This report analyses the performance of the Bank for the 3Q2014. You will find all the necessary details regarding volume growth, market share, margin and asset quality development in the Bank.

The key highlights are:

UniCredit a's 3Q14 profit grows 2% yoy..

UniCredit CR and Slovakia reported a net profit of CZK 1,101 mil. in 3Q14. This is 2% up when compared to last year, though the comparison should be taken with a grain of salt since the 3Q13 operations do not include the bank's Slovak business (incorporated in 4Q14). Since operating profit was down 5% yoy, lower provisions are the only reason the bank saw its profit rise in the quarter.

The overall profitability of the bank remains weak. Since 2008, ROE stays in high single digit figures, which is not good enough for such a well-profitable market as the Czech Republic's.

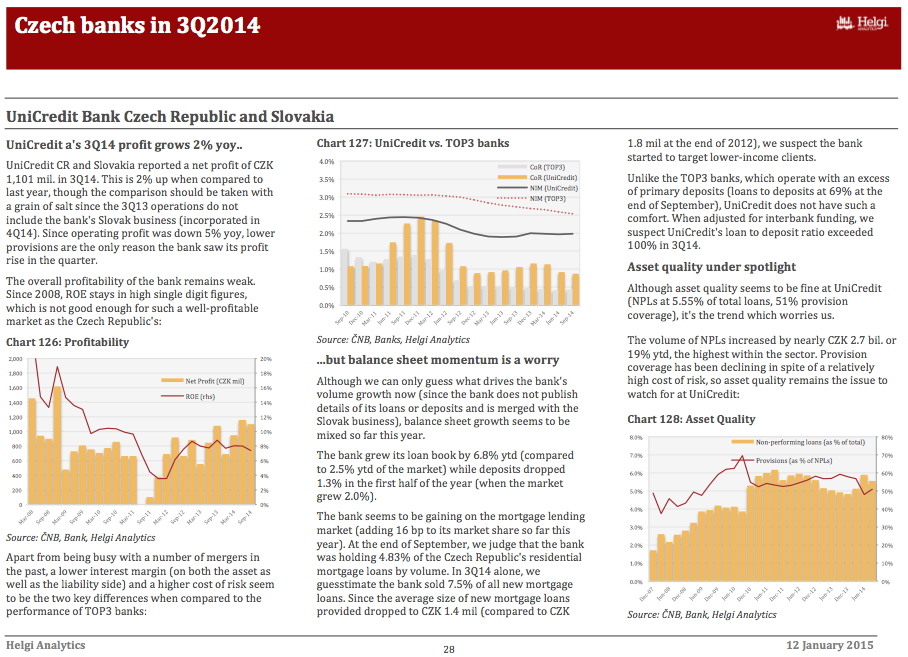

Apart from being busy with a number of mergers in the past, a lower interest margin (on both the asset as well as the liability side) and a higher cost of risk seem to be the two key differences when compared to the performance of TOP3 banks.

...but balance sheet momentum is a worry

Although we can only guess what drives the bank's volume growth now (since the bank does not publish details of its loans or deposits and is merged with the Slovak business), balance sheet growth seems to be mixed so far this year.

The bank grew its loan book by 6.8% ytd (compared to 2.5% ytd of the market) while deposits dropped 1.3% in the first half of the year (when the market grew 2.0%).

The bank seems to be gaining on the mortgage lending market (adding 16 bp to its market share so far this year). At the end of September, we judge that the bank was holding 4.83% of the Czech Republic's residential mortgage loans by volume. In 3Q14 alone, we guesstimate the bank sold 7.5% of all new mortgage loans. Since the average size of new mortgage loans provided dropped to CZK 1.4 mil (compared to CZK 1.8 mil at the end of 2012), we suspect the bank started to target lower-income clients.

Unlike the TOP3 banks, which operate with an excess of primary deposits (loans to deposits at 69% at the end of September), UniCredit does not have such a comfort. When adjusted for interbank funding, we suspect UniCredit's loan to deposit ratio exceeded 100% in 3Q14.

Asset quality under spotlight

Although asset quality seems to be fine at UniCredit (NPLs at 5.55% of total loans, 51% provision coverage), it's the trend which worries us.

The volume of NPLs increased by nearly CZK 2.7 bil. or 19% ytd, the highest within the sector. Provision coverage has been declining in spite of a relatively high cost of risk, so asset quality remains the issue to watch for at UniCredit.

You will find more details about the bank at www.helgilibrary.com/companies

Helgi Library

Helgi Library