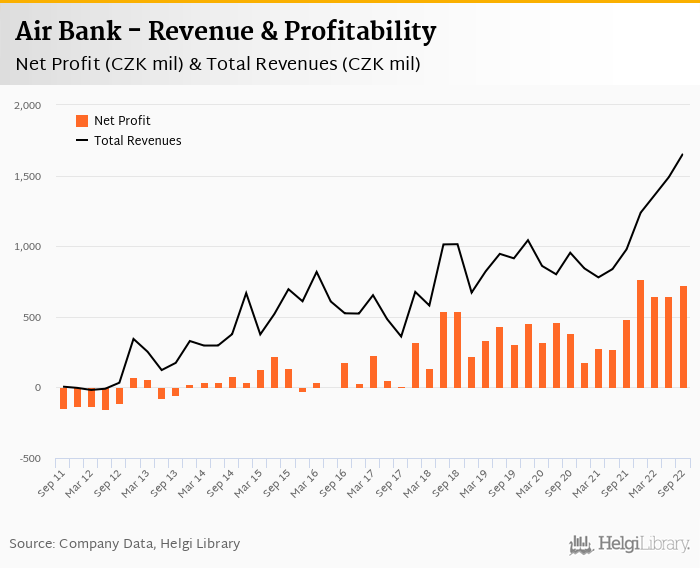

Air Bank decreased its net profit 24.3% to CZK 551 mil in 3Q2023 and generated ROE of 15.5%.

Revenues decreased 8.2% yoy amid lower interest margin while cost rose 16.6%, so cost to income increased to 42.9%

Cost of risk increased to 0.9% of loans, so provisions has eaten a fifth of operating profit last quarter.

We need to wait for full year results to see the big picture, especially, details of Bank's loan portfolio to see the progress in utilization of Bank's clients.

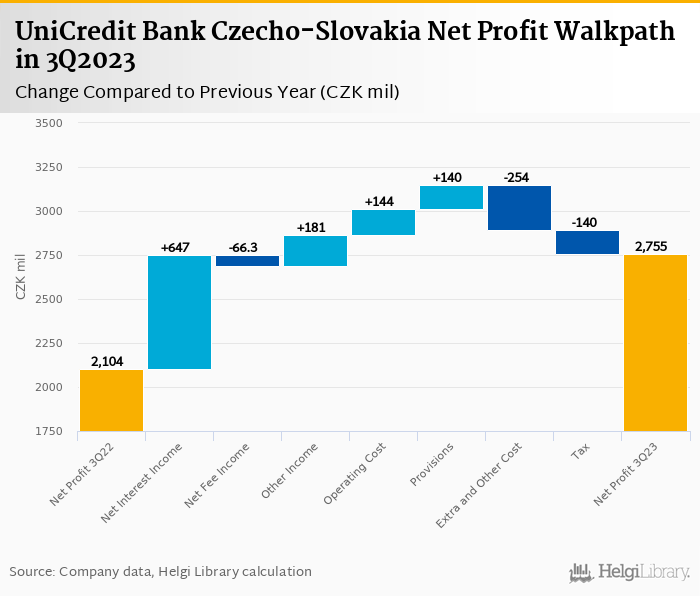

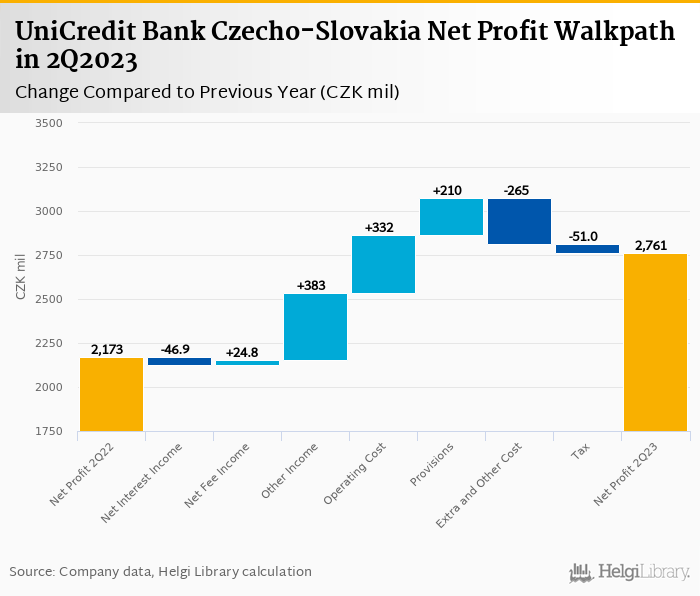

UniCredit Bank Czecho-Slovakia announced strong 3Q2023 results with net profit rising 31% to CZK 2.76 bil and ROE at 14.4%.

Revenues increased 17.1% yoy thanks mainly to strong interest income while cost fell 7.1%. Cost to income therefore decreased to impressive 36.2%

Asset quality seems to be good with no provisions created last quarter, so we assume bad loans stayed at around 1.8% of total loans.

Good momentum unlike other banks reporting 3Q2023 results so far. Similar to other banks, however, weak demand for loans and reduction in interest rates will make the next year more challenging.

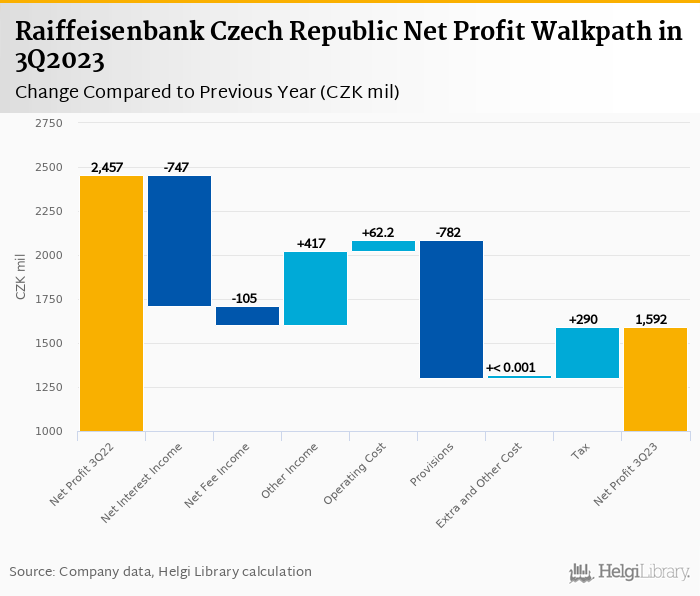

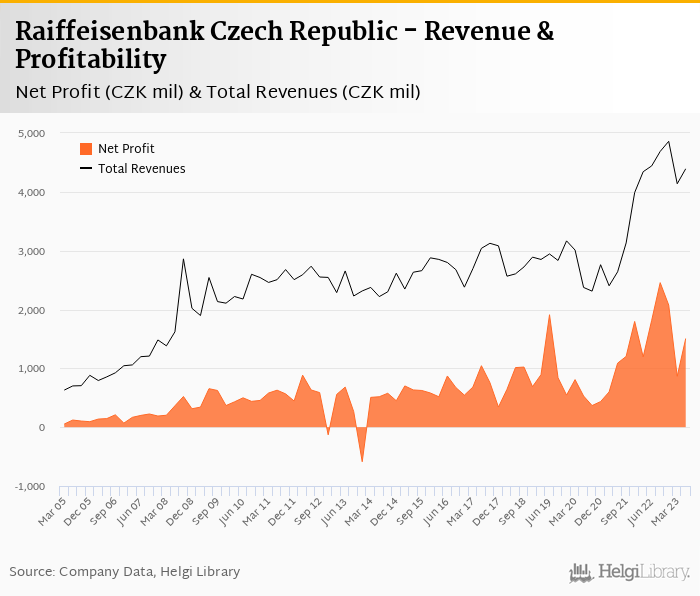

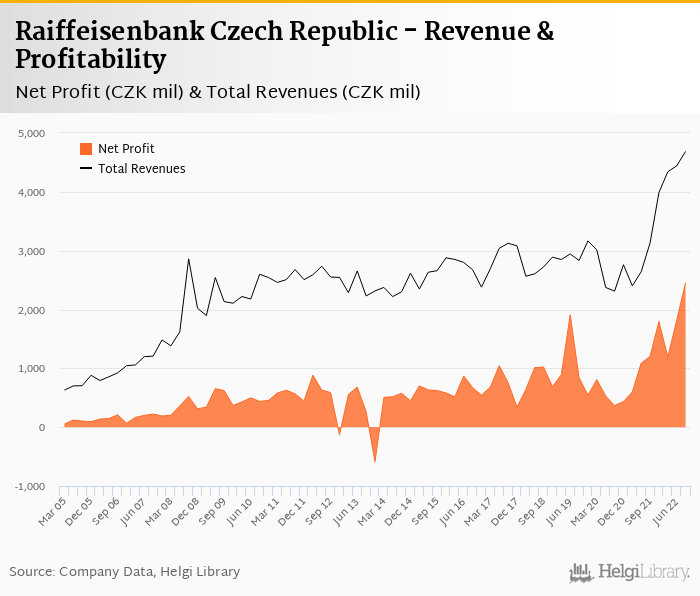

Raiffeisenbank Czech Republic decreased its net profit 35.2% to CZK 1.59 bil in 3Q2023 and generated ROE of 11.7%.

Operating profit fell 2.9% as revenues decreased 9.3% yoy and cost fell 2.9%. Cost to income increased to 49.0%

Cost of risk fell back to annualized 0.29%, a third of the level seen in the previous quarter.

The third quarter suggests a further stabilisation of interest margin, ongoing good cost control and stable asset quality. Good, but not good enough to fight off weak external environment.

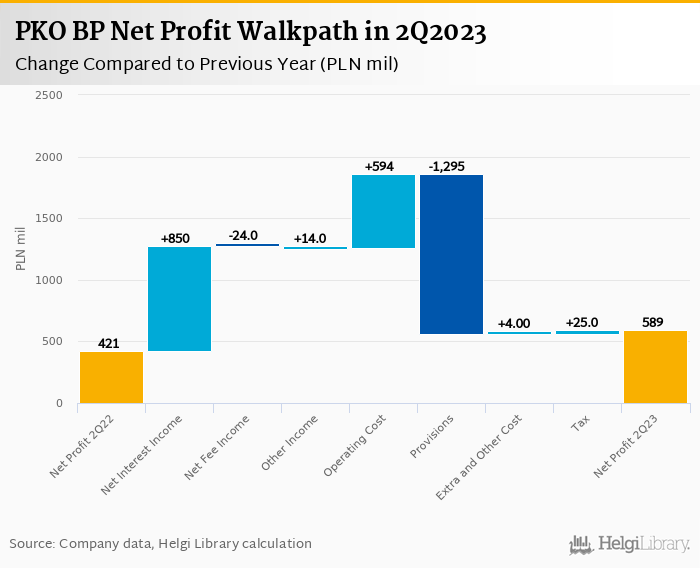

PKO BP rose its adjusted net profit 23.8% to PLN 2.78 bil in 3Q2023 beating market expectations by more than 10% and generating ROE of 25.7%.

Revenues increased 13.6% yoy when adjusted for credit moratoria and cost rose 10.2% when adjusted for lower contribution to the Guarantee Fund, so cost to income decreased to impressive 34.0%

Asset quality remains good with 3.62% of total non-performing while fully covered by provisions. FX mortgages are 71% covered by provisions now

Trading at PE of less than 9x and PBV of 1.2x expected in 2024 while delivering ROE of more than 15%, PKO BP offers a good value. Still, we are bigger fans of Pekao at these prices.

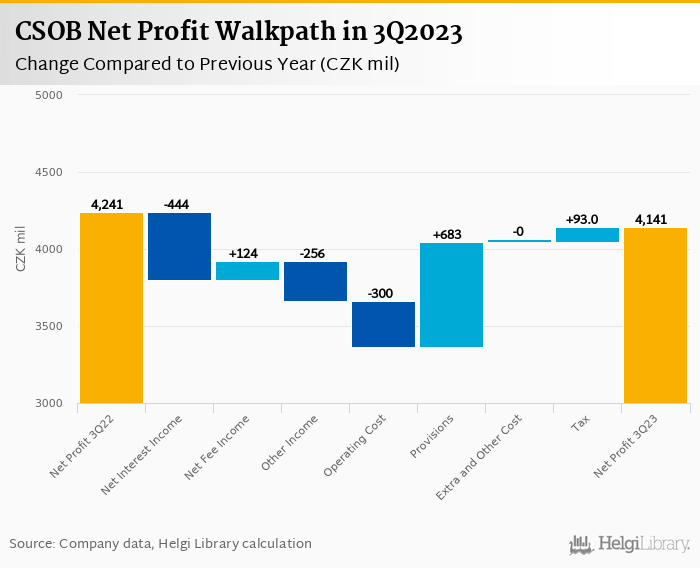

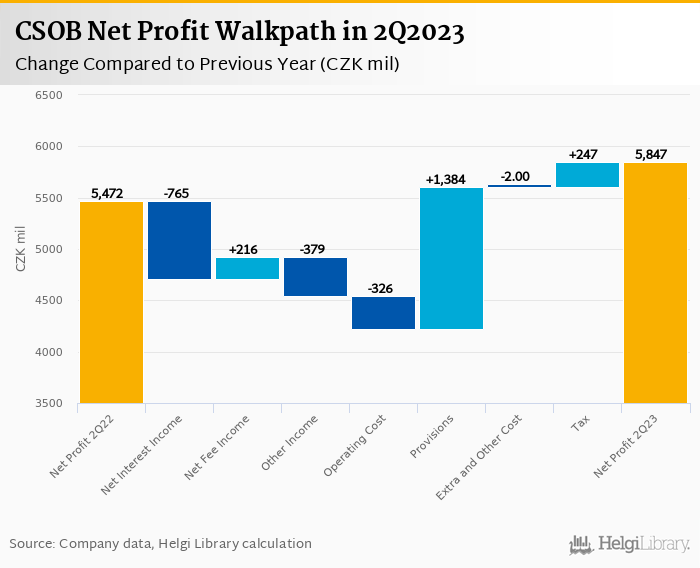

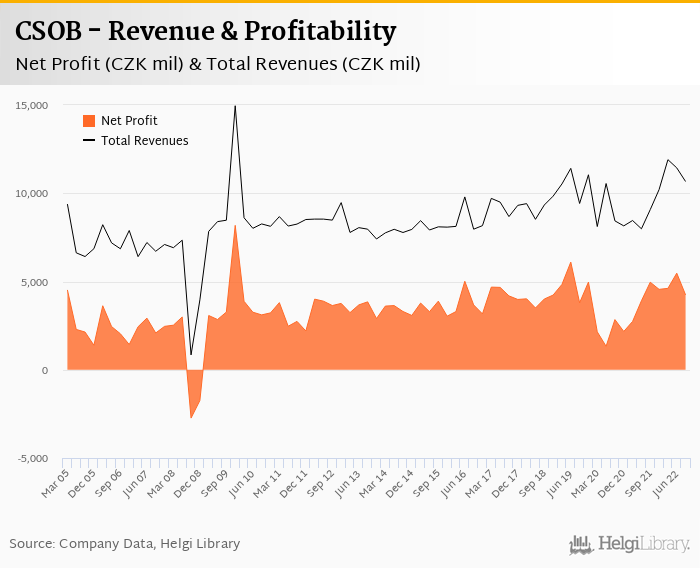

CSOB decreased its net profit 2.35% to CZK 4.14 bil in 3Q2023 and generated ROE of 15.3%.

Revenues decreased 5.40% yoy and cost rose 5.95%, so operating profit fell 15.6% and cost to income increased to 52.9%

Asset quality remains good with NPLs at 1.51% of total loans, so cost of risk was close to zero

With loans to deposit at 60% and capital adequacy at close to 20%, CSOB's balance sheet is hungry for loan demand to pick up...

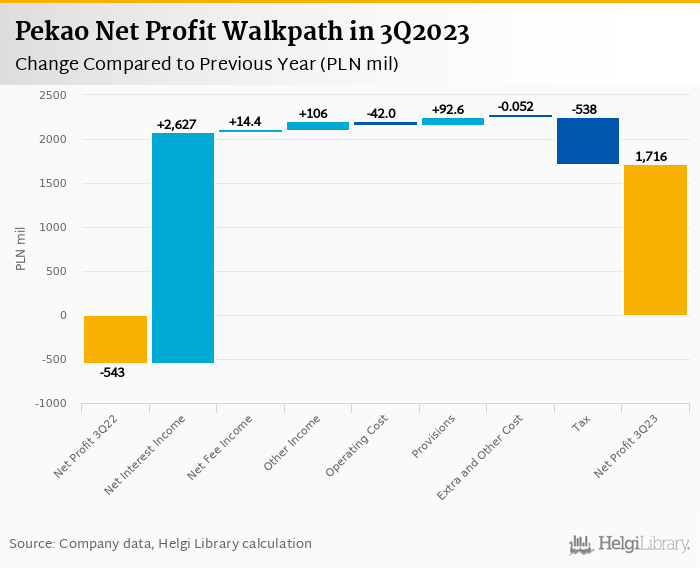

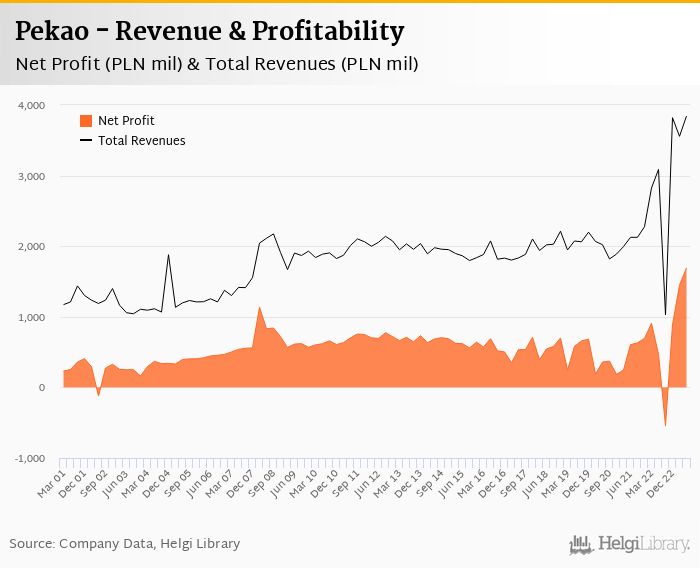

Pekao rose its net profit 4-fold to a record high of PLN 1.72 bil in 3Q2023 and generated ROE of 25.3%. When adjusted for one-offs, the profit was 10.8% higher.

Revenues increased 9.2% yoy when adjusted for credit moratoria and cost rose 16.2% when adjusted for contribution to the Bank Garantee Fund. Cost to income decreased to 37.0%

Asset quality remained good with NPLs at 5.88% and fully covered by provisions incl. its PLN 2.3 bil FX mortgages exposure

Strong results in 2Q2023 already expected by the market driven by strong and peaking interest margin and lower cost of risk. Trading at PE less than 8.0x and PBV of 1.1x with potential 10% dividend yield, Pekao stock looks attractive.

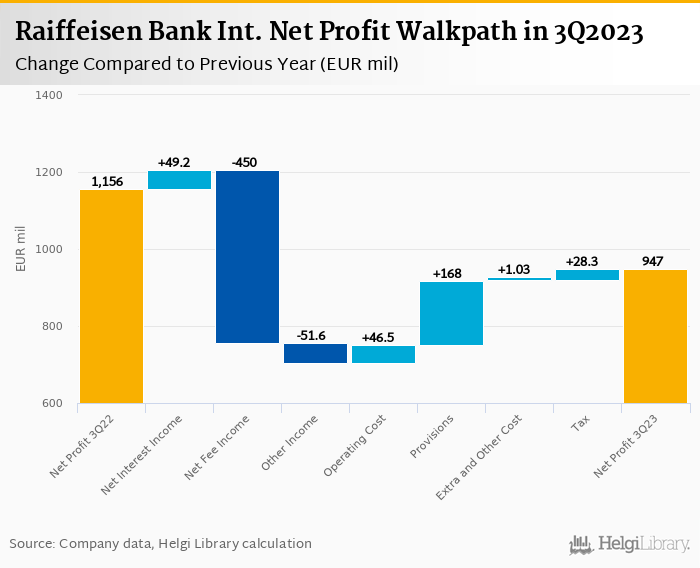

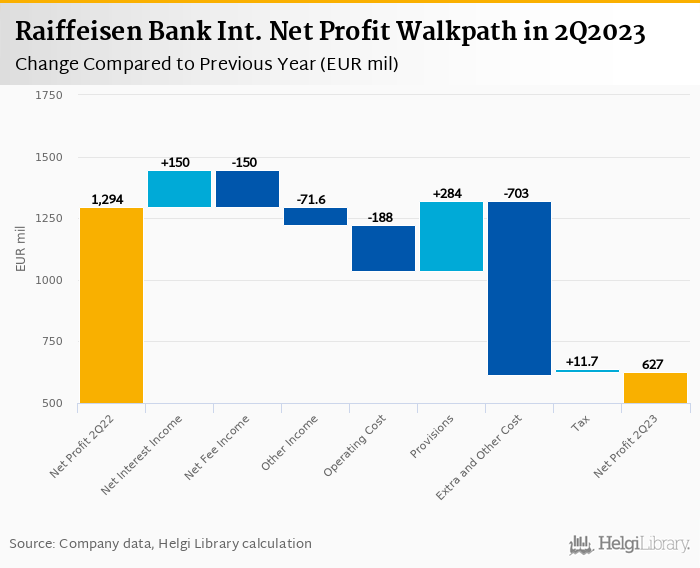

Raiffeisen Bank Int. decreased its net profit 19.3% to EUR 879 mil in 3Q2023 and generated ROE of 19.3%. Better than expected top as well as bottom line numbers lead to a further upgrade in profit guidance for 2023.

For the first nine months of 2023, profit would have grown 26% to EUR 1.036 mil, ROE would have reached 10.9% and CET1 would have amounted to 14.4% when adjusted for Russian business and a sale of Bulgarian unit.

In 3Q23, revenues decreased 16.8% yoy and cost fell 5.0%, so cost to income increased to 39.1% (or 45.2% adjusted). Bad loans fell to 2.80% and 59% of them were covered by provisions.

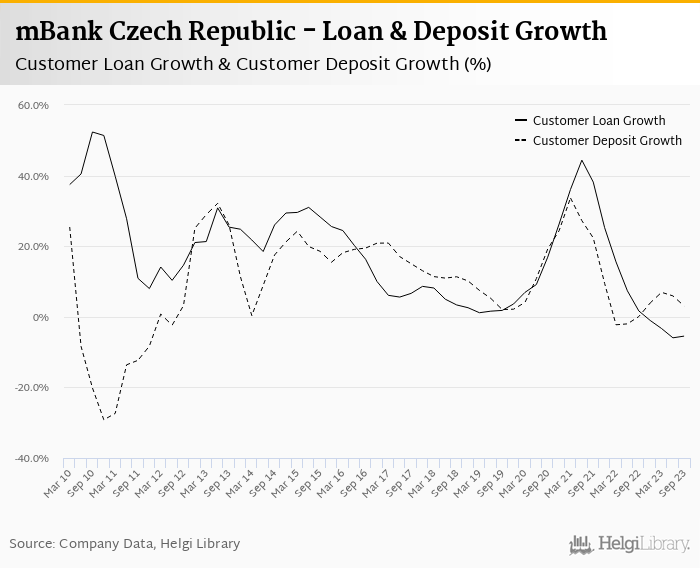

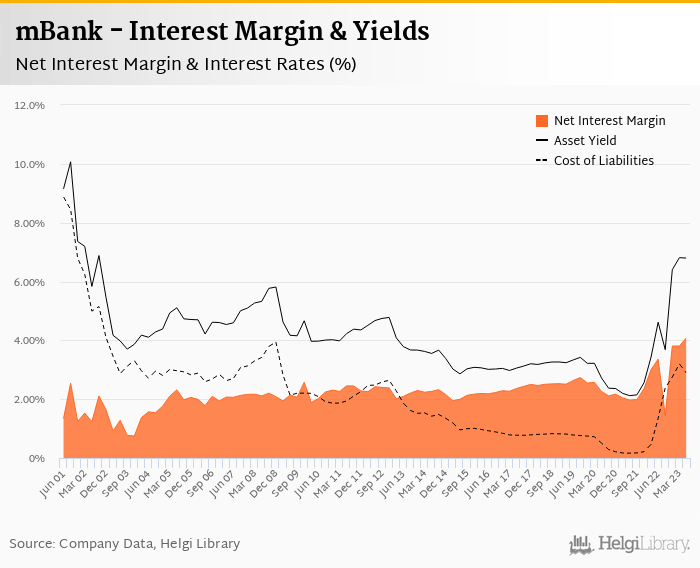

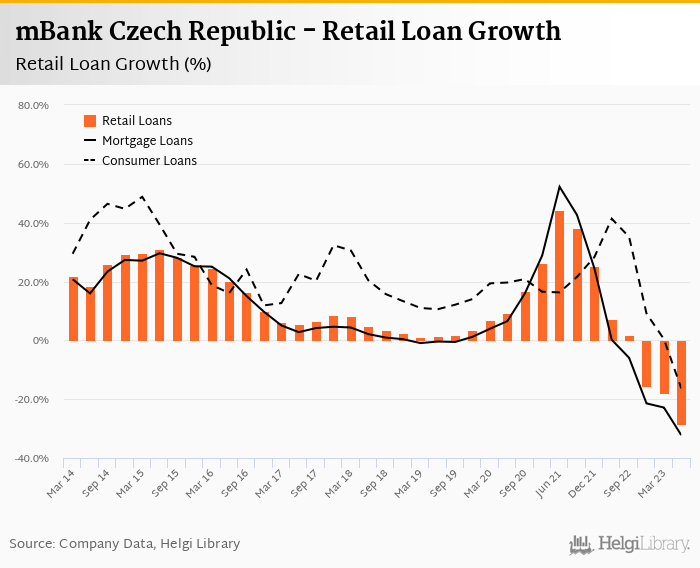

mBank Czech Republic gained further 25,000 customers since the beginning of the year servicing 775,701 clients

Average balance remains stable at around CZK 91,000 per account meaning the Bank has been slightly losing market share

On the lending market, Bank's position is stable in consumer loans (at around 2.0% of the market) while continue to lose in mortgage business (1.5% market share)

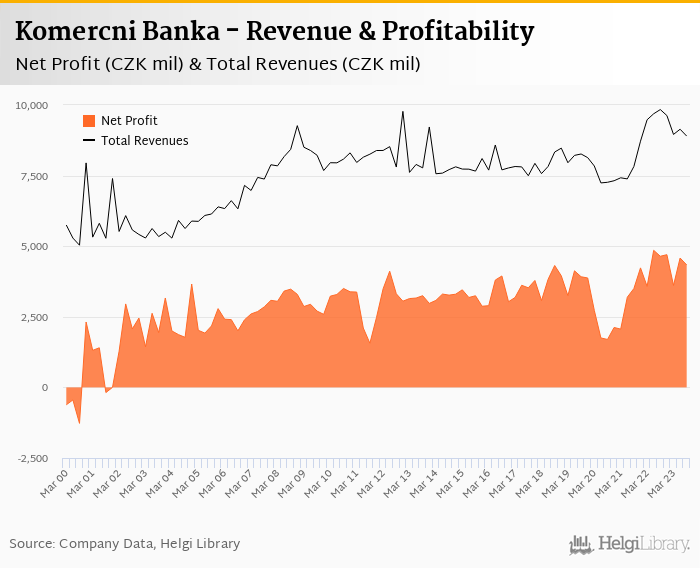

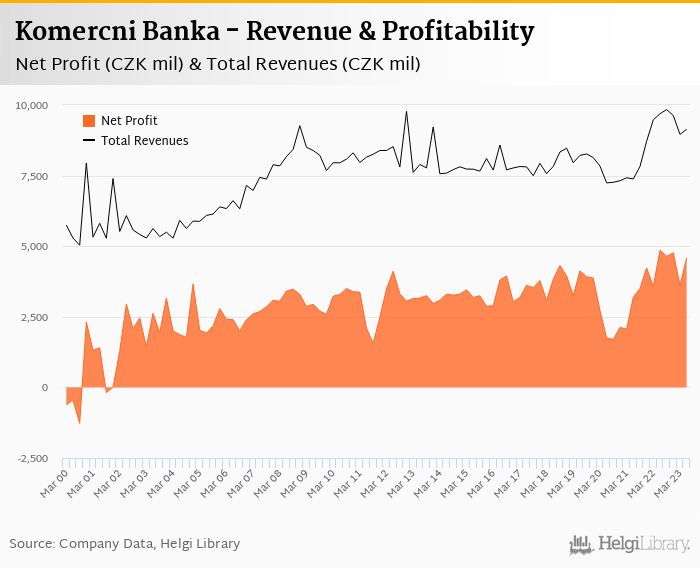

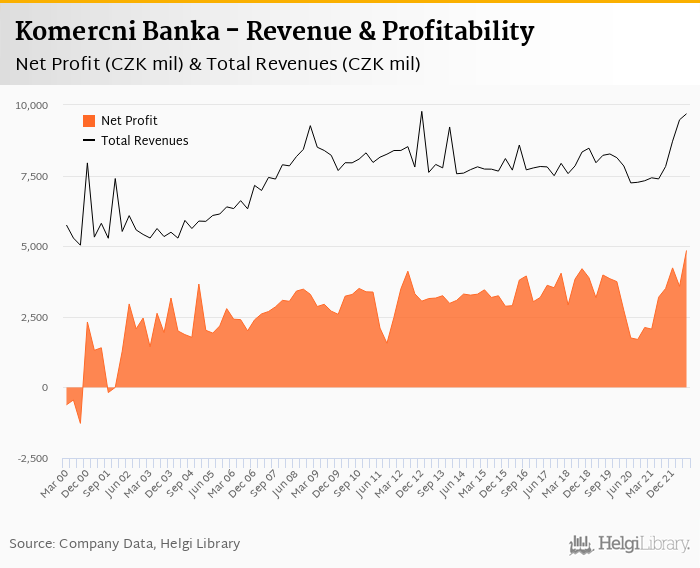

Komercni Banka decreased its net profit 7.3% to CZK 4.27 bil in 3Q2023 and generated ROE of 14.1%

Operating performance disappointed slightly as revenues decreased 9.5% yoy and cost rose 7.19%, so cost to income increased to 44.0%

Provision write-backs and lower effective tax rate were the main positive surprises this quarter, albeit rather lower quality ones

Trading at PE of 9.0x and PBV of 1.1x with a dividend yield at around 7.0%, Komercni Banka looks attractive, though with a risk of a "value trap". Erste Bank and Polish banks seem to be offering a better story now.

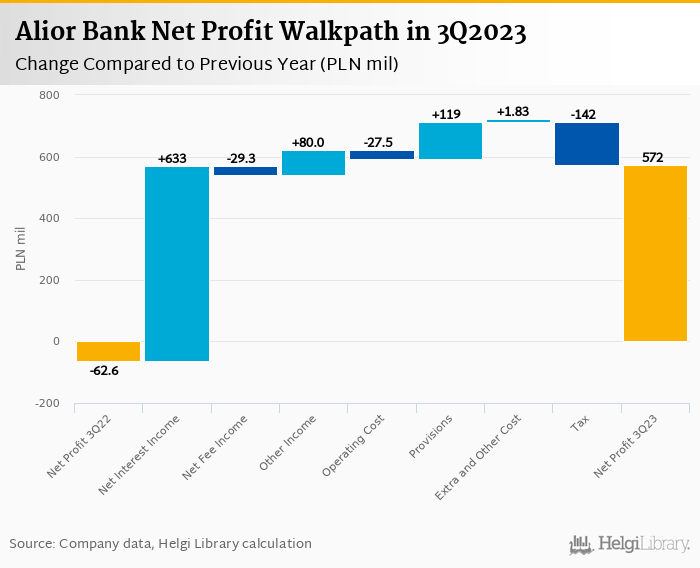

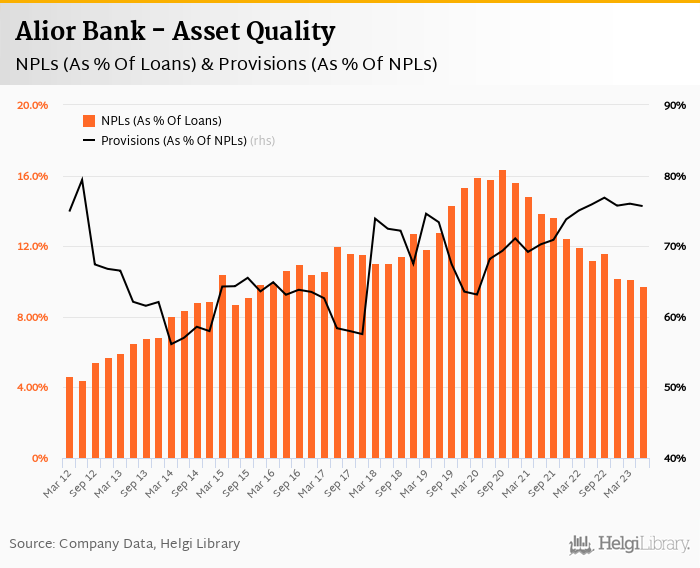

Alior Bank posted another record net profit of PLN PLN 572 mil in 3Q2023 beating market expectations by some 10%.

Revenues increased 12.3% yoy when adjusted for credit moratoria and cost rose by 25.6% when adjusted for contribution to the Bank Guarantee Fund. Still, cost to income decreased to 33.4%

Share of bad loans fell further to 8.93% and provision coverage rose to 77.1%. Management targets cost of risk of only 1.0% in 2024.

Trading at PE of 8.0x and PBV of 1.0x and doing all it can to enjoy current high interest rate environment, the show might still go on for Alior Bank

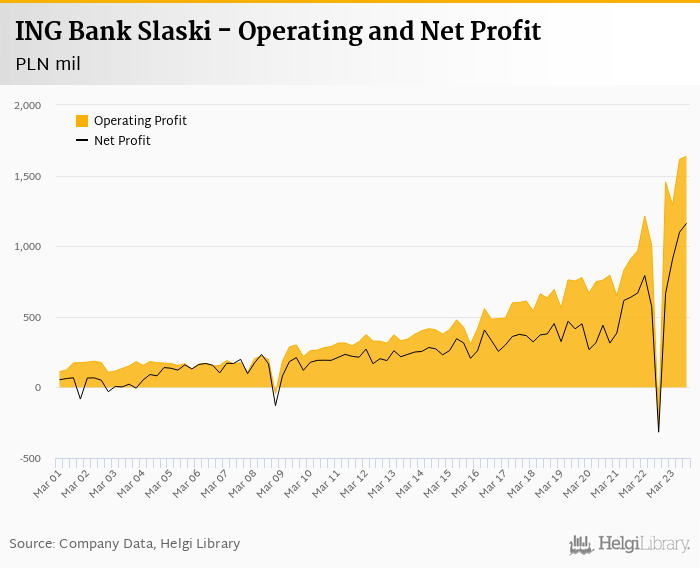

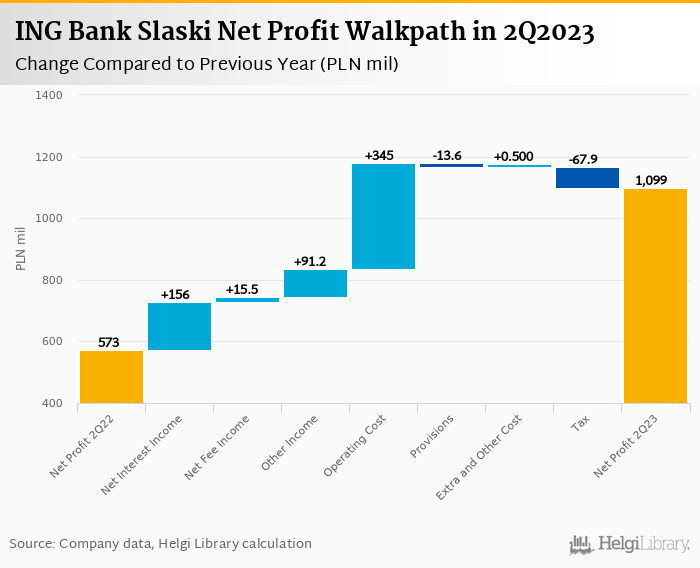

ING Bank Slaski rose its net profit 28.4% to PLN 1,162 mil in 3Q2023 when adjusted for last year's credit moratoria and generated ROE of 33.0%.

Revenues increased 13.3% yoy when adjusted and cost rose 3.86%, so cost to income decreased to 38.5%

Solid results with record quarterly operating and net profitability, though partly expected by the market. Trading at adj. PBV of 1.4x and PE of 9.0x expected in 2024, ING Slaski continues to trade with a premium for its quality.

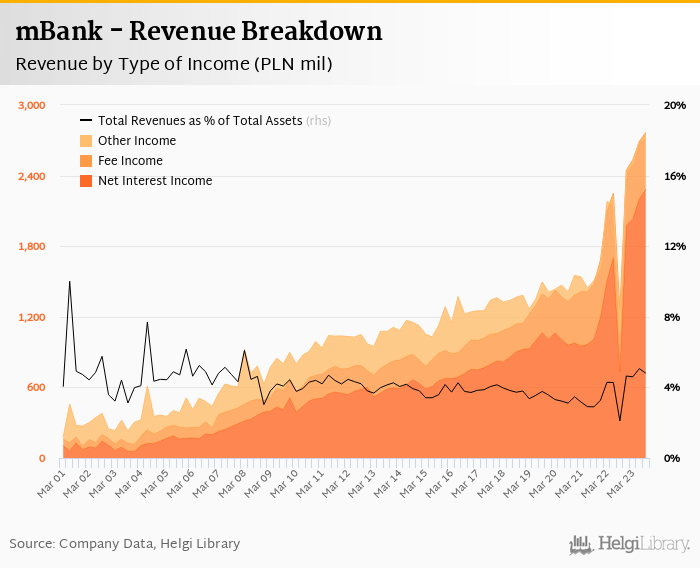

mBank reported a net loss of PLN 83.0 mil in 3Q2023 due mainly to further PLN 1.1 bil of provisions for FX mortgages

Operating profitability was a record high at almost PLN 2.o bil due mainly to still improving interest margin

Bad loans rose to 4.24% of total loans and provision coverage increased to 70%. Almost 86% of FX mortgages are covered by provisions now.

The results were roughly in line with market expectations and valuation of PE of 9.0x and PBV of 1.3 expected in 2024 suggest market expects the worst in FX saga to be over

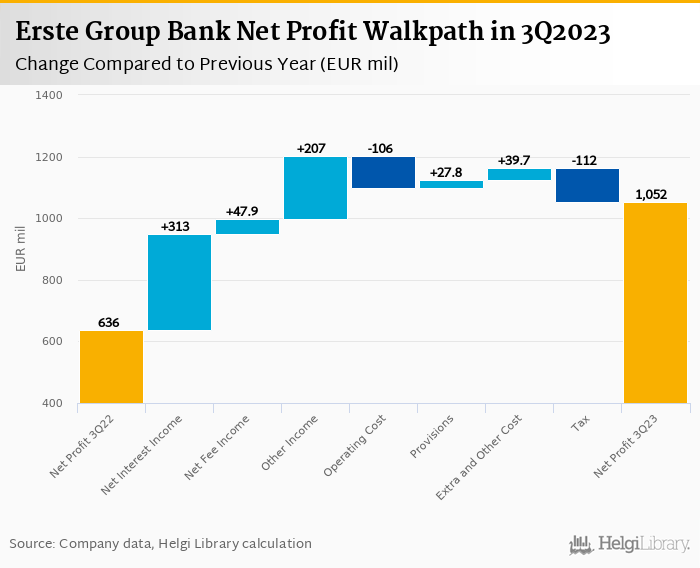

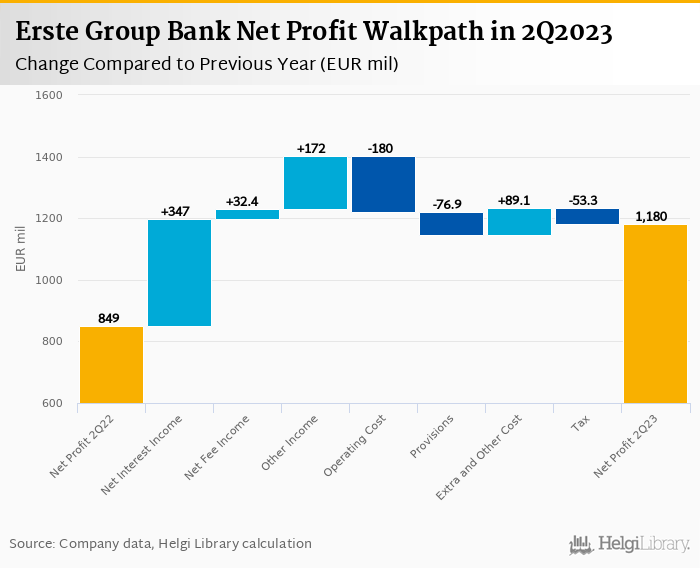

Erste Group Bank beat again market expectations in 3Q2023 with net profit rising 61% to EUR 820 mil and ROE accounting for ROE of 15.5%.

Revenues increased strong 27% yoy driven by rising margin, but fee as well as other income performed strongly

Austria remains the main driver recording historical profits. In the last two quarters, it generated 45% of the Group overall profitability

Trading at PE of around 7.0x, PBV of 0.7x and expected in 2024 and offering potential dividend yield of 8-10%, Erste Bank looks as one of the most attractive banking stocks in the CEE.

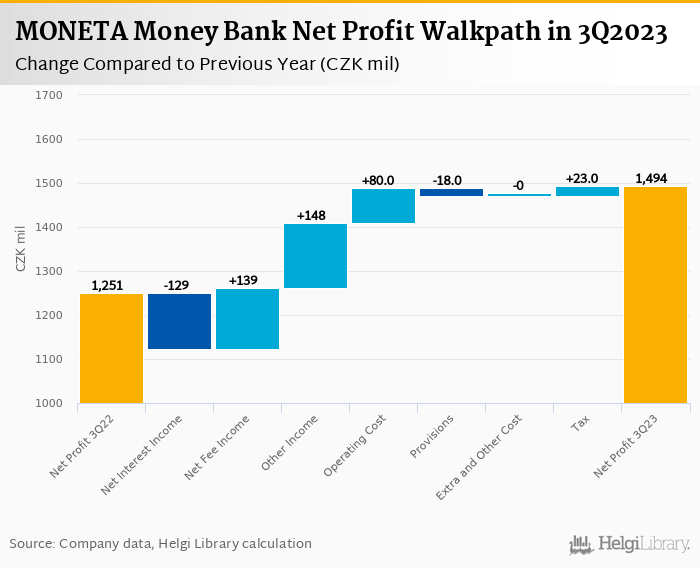

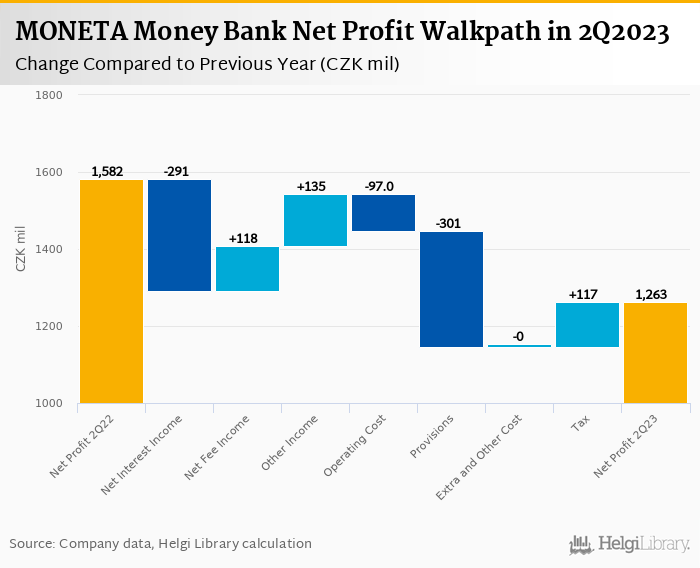

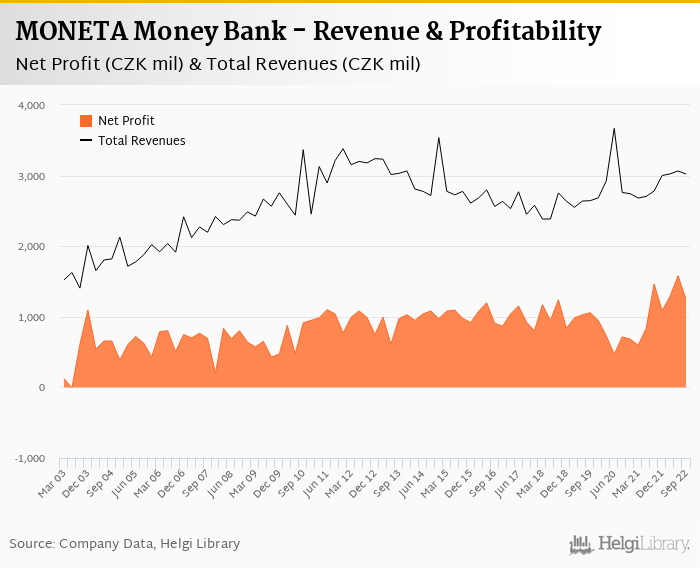

MONETA Money Bank rose its net profit 19.4% to CZK 1.49 bil in 3Q2023 and generated impressive ROE of 19.8%.

Strong revenue generation (up 5.2% yoy) and impressive cost control (down 5.9%) and lower effective tax rate are behind the better than expected profitability

Better than expected results and solid capitalization and release of further CZK 500 mil in 2024 from capital requirements paves room for interesting dividend in 2024

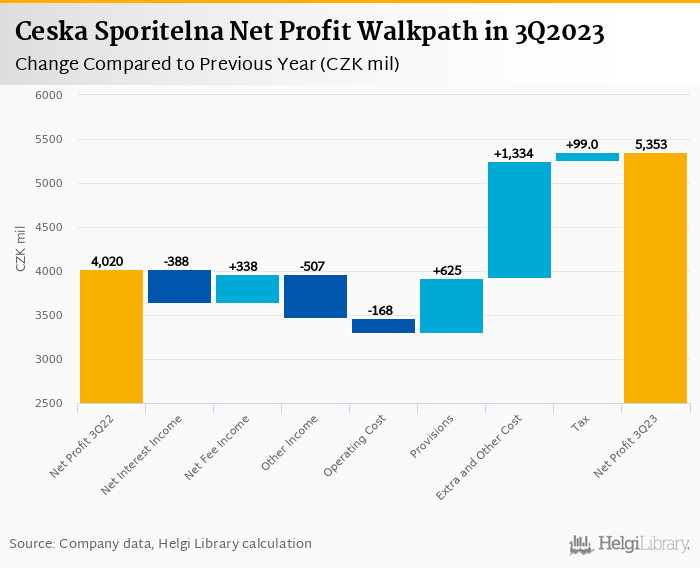

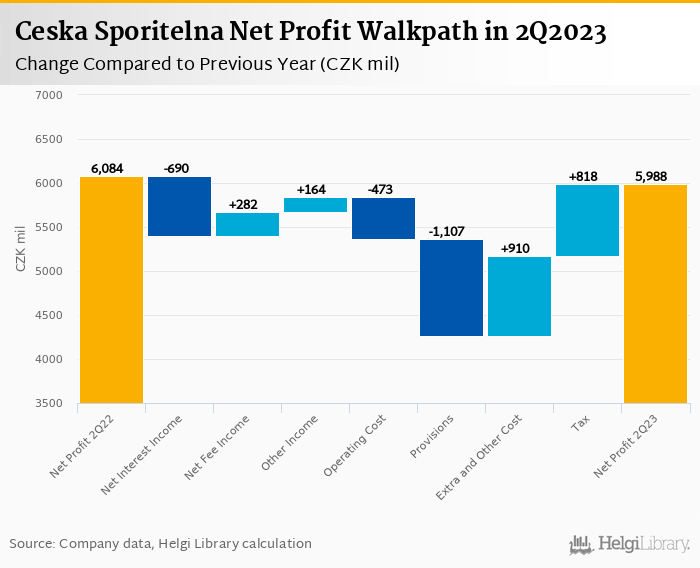

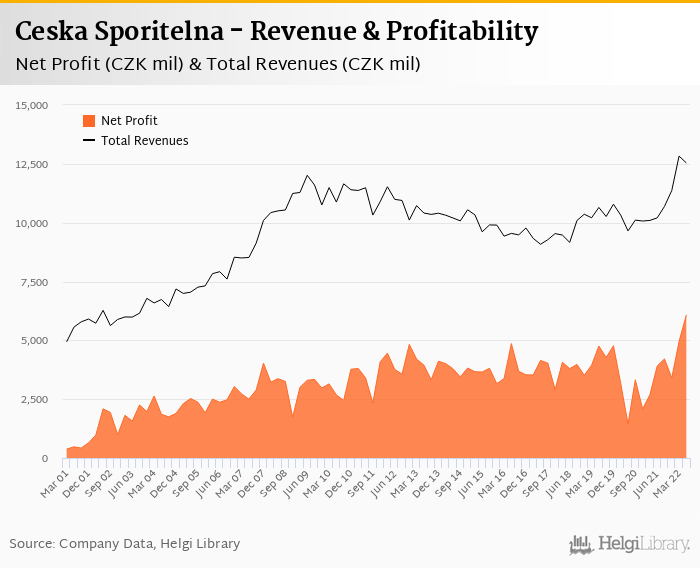

Ceska Sporitelna rose its net profit 33.2% to CZK 5.34 bil in 3Q2023 and generated ROE of 15.8%.

Absence of losses from bond portfolio and buildings from last year and provision write-backs for Sberbank's portfolio drove the bottom line last quarter.

On the operating level, profit fell 10% yoy due mainly to higher cost of funding and weak trading income, though cost cutting seems to be accelerating.

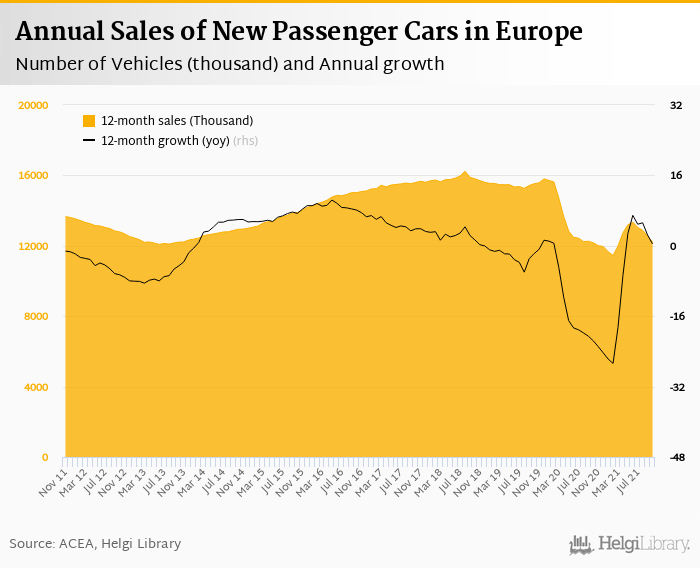

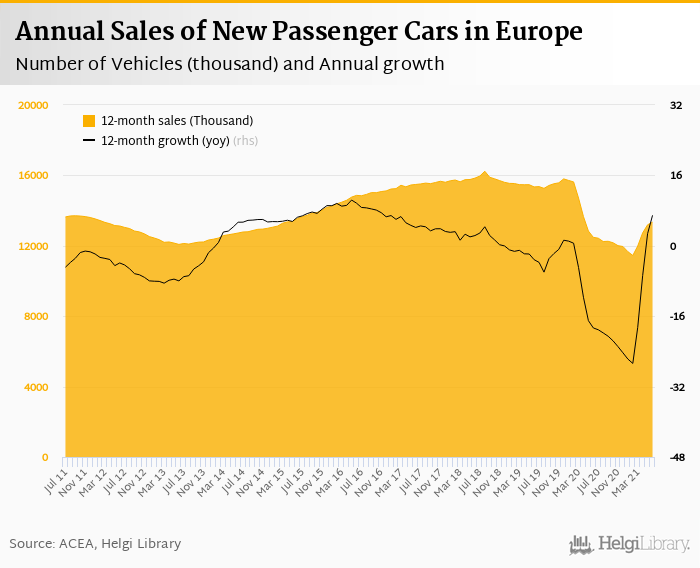

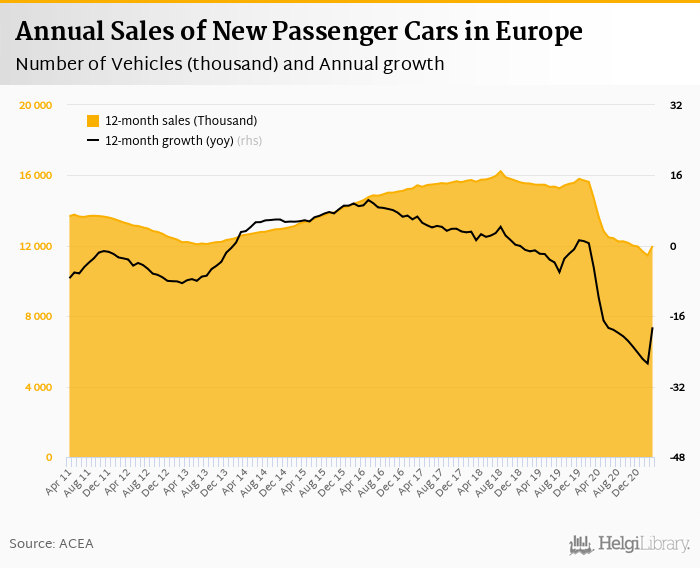

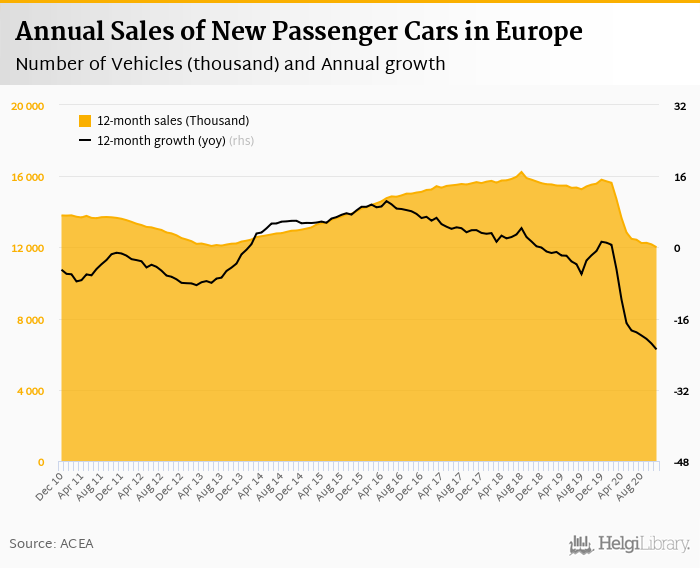

Sales of new cars increased by 117 thousand in September compared to last year

In the first nine months of the year, the growth reached 17% yoy

Bulgaria performed relatively the best (up 40.6% yoy) while sales in Norway showed the weakest change compared to the last year (down 29.4% yoy)

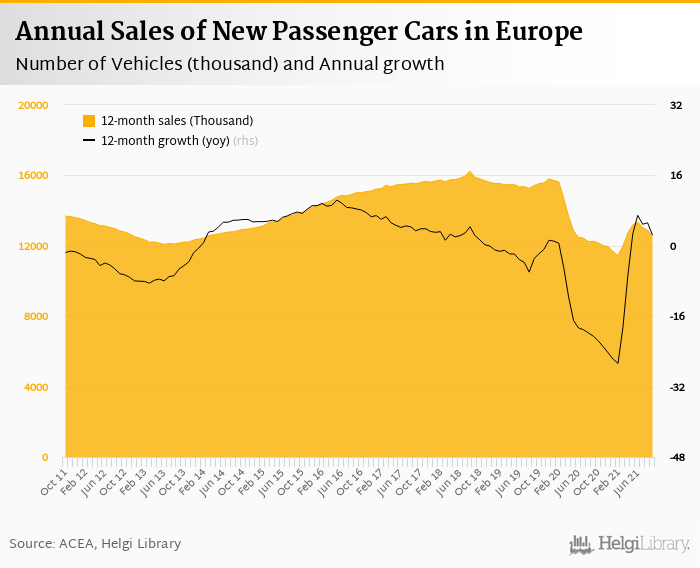

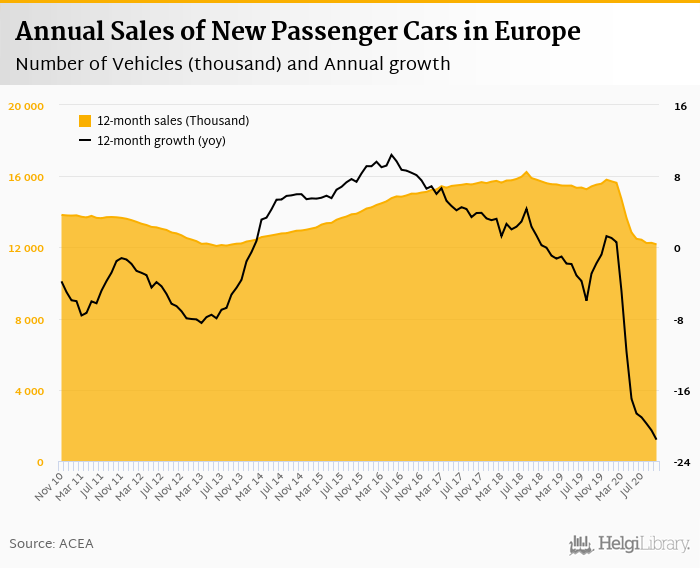

Sales of new cars increased by 156 thousand in August compared to last year

In the first eight months of the year, the growth reached 17.9% yoy

Bulgaria performed relatively the best (up 37.9% yoy) while sales in Hungary showed the weakest change compared to the last year (down 10.4% yoy)

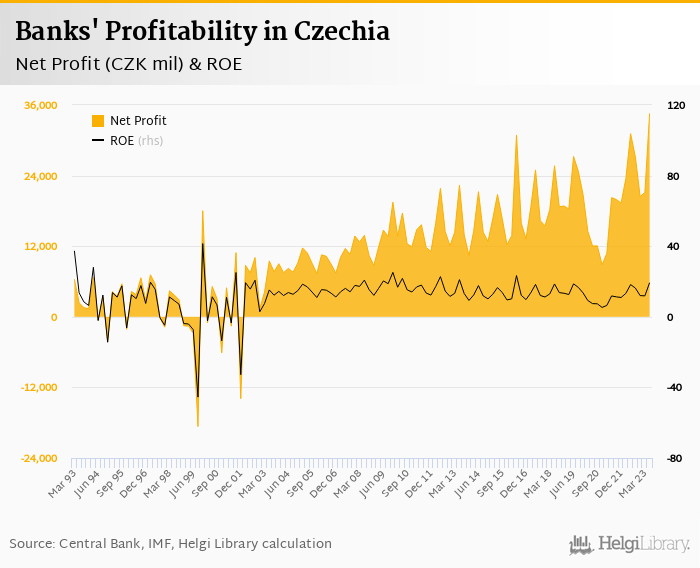

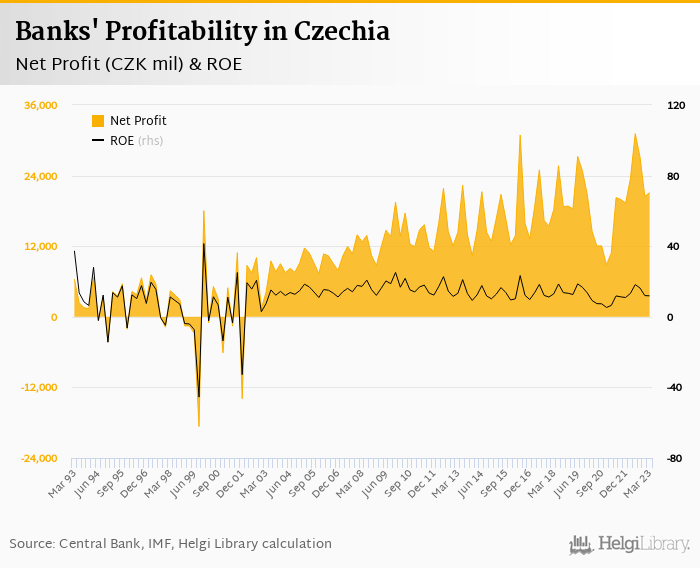

Czech banks increased net profit 11.0% yoy to CZK 34.6 bil in the second quarter of 2023 and generated ROE of 19.3%.

Operating income rose 14.8%, cost to income dropped to 31.2% and banks' share of bad loans fell to 1.82%.

Ceska Sporitelna generated the biggest profit while Modra Pyramida Stavebni Sporitelna produced the smallest one.

Polish banks increased net profit 60.1% yoy to PLN 6,862 mil in the second quarter of 2023 and generated ROE of 12.0%.

Operating income rose 8.65%, cost to income dropped to 44.5% and banks' share of bad loans fell to 4.09%.

Pekao generated the biggest profit while mBank produced the biggest loss.

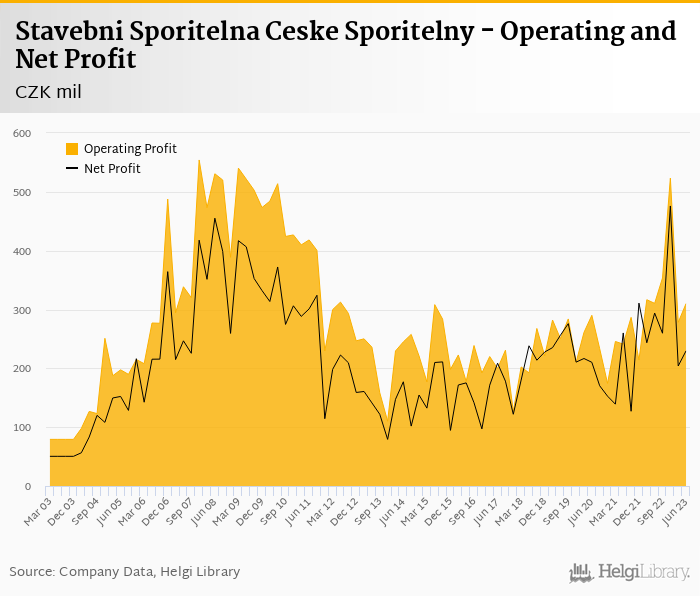

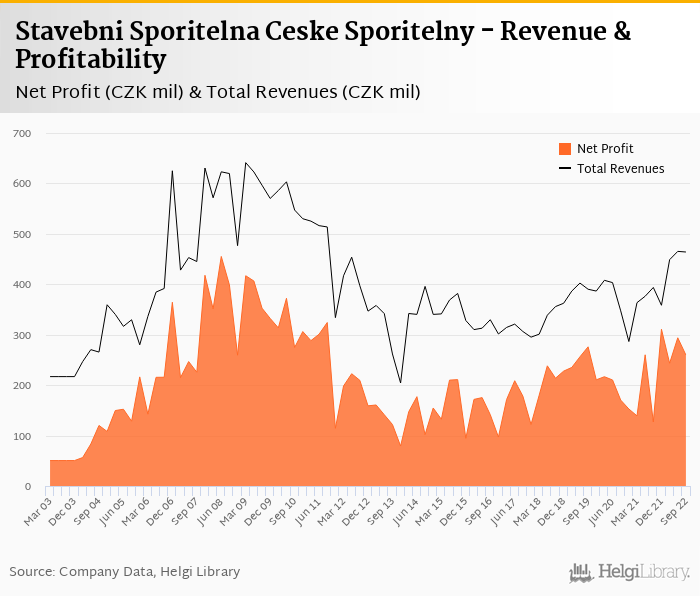

Stavebni Sporitelna Ceske Sporitelny's net profit fell 21.8% to CZK 230 mil in 2Q2023 with ROE at 10.8%.

Operating profit was flattish as 4.9% decrease in revenues was offset by a 14.5% reduction on the cost side. Cost to income fell below 30%.

Asset quality seems to be good with NPL ratio staying around 1.0% on our estimates

Loan to deposit ratio increased further to 109% and capital adequacy might be around 30%.

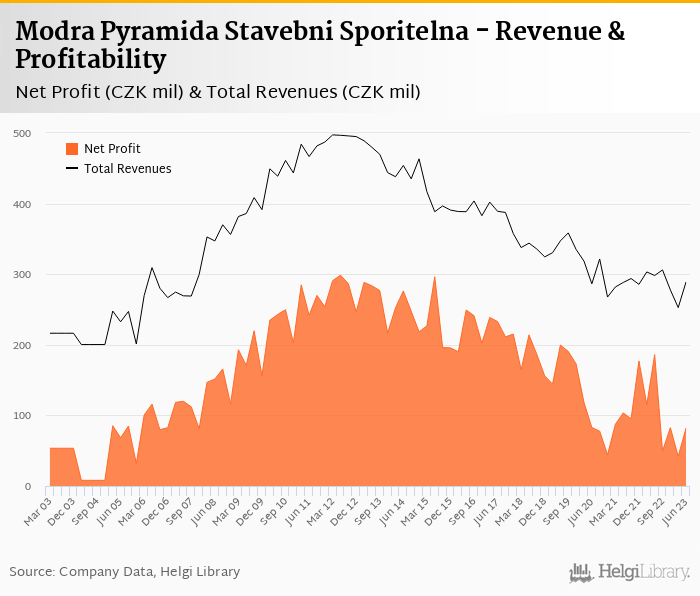

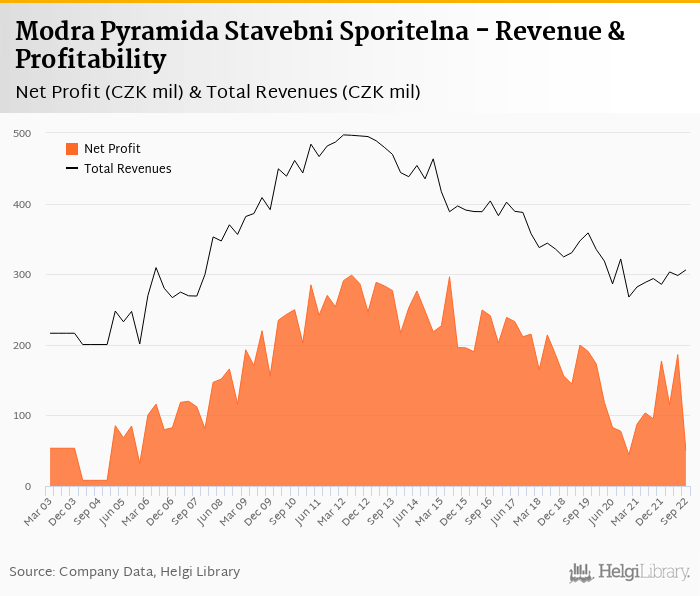

Modra Pyramida Stavebni Sporitelna's net profit fell 59% to CZK 82.3 mil in 2Q2023 due mainly to an absence of CZK 121 mil extra gain made last year.

Operating profit fell by a third as revenues decreased 3.04% due to weak interest income and cost rose hefty 21.3% thanks to staff cost. Cost to income therefore increased to 73.4%

The Bank wrote back another CZK 27.6 mil in provisions, so we expect the NPL ratio fell below 1.0%.

Loan momentum remains good rising 2.3% qoq, though loan to deposit ratio rising to 166% is something to watch for

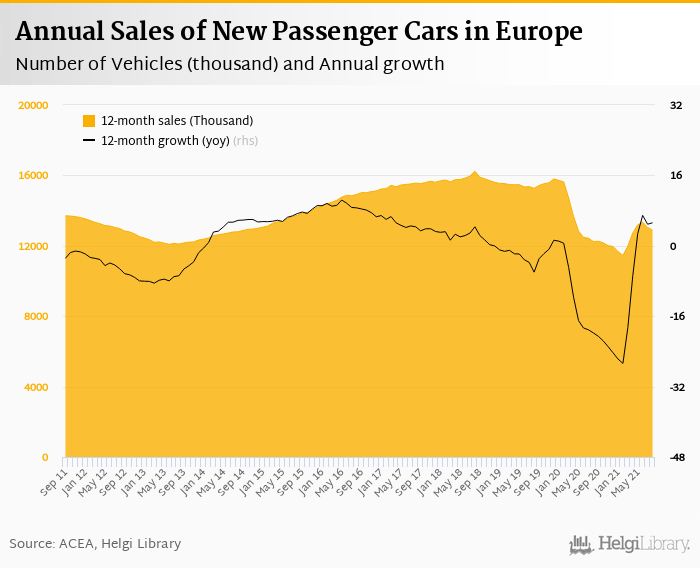

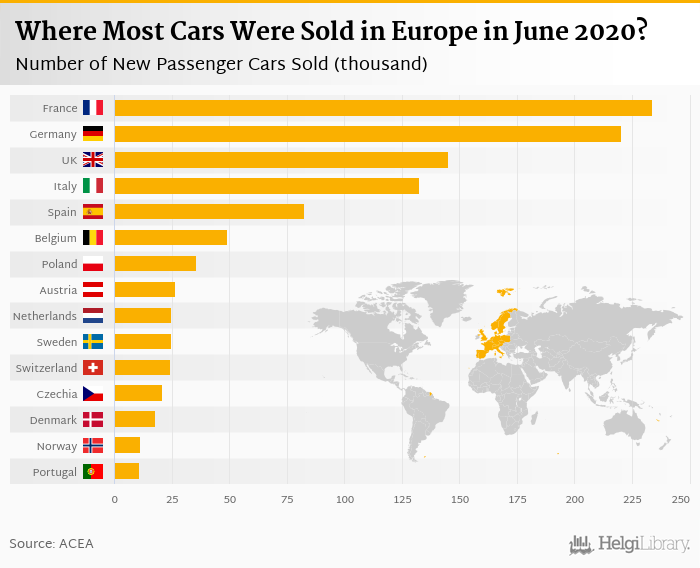

Sales of new cars in Europe increased in July by 16.9% to 1.02 mil. In the first seven months of the year, the growth reached 17.6% totalling 6.3 mil units. This is still 22% lower than in 2019.

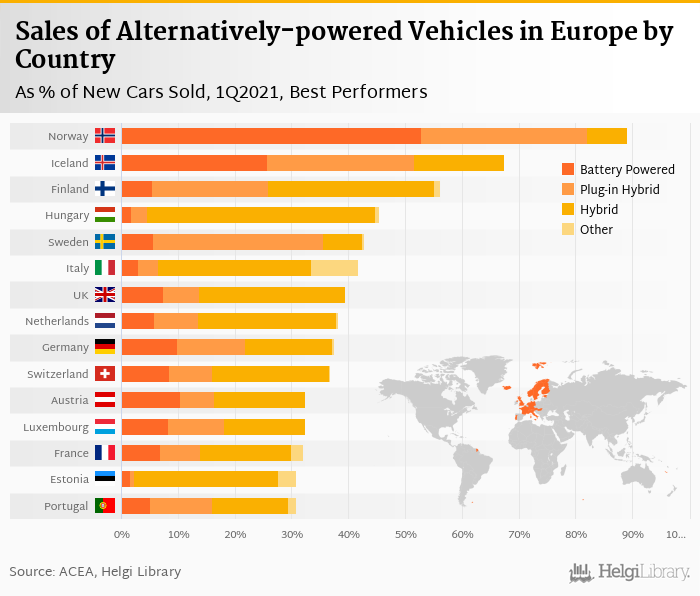

Some 13.6% of the new cars sold were battery-electric cars in July 2023.

Most vehicles (243 thousand) were sold in Germany (up 18.1% yoy), followed by the United Kingdom (144 thousand, up 28.3%) and France with 129 thousand cars (up 19.9%).

Volkswagen Group sold the most cars in July 2023 in Europe, some 280 thousand vehicles representing 27.4% of the European market

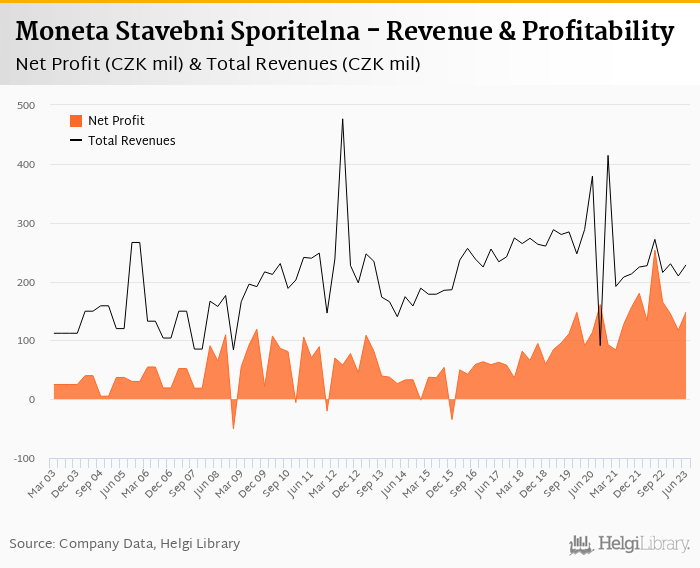

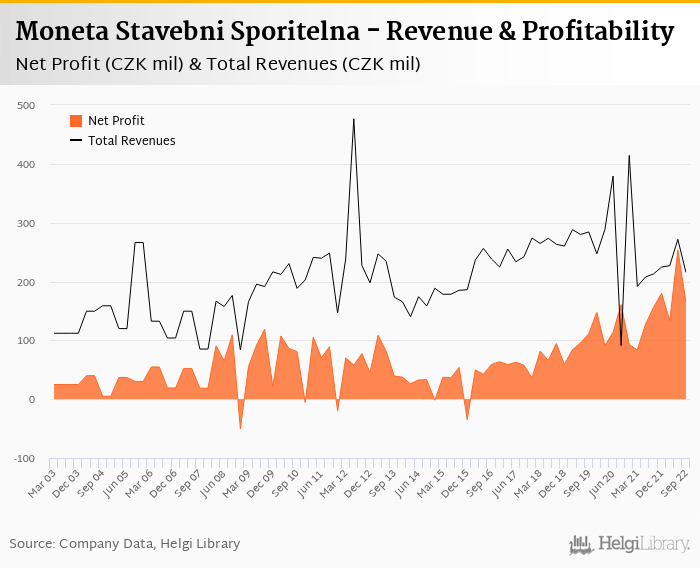

Moneta Stavebni Sporitelna decreased its net profit 41.5% to CZK 148 mil in 2Q2023 and generated ROE of 21.7%.

Revenues decreased 15.9% yoy and cost rose 6.51%. Still, cost to income reached impressive 18.5%

Cost of risk amounted only 0.1%, so we assume asset quality remained good.

The Bank seems to have paid out CZK 556 mil in dividends, so capital adequacy might have dropped to 13-14.0%

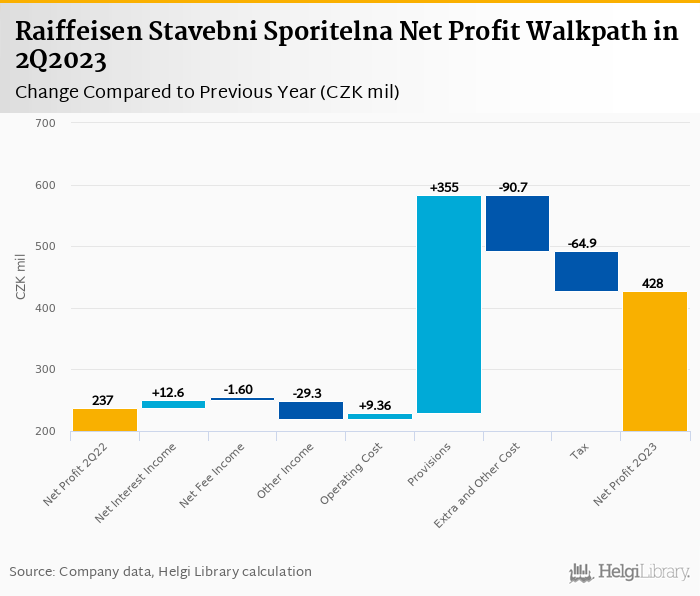

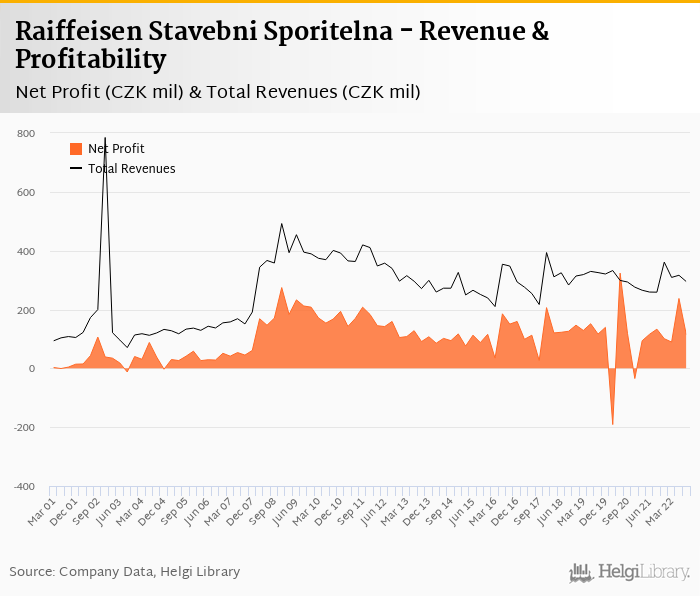

Raiffeisen Stavebni Sporitelna rose its net profit 80% to CZK 428 mil in 2Q2023 and generated ROE of 24.6%.

Revenues decreased 5.8% yoy due to absence of last year's trading gains but cost fell 6.14%, so cost to income decreased to 48.0%

CZK 374 mil provision write-back boosted profitability and generated 70% of the Bank's profit.

Loan to deposit ratio increased to 120% and capital adequacy increased to around 21.5%

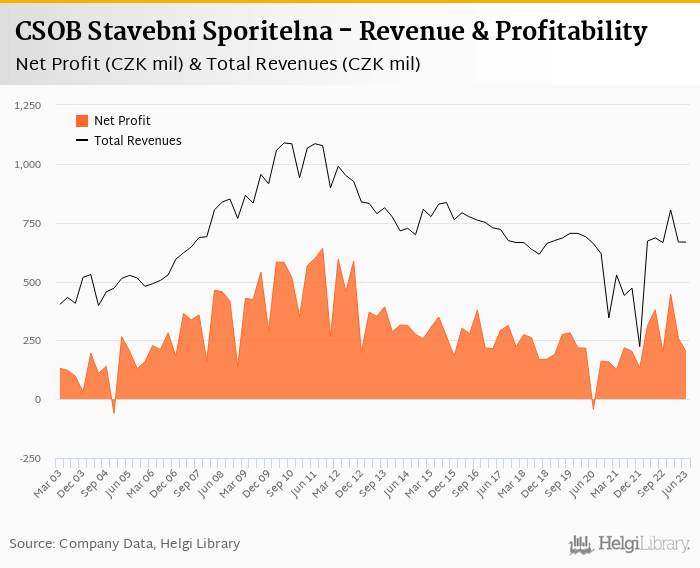

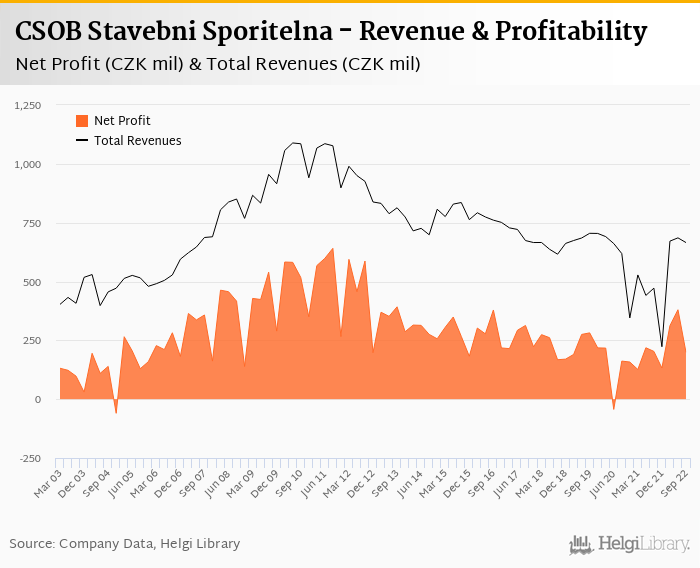

CSOB Stavebni Sporitelna decreased its net profit 47% to CZK 201 mil in 2Q2023 and generated ROE of 8.97%.

Revenues decreased 2.64% yoy and cost rose 14.8%, so cost to income increased to 47.1%

Cost of risk increased to 0.32% and we assume NPL ratio has reached approximately 1.6%.

Loan to deposit ratio increased to 99% and capital adequacy might have fallen to 22-23% as dividends have been paid out

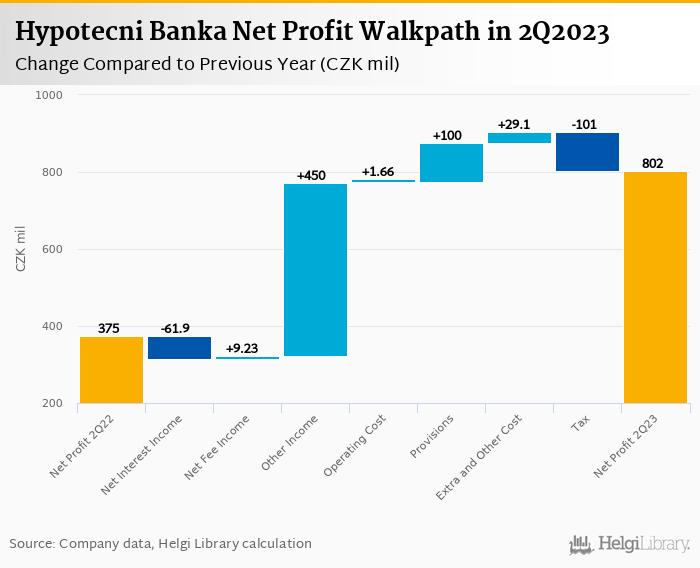

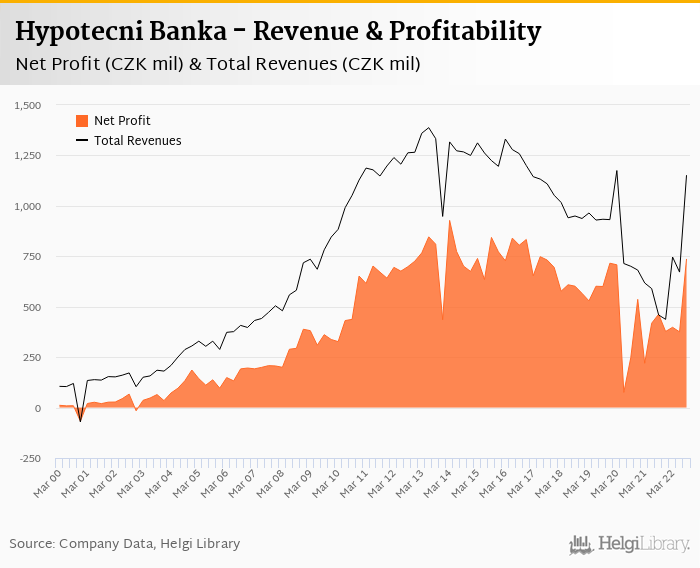

Hypotecni Banka rose its net profit 114% to CZK 802 mil in 2Q2023 and generated ROE of 5.60%.

Revenues increased 59.1% yoy thanks to hedging gains and cost fell 1.12%, so cost to income decreased to 13.7%

Asset quality remains very good and the Bank released further provisions boosting bottom line.

We assume capital adequacy stayed above 50%. When adjusted to 15%, the Bank generated ROE of 18.8% in 2Q2023.

Fio banka announced another record-breaking net profit of CZK 1,52 bil in 2Q2023 implying ROE of 41.8%.

Higher interest margin was again driving the impressive results and pushed revenues 35.3% up. Cost rose 22.1% yoy, so cost to income decreased to 16.0%

Cost of risk amounted relatively high 1.37%. Having no details on asset quality, we suspect management might just have added an extra buffer to its books.

Loan form around a fifth of deposits and capital adequacy might have increased to 33-35%

PKO BP rose its net profit 39.4% to PLN 587 mil in 2Q2023 and generated ROE of 5.86%.

Revenues increased 17.0% yoy driven by higher margins and cost rose 17.6% when adjusted, so cost to income decreased to impressive 30.2%

Cost of risk amounted to hefty 4.5% as PLN 2.74 bil of further provisions for CHF-mortgages were created, though underlying asset quality remains good.

Loan to deposit ratio decreased to 64.5% and capital adequacy increased to strong 19.8%

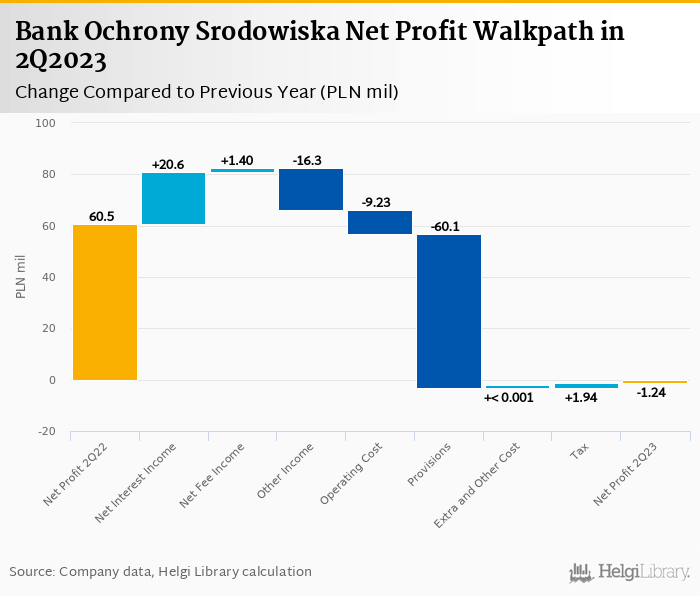

Bank Ochrony Srodowiska made a loss of PLN 1.24 mil in 2Q2023 implying ROE of -0.24%.

Revenues increased 2.2% yoy and adj. cost rose 14.4%, so cost to income increased to 45.8%

Cost of risk amounted 5.0% as PLN 119 mil of provisions were created for CHF-mortgage portfolio.

Loan to deposit ratio decreased to 54.9% and capital adequacy increased to 16.1%

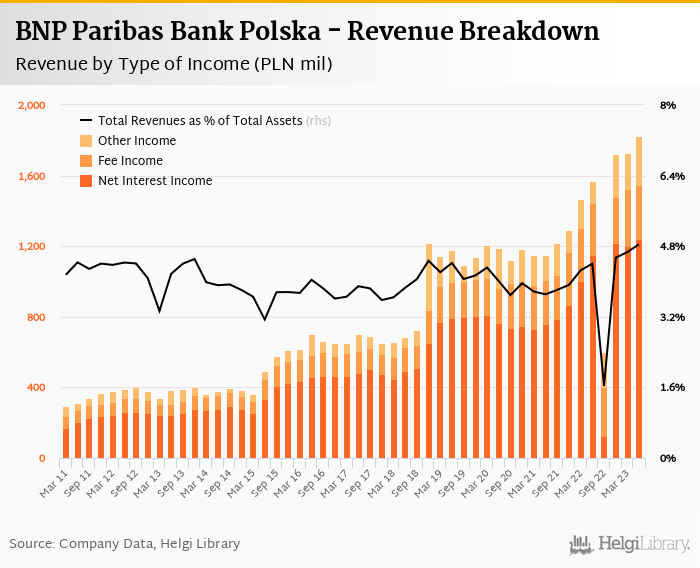

BNP Paribas Bank Polska announced strong net profit of PLN 460 mil in 2Q2023 implying ROE of 14.9%.

Revenues increased 16.4% yoy and cost rose only 7.2%, so cost to income fell below 40%

Cost of risk was high at 1.50% due to further provisioning for CHF-mortgages, though overall asset quality remains good.

Loan to deposit ratio decreased to 74.5% and capital adequacy increased to 16.4%

Raiffeisenbank Czech Republic decreased its net profit 17.0% to CZK 1.5 bil in 2Q2023 and generated ROE of 11.4%.

Revenues decreased 1.1% yoy, but cost fell impressive 6.9%, so cost to income decreased to 44.0%

Asset quality improved with bad loans falling to 1.45% and provision coverage rose to 76%.

Strong liquidity and capital with loan to deposits at 66.5% and capital adequacy at 25.0%

Alior Bank made a record net profit of PLN 506 mil in 2Q2023 implying ROE of 27.7%.

Strong interest margin, absence of contribution to Guarantee Fund and lower provisions were the main drivers

Asset quality continues to improve with NPL ratio falling to 9.74% and cost of risk at 1.05%.

Loan to deposit ratio increased to 82.6% and capital adequacy increased to 15.1%

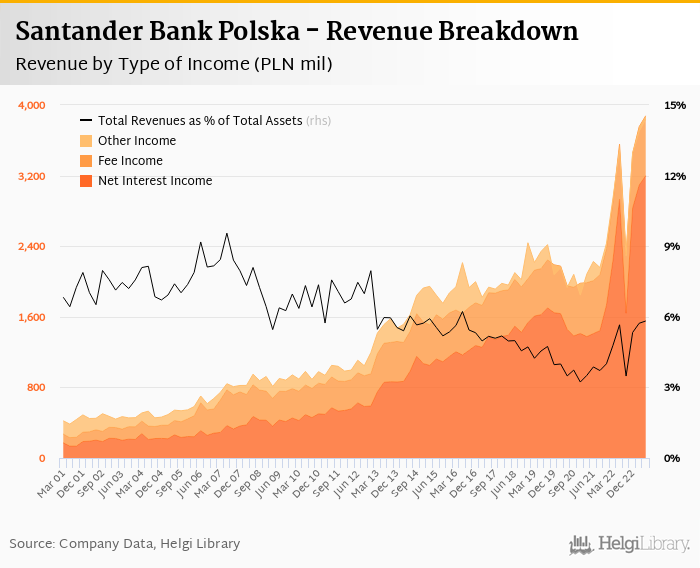

Santander Bank Polska rose its net profit 72% to PLN 1,130 mil in 2Q2023 and generated ROE of 14.0%.

Revenues increased 10.1% yoy and cost fell 21.0%, so cost to income decreased to 26.8%

Cost of risk amounted 2.8% as bad loans rose to 4.28% of total loans

Loan to deposit ratio decreased to 78.2% and capital adequacy increased to 20.8%

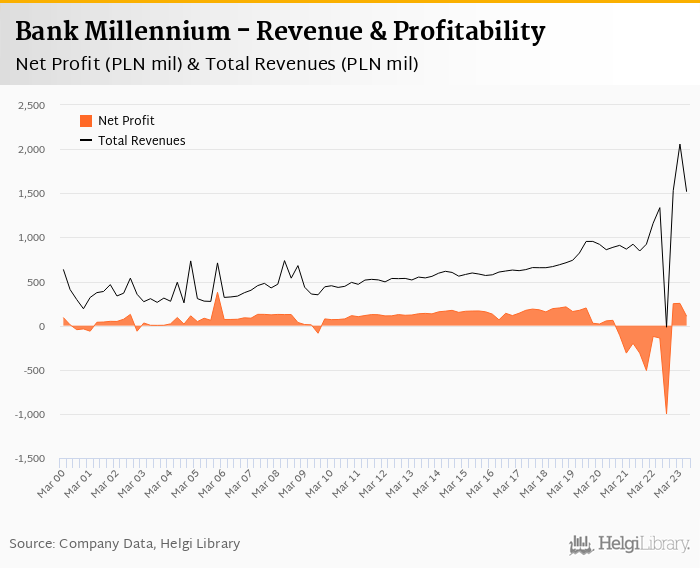

Bank Millennium made a third consecutive quarterly profit and netted PLN 106 mil in 2Q2023

Revenues increased 13.5% yoy and cost rose 21.0% when adjusted translating into cost to income of 31%

Asset quality remains an issue as cost of risk amounted 4.2%. But, provision coverage increased.

Loan to deposit ratio decreased to 73.7% and capital adequacy decreased to 14.8%

ING Bank Slaski almost doubled its net profit to PLN 1.1 bil in 2Q2023 and generated ROE of 36.3%.

Strong operating profitability with cost to income at to 39% as revenues rose 11% yoy and cost increased 9% when adjusted

Bad loans rose to 2.59% of total loans and cost of risk amounted 0.50%, but provision coverage remains solid

With loan to deposit at 78% and capital adequacy at 17.0%, the Bank has a plenty of room to continue strenghtening its market position

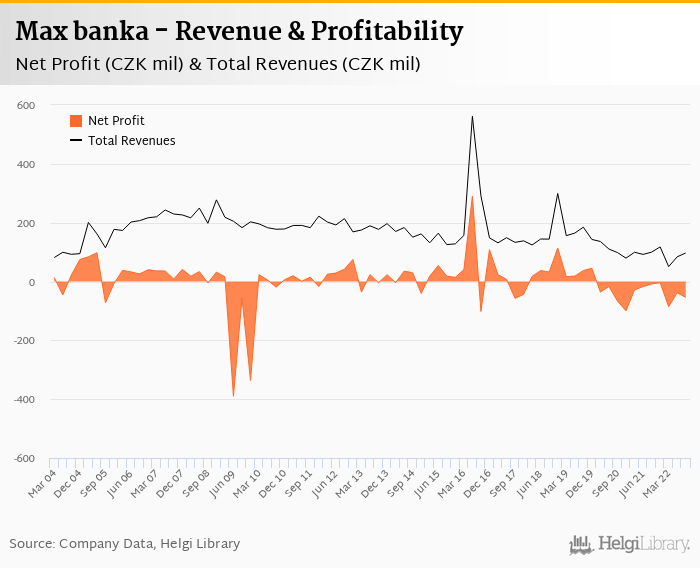

Max banka posted a record net profit CZK 89.3 mil in 2Q2023 and generated ROE of 13.9%.

Revenues more than doubled as deposits increased four-fold. Cost fell 9.7%, so cost to income decreased to 64.1% from more than 100% last year.

With almost 90% of its assets placed with Central Bank and 97% of its revenues coming from interest income, further challenges lay ahead.

With loan to deposit at 7.9% and capital adequacy in access of 30%, the Bank is well positioned to address the asset side when the interest rate differential narrows.

UniCredit Bank Czecho-Slovakia rose its net profit 27.0% to CZK 2,761 mil in 2Q2023 and generated ROE of 15.1%.

The increase in net profit came mainly from stronger trading income, CZK 156 mil reverse on contribution to Depository Fund and lower provision

Adjusted for the contribution, operating profit would have still increase by 18.7% and cost to income ratio would reach impressive 35% in 2Q23

Loan to deposit ratio increased to 72.9% and we estimate capital adequacy reached around 22.5%

Banka Creditas rose its net profit 150% to CZK 223 mil in 2Q2023 and generated ROE of 11.8%.

With flat operating profit and increase in provisons, the jump in profits came mainly from contribution of subsidiaries.

Cost of risk amounted 0.27%, so we assume bad loans fell to 4.5-5.5% of total loans.

With loan to deposit ratio at around 32% and capital adequacy at app. 24%, the Bank is well positioned to grab more of the market.

Trinity Bank rose its net profit 10.4% yoy to CZK 196 mil in 2Q2023 and generated ROE of 15.6%.

Revenues increased 12.1% yoy, but cost rose 39.0% due to a jump in non-personnel. Cost to income increased to still solid 44.2%

Lower provisions were the main profit driver when compared to last year. Cost of risk amounted to 0.043% only, so we assume bad loans fell further to 4.0-4.5% of total loans.

With loan to deposit ratio at 26% and capital adequacy at around 23%, the Bank is well positioned for loan expansion.

CSOB rose its net profit 6.9% to CZK 5,847 mil in 2Q2023 and generated impressive ROE of 22.1%. The strong profits have been achieved heavily by provision write-backs and lower effective tax rate, however.

Operating profit fell 19% yoy due mainly to lower interest margin, though strong fee income and good cost control are worth mentioning helping the bank to keep costs below 50% of income.

CZK 1.26 bil provision write-back for corporate and SME customers saved the day and Bank's bottom line. Share of bad loans fell to 1.52% of total loans.

Weak loan demand and on-going market share losses are worth watching in the near future.

mBank announced strong set of 2Q23 results in spite of the headline losses.

Revenues increased by a quarter thanks to strong interest income, on the other hand, wage and inflationary pressures are something to watch for. Still, adjusted cost to income of below 30% is very impressive

The Bank created further PLN 1.5 bil of provisions for CHF-mortgages, though underlying trends in asset quality seem positive

Management's focus on margin maximising helps ROE to approach 30% level, though market share losses in retail and corporate deposits are something to watch for.

Raiffeisen Bank Int. decreased its net profit 54.5% to EUR 578 mil in 2Q2023 and generated ROE of 13.0%. When excluding for a sale of Bulgarian unit last year, the fall would have been around 22%.

The results were somewhat disappointing on the operating level due to weak fee income generation, though provision write-backs saved the day and bottom line this quarter.

The management slightly upgraded its profit guidance the Bank to generate core ROE of 10% and to operate with cost to income ratio of 51-53% in 2023.

Raiffeisen Int. remains "dirt-cheap" stock trading at adj. PE of 6-7x and at less than half of its book value in 2023/2024. Waiting for a disposal of Russian assets remains a key catalyst.

mBank Czech Republic served almost 750,000 customers in the middle of 2023 through a network of 32 light branches and mKiosks

From almost 2.0% market share in retail lending and deposits in 2021, the Bank has been losing its market position since 2022

In the middle of 2023, the Bank held 1.51% share in consumer, 1.15% in mortgage lending and 1.39% in retail deposits

Average balance on deposits has been stagnating at around CZK 90,000 per account since 2021

Erste Group Bank rose its net profit 30.2% to EUR 896 mil in 2Q2023 and has beaten market expectations by 15-20%.

Higher than expected interest income, a few one-offs and lower than expected cost of risks are behind the strong performance

Management upgraded its 2023 profit guidance with ROTE of >15% and announced a EUR 300 mil share byuback programme.

Trading at PE of around 7.0x, PBV of 0.8x and offering potential dividend yield of 8-10%, Erste Bank share looks attractive.

Pekao's profits more than trippled to PLN 1,693 mil in 2Q2023 and the Bank generated ROE of 26.5%.

Revenues increased 24.5% yoy fuelled by rising margins and trading income while cost fell 22%, due to a fall in regulatory costs.

Cost of risk increased, but was only a half compared to last year on lower provisioning on CHF-mortgages.

Capital adequacy increased to 17.1% and Pekao came out as the most stress-resistant bank out of 70 banks participating in the EBA stress test.

Komercni Banka decreased its net profit 5.96% to CZK 4,525 mil in 2Q2023 and generated ROE of 14.7%.

Operating profitability got under increased pressure as cost of funding bites into margin, demand for loans remains low and inflation pushes costs up.

Asset quality remains very good and saves the date with further provision write-backs. Profitability therefore remains strong profitability and capital buffer high enough the Bank to continue in its generous dividends policy.

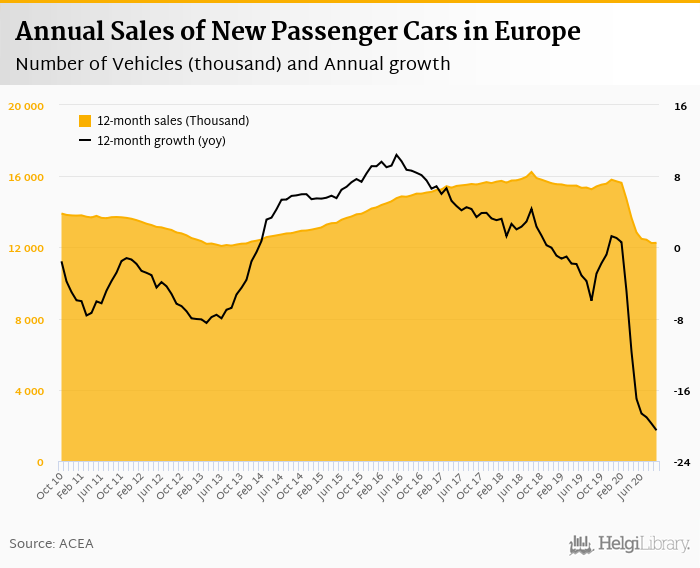

Sales of new cars increased by 200 thousand in June compared to last year

In the first six months of the year, the growth reached 17.7% yoy

Belgium performed relatively the best (up 48.7% yoy) while sales in Hungary showed the weakest change compared to the last year (down 1.40% yoy)

Ceska Sporitelna decreased its net profit 1.58% to CZK 5,988 mil in 2Q2023 and generated ROE of 17.4%.

The operating profit fell almost 10% yoy as higher interest rates have been eating into interest margin and high inflation pushes operating costs higher. Also, cost of risk increased by more than a CZK 1.1 bil yoy due mainly to last year’s provision write-back.

The main positives therefore came from non-core items such as other operating income and lower effective tax rate from expected windfall tax.

Good asset quality, pick up in loan demand and market share increase are other positives worth mentioning.

MONETA Money Bank decreased its net profit 20.2% to CZK 1,263 mil in 2Q2023 and generated ROE of 16.4%.

Revenues decreased 1.24% yoy and cost rose 7.61%, so cost to income increased to 45.3%

Bad loans fell to 1.31% of total loans and cost of risk amounted 0.219%.

Loan to deposit ratio decreased to 72.8% and capital adequacy increased to 19.7%

Czech banks decreased net profit 10.1% yoy to CZK 21,116 mil in the first quarter of 2023 and generated ROE of 11.9%.

Operating income fell 5.78%, cost to income increased to 36.7% and banks' share of bad loans fell to 1.90%.

CSOB generated the biggest profit while Modra Pyramida Stavebni Sporitelna produced the smallest one.

Sales of new cars increased by 173 thousand in May compared to last year

In the first five months of the year, the growth reached 17.4% yoy

Croatia performed relatively the best (up 74.3% yoy) while sales in Hungary showed the weakest change compared to the last year (down 11.3% yoy)

Sales of new cars increased by 295 thousand in March compared to last year

In the first three months of the year, the growth reached 17.5% yoy

Cyprus performed relatively the best (up 109% yoy) while sales in Bulgaria showed the weakest change compared to the last year (down 14.4% yoy)

Sales of new cars increased by 98.7 thousand in February compared to last year

In the first two months of the year, the growth reached 11.5% yoy

Romania performed relatively the best (up 44.5% yoy) while sales in Sweden showed the weakest change compared to the last year (down 12.7% yoy)

Sales of new cars increased by 88.6 thousand in January compared to last year

Greece performed relatively the best (up 90.8% yoy) while sales in Norway showed the weakest change compared to the last year (down 76.6% yoy)

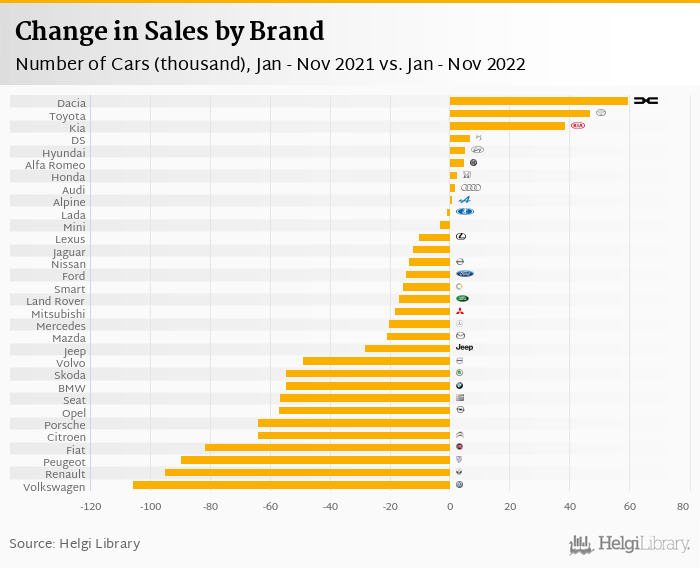

Sales of new cars increased by 151 thousand in November compared to last year

In the first eleven months of the year, the decline reached 5.81% yoy

Latvia performed relatively the best (up 73.6% yoy) while sales in Ireland showed the weakest change compared to the last year (down 12.5% yoy)

Moneta Stavebni Sporitelna rose its net profit 5.7% to CZK 165 mil in 3Q2022 and generated ROE of 25.4%.

Revenues increased 1.19% yoy and cost rose 150%, so cost to income increased to 21.2%

Cost of risk was again negative at -0.783% of loans and loan to deposit ratio increased to 55.3%

CSOB Stavebni Sporitelna decreased its net profit 2.0% to CZK 199 mil and generated ROE of 9.52%.

Revenues increased 41.0% yoy and cost rose 3.99%, so cost to income decreased to 47.8%

Cost of risk amounted 0.320% and loan to deposit ratio increased to 97.0%

Modra Pyramida decreased its net profit 48% to CZK 49.5 mil in 3Q22 and generated ROE of 3.0%.

Revenues increased 4.18% yoy and cost fell 3.67%, so cost to income decreased to 50.0%

Cost of risk amounted 0.46% and loan to deposit ratio increased to 150%

Raiffeisen Stavebni Sporitelna decreased its net profit 14.2% to CZK 114 mil with ROE of 7.9%.

Revenues increased 13.9% yoy and cost fell 15.5%, so cost to income decreased to 45.3%

Cost of risk amounted 0.123% and loan to deposit ratio increased to 113%

Stavebni Sporitelna Ceske Sporitelny doubled its net profit to CZK 260 mil with ROE of 13.7%.

Revenues increased 17.9% yoy and cost rose 3.07%, so cost to income decreased to 23.8%

Cost of risk amounted 0.059% and loan to deposit ratio increased to 99.5%

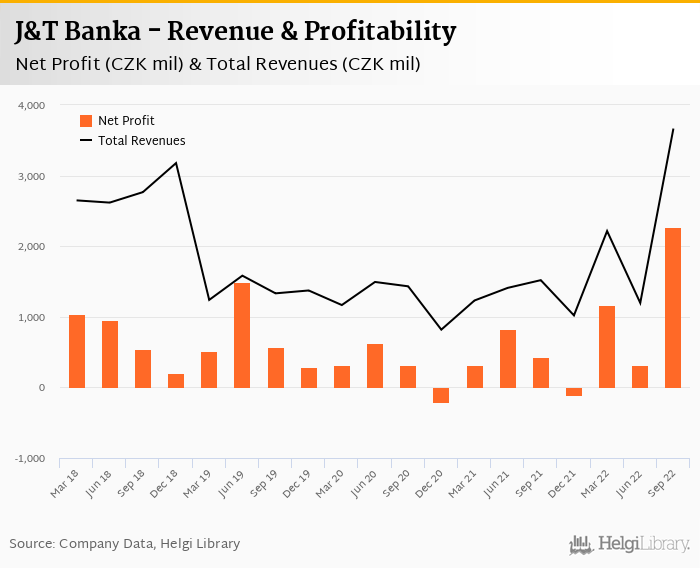

J&T Banka produced a record net profit of CZK 2,277 mil in 3Q2022 with ROE of 32.2%.

Revenues increased 141% yoy and cost rose 10.5%, so cost to income decreased to 19.2%

Cost of risk amounted 0.537% and loan to deposit ratio increased to 34%

Max banka increased its net loss to CZK 54.2 mil in 3Q2022 and generated a negative ROE of 10.8%.

Revenues decreased 2.9% yoy and cost rose 22.1%, so cost to income increased to 144%

Cost of risk increased to 0.983% and loan to deposit ratio decreased to 49.4%

PPF Banka almost doubled its net profit to CZK 746 mil in 3Q2022 with ROE of 18.8%.

Revenues increased 78% yoy and cost rose 0.685%, so cost to income decreased to 25.6%

Cost of risk amounted 1.60% and loan to deposit ratio decreased to 28.1%

Fio banka has doubled its net profit to CZK 1.27 bil in 3Q22 generating ROE of 48.7%.

Revenues increased 79.8% yoy and cost rose 18.6%, so cost to income decreased to 17.1%

Cost of risk amounted 0.517% and loans to deposit ratio increased to 18.2%

Air Bank reported record numbers in 3Q2022 with CZK 727 mil net profit and ROE of 25.2%.

Revenues increased 69.1% yoy and cost rose 22.6%, so cost to income decreased to only 33.8%

Cost of risk increased to 1.05% while loan to deposit ratio increased to 56.6%

Hypotecni Banka's net profit rose 59.2% to CZK 737 mil in 3Q2022, the highest figure since 2017

Revenues increased 151% yoy thanks to rising interest rates and other income, cost fell 4.85%

Cost of risk amounted to only 0.091% amid limited asset quality concerns

Banka Creditas booked a record net profit of CZK 1,450 mil in 3Q2022 heavily driven by extra profit

Excluding the one-off, revenues increased 144% yoy, cost rose 7.38% and operating profit reached all-time high of CZK 254 mil

Cost to income decreased to 48.1%and underlying ROE would have reached of 13.6%

Trinity Bank increased its net profit 5-fold to CZK 316 mil in 3Q2022 and generated ROE of 38.8%.

Revenues increased 239% yoy and cost rose 65.2%, so cost to income decreased to 26.3%

Cost of risk amounted 0.339% of loans and loan to deposit ratio decreased to 19.8%

Sales of new cars increased by 23.0 thousand in October compared to last year

In the first ten months of the year, the decline reached 8.72% yoy

Latvia performed relatively the best (up 61.3% yoy) while sales in Slovenia showed the weakest change compared to the last year (down 18.7% yoy)

Raiffeisenbank Czech Republic showed a record net profit of CZK 2,457 mil in 3Q2022 and generated ROE of 20.5%.

Revenues increased 49.7% yoy and cost rose 26.0%, so cost to income decreased to 45.8%

Loan to deposit ratio increased to 71.3% and capital adequacy might have decreased to 20.4%

UniCredit Bank Czecho-Slovakia decreased its net profit 3.04% yoy to CZK 2,104 mil in 3Q2022 and generated ROE of 11.6%.

Revenues increased 2.21% yoy and cost rose 2.10%, so cost to income decreased to 45.6%

Loan to deposit ratio decreased to 65.2% and capital adequacy increased to 22.7%

CSOB decreased its net profit 14.5% to CZK 4,241 mil in 3Q2022 and generated ROE of 17.3%.

Revenues increased 17.5% yoy and cost rose 13.7%, so cost to income decreased to 47.3%

Bad loans fell to 1.36% of total loans and cost of risk amounted 0.277%.

Loan to deposit ratio increased to 83.0% and capital adequacy decreased to 19.6%

MONETA Money Bank decreased its net profit 14.7% to CZK 1,251 mil in 3Q2022 and generated ROE of 17.0%.

Revenues increased 8.67% yoy and cost rose 7.45%, so cost to income decreased to 44.9%

Bad loans fell to 1.40% of total loans and cost of risk amounted 0.186%.

Loan to deposit ratio decreased to 83.8% and capital adequacy decreased to 17.0%

Ceska Sporitelna decreased its net profit 4.54% to CZK 4,020 mil in 3Q2022 and generated ROE of 12.5%.

Revenues increased 15.9% yoy and cost rose 9.28%, so cost to income decreased to 42.7%

Bad loans fell to 1.90% of total loans and cost of risk amounted 0.357%.

Loan to deposit ratio increased to 66.1% and capital adequacy decreased to 19.9%

Komercni Banka rose its net profit 32.8% to CZK 4,650 mil in 3Q2022 and generated ROE of 14.6%.

Revenues increased 25.8% yoy and cost rose 3.80%, so cost to income decreased to 37.2%

Bad loans fell to 2.27% of total loans and cost of risk amounted 0.349%.

Loan to deposit ratio increased to 69.3% and capital adequacy decreased to 21.1%

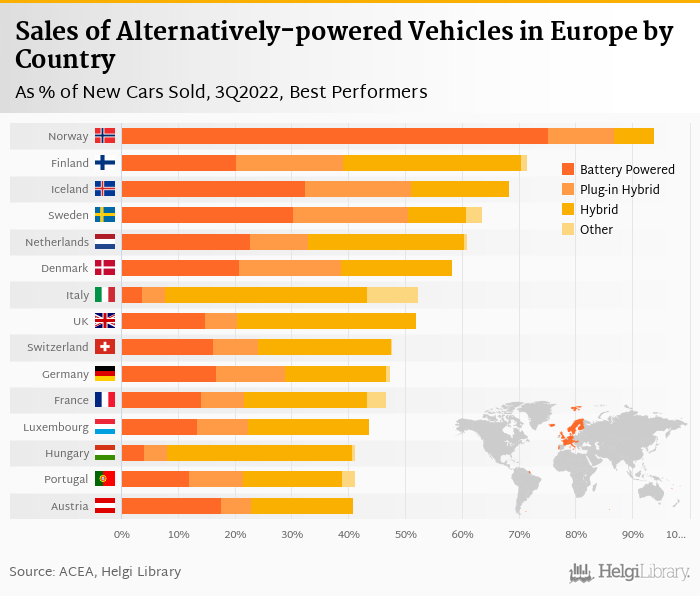

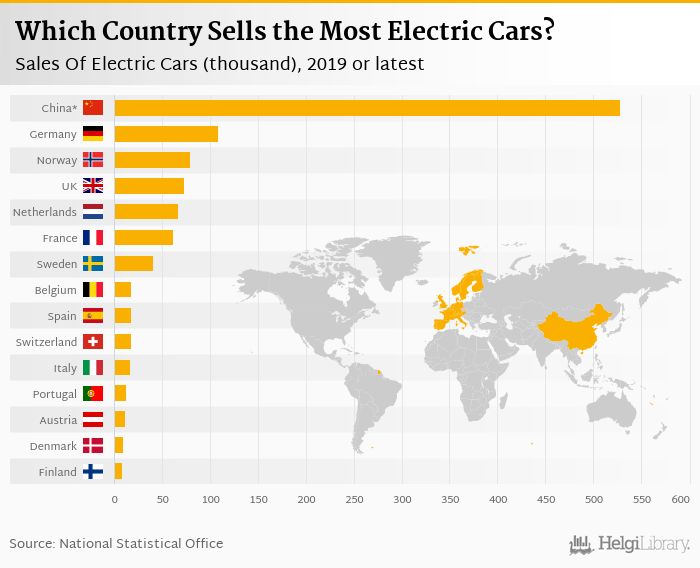

Sales of electrically-chargeable vehicles amounted to 555 thousand in 3Q2022, 21.5 thousand more than the last year.

Electric cars represented 23.2% of all new cars sold in 3Q2022, up from 22.4% a year ago.

Most electric vehicles have been sold in Germany (182 thousand), while Cyprus registered the biggest increase in sales when compared to last year.

Czech banks increased net profit 53.7% yoy to CZK 31,133 mil in the second quarter of 2022 and generated ROE of 18.2%.

Operating income rose 26.3%, cost to income dropped to 40.3% and banks' share of bad loans fell to 2.27%.

Ceska Sporitelna generated the biggest profit while Max banka produced the biggest loss in 2Q2022.

Sales of new cars increased by 77.2 thousand in September compared to last year

In the first nine months of the year, the decline reached 9.73% yoy

Bulgaria performed relatively the best (up 46.4% yoy) while sales in Norway showed the weakest change compared to the last year (down 18.6% yoy)

Sales of new cars increased by 24.2 thousand in August compared to last year

In the first eight months of the year, the decline reached 11.8% yoy

Portugal performed relatively the best (up 42.4% yoy) while sales in Norway showed the weakest change compared to the last year (down 24.7% yoy)

Sales of new cars decreased by 104 thousand in July compared to last year

In the first seven months of the year, the decline reached 13.3% yoy

Portugal performed relatively the best (up 17.6% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 34.3% yoy)

Sales of new cars decreased by 216 thousand in June compared to last year

In the first six months of the year, the decline reached 13.7% yoy

Iceland performed relatively the best (up 35.7% yoy) while sales in Croatia showed the weakest change compared to the last year (down 28.4% yoy)

Sales of electrically-chargeable vehicles amounted to 545 thousand in 2Q2022, -18.8 thousand less than the last year.

Electric cars represented 21.4% of all new cars sold in 2Q2022, up from 18.4% a year ago.

Most electric vehicles have been sold in Germany (155 thousand), while Romania registered the biggest increase in sales when compared to last year.

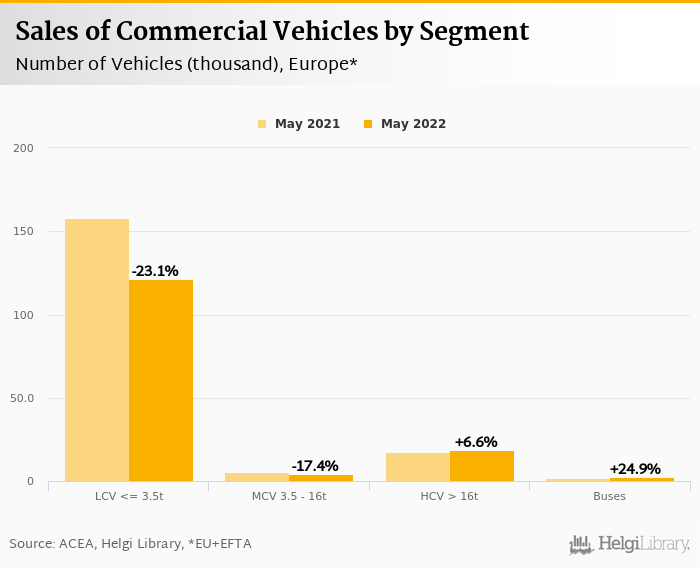

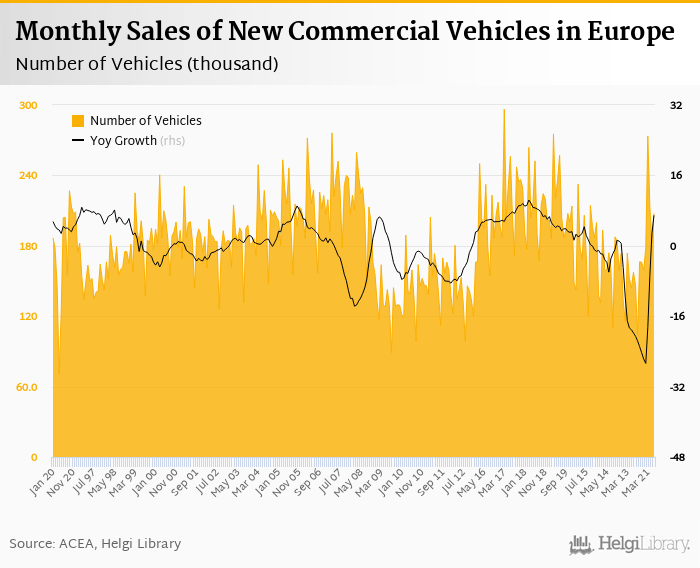

Sales of new commercial vehicles reached 147 thousand in May 2022 in the enlarged Europe (EU plus Iceland, Norway and Switzerland), according to ACEA. This is 19.5%, or 35.6 thousand fewer than in the previous year.

Historically, between January 1997 and May 2022, sales of commercial vehicles in Europe reached a high of 296 thousand in March 2017 and a low of 71.0 thousand in April 2020.

So far this year, some 740 thousand vehicles were sold in Europe, down 27.8% yoy.

Sales of new cars decreased by 136 thousand in May compared to last year

In the first five months of the year, the decline reached 12.9% yoy

Iceland performed relatively the best (up 65.9% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 33.1% yoy)

Sales of electrically-chargeable vehicles amounted to 548 thousand in 1Q2022, 101 thousand more than the last year.

Electric cars represented 22.1% of all new cars sold in 1Q2022, up from 16.0% a year ago.

Most electric vehicles have been sold in Germany (152 thousand), while Romania registered the biggest increase in sales when compared to last year.

Sales of new cars decreased by 209 thousand in April compared to last year

In the first four months of the year, the decline reached 13% yoy

Iceland performed relatively the best (up 79.6% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 35.0% yoy)

Sales of new cars decreased by 261 thousand in March compared to last year

In the first three months of the year, the decline reached 10.6% yoy

Iceland performed relatively the best (up 51.6% yoy) while sales in Sweden showed the weakest change compared to the last year (down 39.5% yoy)

Sales of new cars decreased by 46.1 thousand in February compared to last year

In the first two months of the year, the decline reached 3.93% yoy

Iceland performed relatively the best (up 47.3% yoy) while sales in Norway showed the weakest change compared to the last year (down 23.8% yoy)

Sales of new cars decreased by 20.4 thousand in January compared to last year

Slovakia performed relatively the best (up 72.6% yoy) while sales in Greece showed the weakest change compared to the last year (down 28.9% yoy)

Sales of electrically-chargeable vehicles amounted to 666 thousand in 4Q2021, 81.8 thousand more than the last year.

Electric cars represented 28.3% of all new cars sold in 4Q2021, up from 19.2% a year ago.

Most electric vehicles have been sold in Germany (204 thousand), while Lithuania registered the biggest increase in sales when compared to last year.

Sales of new cars decreased by 264 thousand in December compared to last year

This year, the decline reached 1.54% yoy

Iceland performed relatively the best (up 53.9% yoy) while sales in Ireland showed the weakest change compared to the last year (down 82.4% yoy)

Sales of new cars decreased by 183 thousand in November compared to last year

In the first eleven months of the year, the growth reached 0.75% yoy

Iceland performed relatively the best (up 73.8% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 59.1% yoy)

Sales of new cars decreased by 331 thousand in October compared to last year

In the first ten months of the year, the growth reached 2.72% yoy

Ireland performed relatively the best (up 16.7% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 54.8% yoy)

Sales of new cars decreased by 327 thousand in September compared to last year

In the first nine months of the year, the growth reached 6.94% yoy

Norway performed relatively the best (up 15.7% yoy) while sales in Lithuania showed the weakest change compared to the last year (down 56.8% yoy)

Sales of new cars decreased by 160 thousand in August compared to last year

In the first eight months of the year, the growth reached 12.7% yoy

Norway performed relatively the best (up 52.1% yoy) while sales in Portugal showed the weakest change compared to the last year (down 35.8% yoy)

Sales of new cars decreased by 303 thousand in July compared to last year

In the first seven months of the year, the growth reached 16.9% yoy

Ireland performed relatively the best (up 24.8% yoy) while sales in Belgium showed the weakest change compared to the last year (down 38.0% yoy)

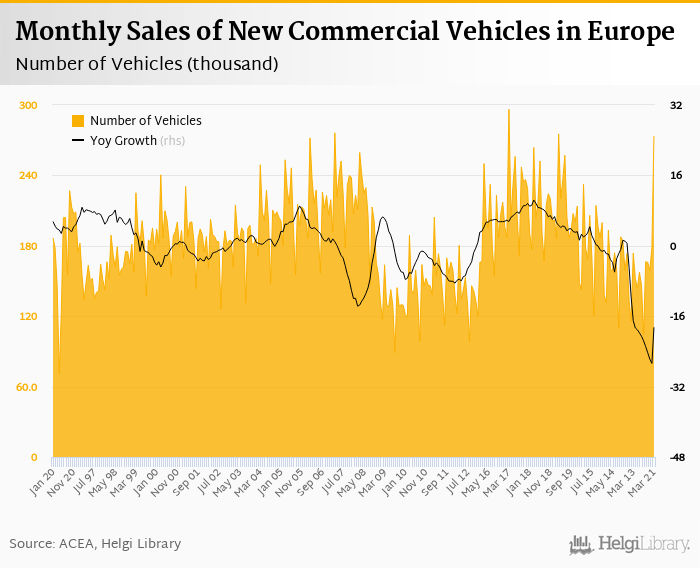

Sales of new commercial vehicles reached 208 thousand in June 2021 in the enlarged Europe (EU plus Iceland, Norway and Switzerland), according to ACEA. This is 1.78%, or 3.62 thousand more than in the previous year.

Historically, between January 1997 and June 2021, sales of commercial vehicles in Europe reached a high of 296 thousand in March 2017 and a low of 71.0 thousand in April 2020.

So far this year, some 1,233 thousand vehicles were sold in Europe, up 35.7% yoy.

Sales of new cars increased by 151 thousand in June compared to last year

In the first six months of the year, the growth reached 27.1% yoy

Ireland performed relatively the best (up 174% yoy) while sales in Slovenia showed the weakest change compared to the last year (down 21.2% yoy)

Sales of new commercial vehicles reached 274 thousand in March 2021 in the enlarged Europe (EU plus Iceland, Norway and Switzerland), according to ACEA. This is 88.1%, or 128 thousand more than in the previous year.

Historically, between January 1997 and March 2021, sales of commercial vehicles in Europe reached a high of 296 thousand in March 2017 and a low of 71.0 thousand in April 2020.

So far this year, some 630 thousand vehicles were sold in Europe, up 23.5% yoy.

Sales of new cars increased by 748 thousand in April compared to last year

In the first four months of the year, the growth reached 23.1% yoy

Italy performed relatively the best (up 3,289% yoy) while sales in Sweden showed the weakest change compared to the last year (up 15.6% yoy)

Sales of electrically-chargeable vehicles amounted to 445 thousand in 1Q2021, 222 thousand more than the last year.

Electric cars represented 15.9% of all new cars sold in 1Q2021, up from 8.10% a year ago.

Most electric vehicles have been sold in Germany (143 thousand), while Cyprus registered the biggest increase in sales when compared to last year.

Sales of electrically-chargeable vehicles amounted to 584 thousand in 4Q2020, 406 thousand more than the last year.

Electric cars represented 19.6% of all new cars sold in 4Q2020, up from 5.35% a year ago.

Most electric vehicles have been sold in Germany (190 thousand), while Slovenia registered the biggest increase in sales when compared to last year.

Sales of new cars increased by 535 thousand in March compared to last year

In the first three months of the year, the growth reached 0.849% yoy

Italy performed relatively the best (up 499% yoy) while sales in Netherlands showed the weakest change compared to the last year (down 18.0% yoy)

Sales of new cars decreased by 47.2 thousand in December compared to last year

This year, the decline reached 24.3% yoy

Ireland performed relatively the best (up 168% yoy) while sales in Croatia showed the weakest change compared to the last year (down 49.5% yoy)

Sales of new cars decreased by 163 thousand in November compared to last year

In the first eleven months of the year, the decline reached 26.1% yoy

Norway performed relatively the best (up 24.9% yoy) while sales in Bulgaria showed the weakest change compared to the last year (down 45.2% yoy)

Sales of new cars decreased by 85.8 thousand in October compared to last year

In the first ten months of the year, the decline reached 27.2% yoy

Norway performed relatively the best (up 23.6% yoy) while sales in Latvia showed the weakest change compared to the last year (down 29.3% yoy)

Sales of new cars increased by 14.6 thousand in September compared to last year

In the first nine months of the year, the decline reached 29.3% yoy

Romania performed relatively the best (up 79.9% yoy) while sales in Bulgaria showed the weakest change compared to the last year (down 27.7% yoy)

Sales of new cars decreased by 190 thousand in August compared to last year

In the first eight months of the year, the decline reached 32.9% yoy

Cyprus performed relatively the best (up 14.1% yoy) while sales in Romania showed the weakest change compared to the last year (down 51.9% yoy)

Sales of new cars decreased by 48.5 thousand in July compared to last year

In the first seven months of the year, the decline reached 34.6% yoy

Iceland performed relatively the best (44.5%) while sales in Romania showed the weakest change compared to the last year (-44.2%)

Sales of electrically-chargeable vehicles amounted to 228 thousand in 1Q2020, up by 101 thousand in 1Q2020 compared to last year

Electric cars represented 7.47% of all new cars sold in 1Q2020, up from 3.06% a year ago.

Most electric vehicles have been sold in Germany (52.4 thousand) while France registered the biggest increase in sales when compared to last year.

Sales of new cars decreased by 359 thousand in June compared to last year

In the first six months of the year, the decline reached 39.4% yoy

The smallest decline was seen in France (1.23%) while sales in Portugal dropped the most (-56.2%)

Sales of new cars decreased by 1,053 thousand in April compared to last year

In the first four months of the year, the decline reached 39% yoy

Norway performed relatively the best (-34.0%) while sales in Italy showed the weakest change compared to the last year (-97.5%)

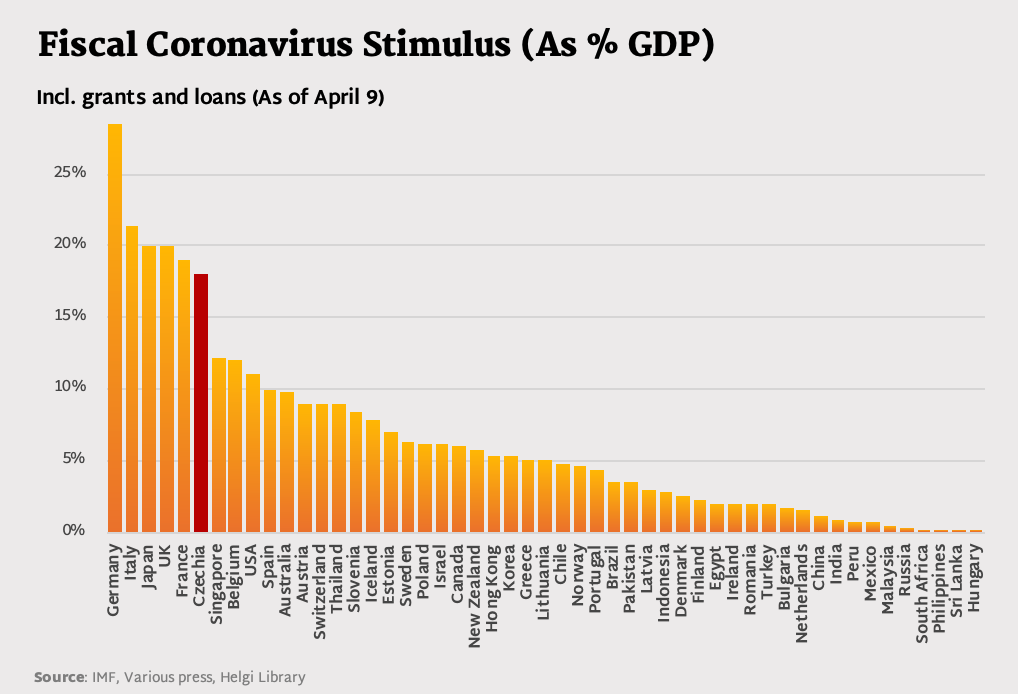

The scale of fiscal support being deployed to fight the Covid-19 economic crisis is huge.

The Czech Government is willing to spend an impressive 20% of GDP, but the what has been accomplished so far is mediocre.

The Government is slow in distributing help to those most in need, lacks expertise and fails to communicate effectively.

Good examples from abroad should be followed, such as teaming up with banks to speed things up.

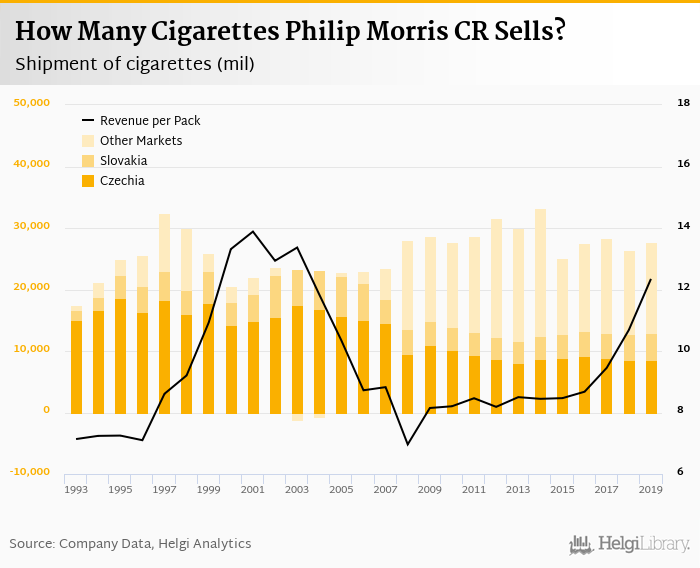

Philip Morris Czech Republic (PMCR) made a net profit of CZK 4,019 mil under sales of CZK 17.1 bil in 2019

The firm might have sold 27,691 mil cigarettes in 2019, on our estimates

We calculate that the company made revenue of CZK 12.3 and a net profit of CZK 2.90 per pack of cigarettes sold in 2019

PMCR held 41.3% share on the domestic Czech market in 2019 and 54.8% share in Slovakia

New study suggests excessive coffee consumption does not cause arteries to stiffen, putting pressure on the heart

You can drink up to 25 cups of coffee a day without increasing the likelihood of having a heart attack or stroke

When drinking coffee, you will still have a bad breath, though...

Wage growth across Central Europe has sped up to 5-10%, closing the gap again with Western peers.

Cheap and skilled labor has been one of the reasons CEE banks are so cost efficient and profitable.

Could fast growth in wages endangers superior profitability of CEE banking?

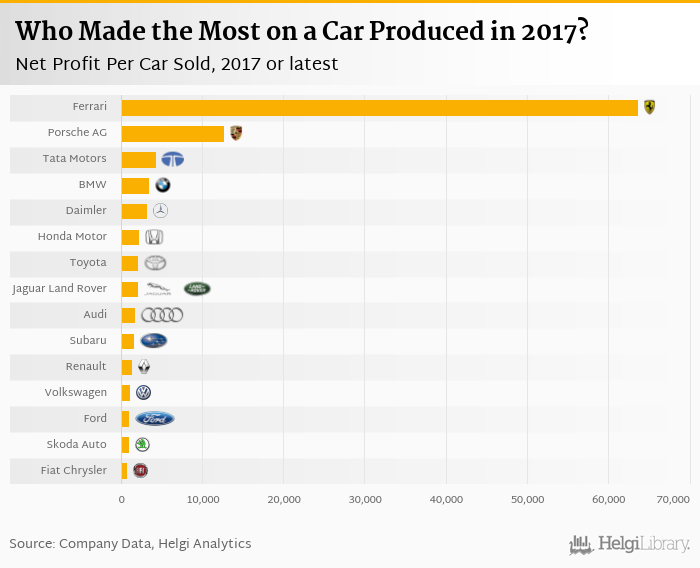

Ferrari earned EUR 63,752 per car sold, five times more than Porsche. On the other hand, Volkswagen created the biggest operating profit in 2017 among car manufacturers.

Toyota was the most valuable automotive Company in the world in 2017 while Tesla remains a different species in the pond.

Instead of tracing what has happened since the first visible incidence of ‘Gulenist movement’ (as named by the AKP) and the two elections that took place last year, we would like to focus on what we believe are the key objectives/positions taken by the main player(s?) of the ruling party. We believe it is clear to the market (hopefully by now) that Turkey is an ‘autocratic democracy’ (an oxymoron): the government is elected through a democratic process with an aim to rule as an autocracy.

Irrespective of the ‘office’ held, Mr. Recep Tayyip Erdogan (currently in the office of a neutral President) wants to rule the country despite holding a ceremonial post. The power in Turkey officially rests in the office of Prime Ministership which is occupied by the leader of the ruling party (currently, Mr. Binali Yildirim).

It is an open secret that President Erdogan is trying to engineer amendments in the constitution to ‘upstream’ power to the presidency and rule the country. His actions so far indicate his desire to control and manage outcomes as he sees fit. This is in line with his interference via commentary on interest rates, prosecutorial activities, and strategy towards PKK and Kurdish elements in Turkey, involvement in Syria, etc.

Contrary to common perception, based on real high frequency data and ‘changes’ that we observe, we believe 1) the economic outlook has changed for the better, 2) the legal infrastructure and reforms re financial sector, especially the NPL is in place, and 3) the banks are in advance stages of planning and implementing reduction of NPLs and restart core banking activities.

Instead of updating on the ‘news of the day/week/month’ and or commenting on how/why and what of the outcome of the Brexit vote, we want to focus on three aspects: 1) how it affects UK and what we believe might happen, 2) what is the likely ‘response’ of EU to this event with respect to EU rather than UK, and, 3) Atmosphere.

For all non-financial companies/businesses that we look at, our primary focus is to get a real sense of a business’s ability to generate sustainably equity free-cash flow (‘E-fcf) given a view of macro-economic and competitive scenario. ‘E-fcf’ yield relative to the cost of ‘funds’ (debt) is one of the primary benchmark to sense the relative attractiveness of the investment under consideration.

To us, sustainability of dividend is of paramount importance, and we use our estimate of ‘e-fcf’ to assess sustainability of dividends: ‘e-fcf’ > dividends is the key. We are okay with the companies retaining some ‘e-fcf’ for ‘rainy-days’ or deleveraging for cyclical cushion. However, companies where we see dividends consistently above ‘E-fcf’ we believe are of poor quality and more akin to ‘equity-release’ rather than ‘equity-return’.

Statistical adjustments caught-up with Greece as the ‘money tap’ started to run dry when the GFC unfolded and the financial institutions started to look at how they can shrink their balance sheets. The Greek government declared that it was running fiscal deficits closer to 10% vs. 3% (as per Maastricht criteria), and approached the EU to ask for a programme and help to put Greek back on sound financial footing. The first EU-IMF-ECB (popularly known as Troika) bailout programme was introduced with an austerity plan requiring expenditure and revenue measures. At the same time, ‘non-Greek’ banks were trying to pull-out from Greece, aggravating the impact of austerity measures (revenue side suffered) as corporate Greece was faced to liquidity squeeze.

Instead of repeating the mantra of why investing in this region has a measurably attractive reward to risk profile, valuations are attractive, the underlying economic outlook has more potential to surprise on the upside etc., we would like to take the opportunity here to demonstrate through an example or ‘investment’ thought process (in a Socratic dialogue format).

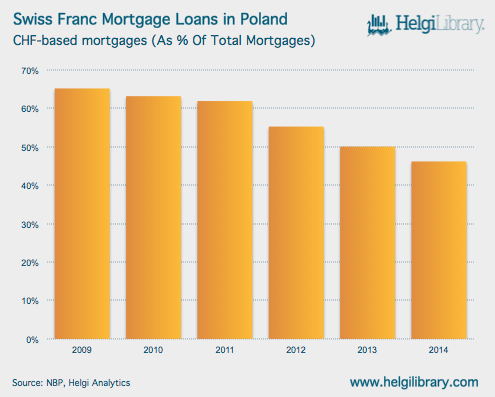

For better or for worse, the issue of CHF mortgages is blown out of proportion and has become a tri-party football match between the banks, the borrowers and the regulator.

There are two Diamond News In November 2015.

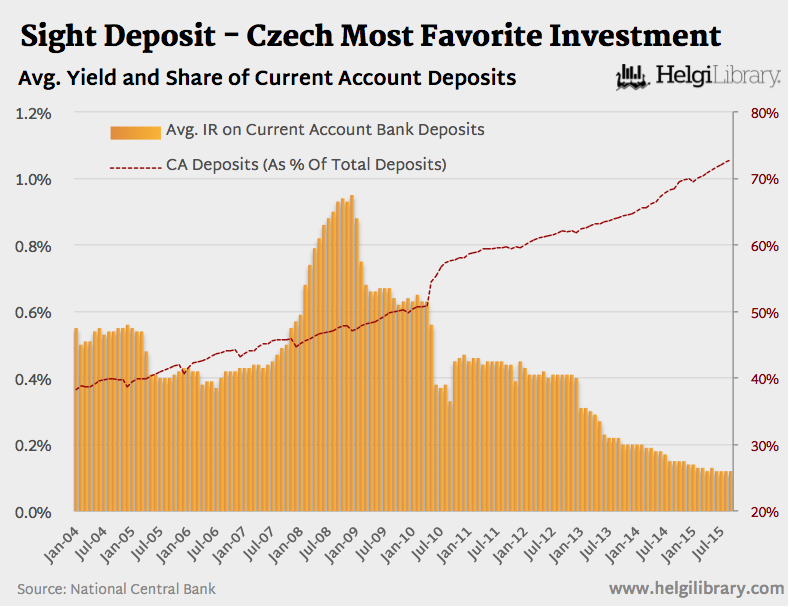

Deutsche Skatbank, in the eastern state of Thuringia, plans to apply a negative rate of interest to current account deposits with balances over EUR 500,000. The bank presumably hopes to nudge savers into other longer-term, less liquid or higher-return investments and make some money by selling these.

Deutsche Skatbank, in the eastern state of Thuringia, plans to apply a negative rate of interest to current account deposits with balances over EUR 500,000. The bank presumably hopes to nudge savers into other longer-term, less liquid or higher-return investments and make some money by selling these.

Helgi Library

Helgi Library