This report analyses the performance of the Bank for the 3Q2014. You will find all the necessary details regarding volume growth, market share, margin and asset quality development in the Bank.

The key highlights are:

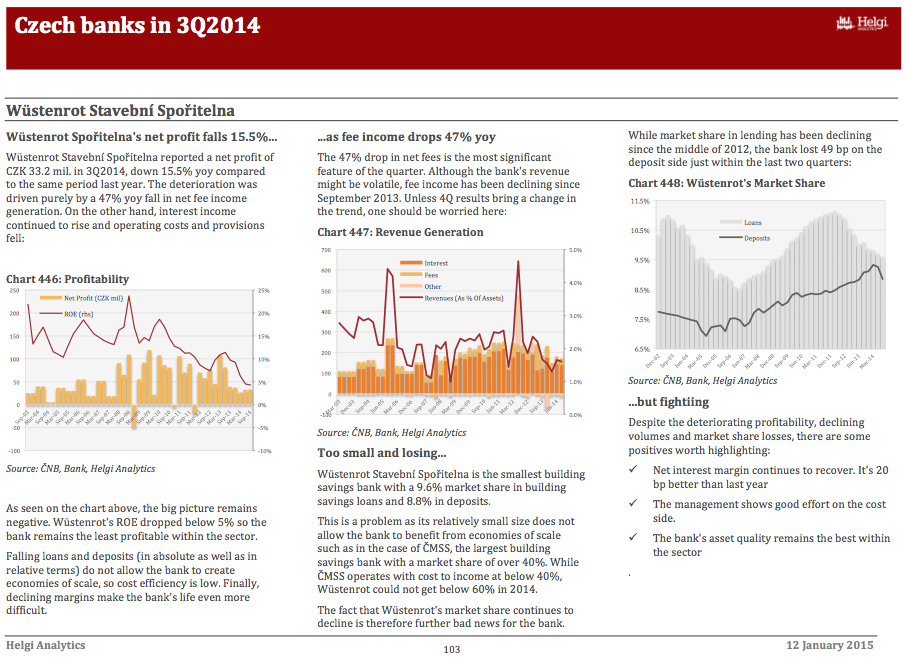

Wüstenrot Spořitelna's net profit falls 15.5%...

Wüstenrot Stavební Spořitelna reported a net profit of CZK 33.2 mil. in 3Q2014, down 15.5% yoy compared to the same period last year. The deterioration was driven purely by a 47% yoy fall in net fee income generation. On the other hand, interest income continued to rise and operating costs and provisions fell.

As seen on the chart above, the big picture remains negative. Wüstenrot's ROE dropped below 5% so the bank remains the least profitable within the sector.

Falling loans and deposits (in absolute as well as in relative terms) do not allow the bank to create economies of scale, so cost efficiency is low. Finally, declining margins make the bank's life even more difficult.

...as fee income drops 47% yoy

The 47% drop in net fees is the most significant feature of the quarter. Although the bank's revenue might be volatile, fee income has been declining since September 2013. Unless 4Q results bring a change in the trend, one should be worried here.

Too small and losing...

Wüstenrot Stavební Spořitelna is the smallest building savings bank with a 9.6% market share in building savings loans and 8.8% in deposits.

This is a problem as its relatively small size does not allow the bank to benefit from economies of scale such as in the case of ČMSS, the largest building savings bank with a market share of over 40%. While ČMSS operates with cost to income at below 40%, Wüstenrot could not get below 60% in 2014.

The fact that Wüstenrot's market share continues to decline is therefore further bad news for the bank.

While market share in lending has been declining since the middle of 2012, the bank lost 49 bp on the deposit side just within the last two quarters.

...but fightiing

Despite the deteriorating profitability, declining volumes and market share losses, there are some positives worth highlighting:

• Net interest margin continues to recover. It's 20 bp better than last year

• The management shows good effort on the cost side.

• The bank's asset quality remains the best within the sector

You will find more details about the bank at www.helgilibrary.com/companies

Helgi Library

Helgi Library