By Helgi Library - August 20, 2019

Promsvyazbank's non-performing loans reached 35.2% of total loans at the end of 2018, down from 61.7% compared to the previous ye...

By Helgi Library - August 20, 2019

Promsvyazbank's net interest margin amounted to 2.37% in 2018, down from 2.44% compared to the previous year. Historically...

By Helgi Library - August 20, 2019

Promsvyazbank employed 12,700 persons in 2018, up 33.7% when compared to the previous year. Historically, the bank's workforce h...

| Profit Statement | 2016 | 2017 | 2018 | |

| Net Interest Income | RUB bil | 27.6 | 24.9 | 24.8 |

| Net Fee Income | RUB bil | 17.7 | 22.0 | 16.5 |

| Other Income | RUB bil | 10.6 | -5.46 | -2.34 |

| Total Revenues | RUB bil | 55.9 | 41.4 | 39.0 |

| Staff Cost | RUB bil | 12.7 | 15.8 | 20.4 |

| Operating Profit | RUB bil | 34.8 | 16.4 | 9.52 |

| Provisions | RUB bil | 32.1 | 412 | 12.3 |

| Net Profit | RUB bil | 2.28 | -406 | 1.70 |

| Balance Sheet | 2016 | 2017 | 2018 | |

| Interbank Loans | RUB bil | 17.5 | 3.54 | 189 |

| Customer Loans | RUB bil | 783 | 469 | 551 |

| Total Assets | RUB bil | 1,224 | 813 | 1,281 |

| Shareholders' Equity | RUB bil | 91.5 | -285 | 149 |

| Interbank Borrowing | RUB bil | 76.7 | 443 | 47.6 |

| Customer Deposits | RUB bil | 883 | 575 | 1,012 |

| Issued Debt Securities | RUB bil | 122 | 50.6 | 24.1 |

| Ratios | 2016 | 2017 | 2018 | |

| ROE | % | 2.61 | -420 | -2.51 |

| ROA | % | 0.187 | -39.8 | 0.162 |

| Costs (As % Of Assets) | % | 1.73 | 2.45 | 2.81 |

| Costs (As % Of Income) | % | 37.7 | 60.4 | 75.6 |

| Capital Adequacy Ratio | % | 13.4 | ... | 13.5 |

| Net Interest Margin | % | 2.27 | 2.44 | 2.37 |

| Loans (As % Of Deposits) | % | 88.7 | 81.5 | 54.4 |

| NPLs (As % Of Loans) | % | 19.3 | 61.7 | 35.2 |

| Provisions (As % Of NPLs) | % | 41.4 | 67.6 | 86.5 |

| Growth Rates | 2016 | 2017 | 2018 | |

| Total Revenue Growth | % | 19.3 | -26.0 | -5.86 |

| Operating Cost Growth | % | 7.30 | 18.7 | 17.8 |

| Operating Profit Growth | % | 27.9 | -52.9 | -41.9 |

| Net Profit Growth | % | -114 | -17,856 | -100 |

| Customer Loan Growth | % | -2.07 | -40.1 | 17.5 |

| Total Asset Growth | % | 0.947 | -33.6 | 57.6 |

| Customer Deposit Growth | % | 11.5 | -34.9 | 76.0 |

| Shareholders' Equity Growth | % | 9.70 | -411 | -152 |

| Employees | 9,358 | 9,500 | 12,700 | |

Get all company financials in excel:

| summary | Unit | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| income statement | |||||||||||||||||||

| Net Interest Income | RUB bil | 25.8 | 29.6 | 32.8 | 27.3 | 27.6 | |||||||||||||

| Total Revenues | RUB bil | 34.3 | 40.8 | 51.0 | 46.9 | 55.9 | |||||||||||||

| Operating Profit | RUB bil | 14.3 | 19.6 | 29.8 | 27.2 | 34.8 | |||||||||||||

| Net Profit | RUB bil | 8.17 | 3.96 | 2.34 | -16.5 | 2.28 | |||||||||||||

| balance sheet | |||||||||||||||||||

| Interbank Loans | RUB bil | 11.8 | 20.7 | 25.0 | 37.8 | 17.5 | |||||||||||||

| Customer Loans | RUB bil | 462 | 545 | 753 | 800 | 783 | |||||||||||||

| Debt Securities | RUB bil | 59.7 | 62.8 | 97.2 | 151 | 209 | |||||||||||||

| Total Assets | RUB bil | 690 | 739 | 1,062 | 1,213 | 1,224 | |||||||||||||

| Shareholders' Equity | RUB bil | 62.7 | 66.2 | 69.0 | 83.4 | 91.5 | |||||||||||||

| Interbank Borrowing | RUB bil | 55.3 | 58.0 | 159 | 164 | 76.7 | |||||||||||||

| Customer Deposits | RUB bil | 445 | 488 | 660 | 792 | 883 | |||||||||||||

| Issued Debt Securities | RUB bil | 124 | 120 | 165 | 118 | 122 | |||||||||||||

| ratios | |||||||||||||||||||

| ROE | % | 14.0 | 6.14 | 3.47 | -21.6 | 2.61 | |||||||||||||

| ROA | % | 1.30 | 0.554 | 0.260 | -1.45 | 0.187 | |||||||||||||

| Costs (As % Of Assets) | % | 3.20 | 2.96 | 2.35 | 1.73 | 1.73 | |||||||||||||

| Costs (As % Of Income) | % | 58.4 | 51.9 | 41.5 | 41.9 | 37.7 | |||||||||||||

| Capital Adequacy Ratio | % | ... | ... | ... | 16.0 | 14.4 | 13.5 | 14.4 | 13.4 | ... | |||||||||

| Net Interest Margin | % | 4.12 | 4.15 | 3.64 | 2.40 | 2.27 | |||||||||||||

| Interest Income (As % Of Revenues) | % | 75.3 | 72.6 | 64.3 | 58.3 | 49.4 | |||||||||||||

| Fee Income (As % Of Revenues) | % | 22.0 | 22.4 | 26.1 | 28.4 | 31.7 | |||||||||||||

| Staff Cost (As % Of Total Cost) | % | 63.6 | 65.7 | 66.9 | 63.7 | 60.1 | |||||||||||||

| Equity (As % Of Assets) | % | 9.09 | 8.95 | 6.50 | 6.88 | 7.48 | |||||||||||||

| Loans (As % Of Deposits) | % | 104 | 112 | 114 | 101 | 88.7 | |||||||||||||

| Loans (As % Assets) | % | 66.9 | 73.8 | 70.9 | 65.9 | 64.0 | |||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 4.35 | 3.61 | 2.90 | 4.03 | 19.3 | ||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 110 | 125 | 165 | 200 | 41.4 | ||||||||||

| valuation | |||||||||||||||||||

| Book Value Per Share Growth | % | ... | 31.8 | 14.7 | 10.8 | -16.8 | 1.14 |

| income statement | Unit | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| income statement | |||||||||||||||||||

| Interest Income | RUB bil | 54.7 | 66.2 | 79.5 | 103 | 103 | |||||||||||||

| Interest Cost | RUB bil | 28.9 | 36.5 | 46.7 | 76.1 | 75.4 | |||||||||||||

| Net Interest Income | RUB bil | 25.8 | 29.6 | 32.8 | 27.3 | 27.6 | |||||||||||||

| Net Fee Income | RUB bil | 7.56 | 9.15 | 13.3 | 13.3 | 17.7 | |||||||||||||

| Other Income | RUB bil | 0.922 | 2.03 | 4.90 | 6.25 | 10.6 | |||||||||||||

| Total Revenues | RUB bil | 34.3 | 40.8 | 51.0 | 46.9 | 55.9 | |||||||||||||

| Staff Cost | RUB bil | 12.7 | 13.9 | 14.2 | 12.5 | 12.7 | |||||||||||||

| Depreciation | RUB bil | 1.16 | 1.04 | 1.06 | 1.34 | 1.68 | |||||||||||||

| Other Cost | RUB bil | 6.14 | 6.23 | 5.95 | 5.78 | 6.72 | |||||||||||||

| Operating Cost | RUB bil | 20.0 | 21.2 | 21.2 | 19.6 | 21.1 | |||||||||||||

| Operating Profit | RUB bil | 14.3 | 19.6 | 29.8 | 27.2 | 34.8 | |||||||||||||

| Provisions | RUB bil | 4.33 | 14.2 | 26.6 | 47.3 | 32.1 | |||||||||||||

| Extra and Other Cost | RUB bil | -0.070 | 0.553 | -0.001 | 0 | 0 | |||||||||||||

| Pre-Tax Profit | RUB bil | 10.0 | 4.90 | 3.24 | -20.1 | 2.77 | |||||||||||||

| Tax | RUB bil | 1.85 | 0.944 | 0.937 | -3.68 | 0.638 | |||||||||||||

| Minorities | RUB bil | -0.007 | -0.001 | -0.038 | 0.067 | 0.148 | |||||||||||||

| Net Profit | RUB bil | 8.17 | 3.96 | 2.34 | -16.5 | 2.28 | |||||||||||||

| growth rates | |||||||||||||||||||

| Net Interest Income Growth | % | ... | 31.8 | 14.7 | 10.8 | -16.8 | 1.14 | ||||||||||||

| Net Fee Income Growth | % | ... | 6.75 | 21.0 | 45.8 | -0.143 | 33.0 | ||||||||||||

| Total Revenue Growth | % | ... | 18.7 | 18.9 | 25.1 | -8.19 | 19.3 | ||||||||||||

| Operating Cost Growth | % | ... | 18.2 | 5.68 | 0.057 | -7.42 | 7.30 | ||||||||||||

| Operating Profit Growth | % | ... | 19.4 | 37.5 | 52.2 | -8.74 | 27.9 | ||||||||||||

| Pre-Tax Profit Growth | % | ... | 41.7 | -51.0 | -33.9 | -719 | -114 | ||||||||||||

| Net Profit Growth | % | ... | 55.3 | -51.5 | -40.8 | -803 | -114 | ||||||||||||

| market share | |||||||||||||||||||

| Market Share in Revenues | % | ... | ... | ... | 0.865 | 0.901 | 0.849 | 0.700 | 0.426 | ... | |||||||||

| Market Share in Net Profit | % | ... | ... | ... | ... | 1.03 | 0.545 | 0.482 | ... | 0.348 | ... | ... | |||||||

| Market Share in Employees | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.14 | 1.03 | ... | ... | ... |

| Market Share in Branches | % | ... | ... | ... | ... | ... | ... | 0.718 | 0.745 | 0.721 | 0.827 | 0.893 | ... |

| balance sheet | Unit | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| balance sheet | |||||||||||||||||||

| Cash | RUB bil | 129 | 77.3 | 138 | 149 | 127 | |||||||||||||

| Interbank Loans | RUB bil | 11.8 | 20.7 | 25.0 | 37.8 | 17.5 | |||||||||||||

| Customer Loans | RUB bil | 462 | 545 | 753 | 800 | 783 | |||||||||||||

| Retail Loans | RUB bil | 54.5 | 67.9 | 81.6 | 72.6 | 71.8 | |||||||||||||

| Mortgage Loans | RUB bil | ... | ... | ... | ... | ... | ... | 8.38 | 9.64 | 16.5 | 17.2 | 24.2 | |||||||

| Consumer Loans | RUB bil | ... | ... | ... | ... | ... | ... | 41.1 | 52.2 | 59.5 | 48.7 | 47.6 | |||||||

| Corporate Loans | RUB bil | 354 | 416 | 631 | 743 | 779 | |||||||||||||

| Debt Securities | RUB bil | 59.7 | 62.8 | 97.2 | 151 | 209 | |||||||||||||

| Fixed Assets | RUB bil | 25.2 | 23.7 | 13.8 | 14.3 | 13.4 | |||||||||||||

| Total Assets | RUB bil | 690 | 739 | 1,062 | 1,213 | 1,224 | |||||||||||||

| Shareholders' Equity | RUB bil | 62.7 | 66.2 | 69.0 | 83.4 | 91.5 | |||||||||||||

| Of Which Minority Interest | RUB bil | -0.051 | -0.021 | -0.059 | 1.06 | -0.099 | |||||||||||||

| Liabilities | RUB bil | 627 | 673 | 993 | 1,129 | 1,133 | |||||||||||||

| Interbank Borrowing | RUB bil | 55.3 | 58.0 | 159 | 164 | 76.7 | |||||||||||||

| Customer Deposits | RUB bil | 445 | 488 | 660 | 792 | 883 | |||||||||||||

| Retail Deposits | RUB bil | 171 | 201 | 240 | 289 | 400 | |||||||||||||

| Corporate Deposits | RUB bil | 275 | 288 | 421 | 502 | 483 | |||||||||||||

| Sight Deposits | RUB bil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 174 | 224 | 225 | ||

| Term Deposits | RUB bil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 487 | 567 | 659 | ||

| Issued Debt Securities | RUB bil | 124 | 120 | 165 | 118 | 122 | |||||||||||||

| Other Liabilities | RUB bil | 3.31 | 6.46 | 9.06 | 56.0 | 50.4 | |||||||||||||

| asset quality | |||||||||||||||||||

| Non-Performing Loans | RUB bil | ... | ... | ... | 21.1 | 20.6 | 23.0 | 35.1 | 164 | ||||||||||

| Gross Loans | RUB bil | ... | ... | ... | 485 | 571 | 791 | 870 | 851 | ||||||||||

| Total Provisions | RUB bil | ... | ... | ... | 23.1 | 25.8 | 37.8 | 70.3 | 68.1 | ||||||||||

| growth rates | |||||||||||||||||||

| Customer Loan Growth | % | ... | 16.6 | 18.1 | 38.0 | 6.22 | -2.07 | ||||||||||||

| Retail Loan Growth | % | ... | 69.0 | 24.6 | 20.2 | -11.0 | -1.15 | ||||||||||||

| Mortgage Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | 72.0 | 15.0 | 70.8 | 4.71 | 40.6 | ||||||

| Consumer Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | 63.5 | 27.0 | 14.0 | -18.1 | -2.38 | ||||||

| Corporate Loan Growth | % | ... | 9.18 | 17.4 | 51.5 | 17.9 | 4.84 | ||||||||||||

| Total Asset Growth | % | ... | 22.7 | 7.08 | 43.7 | 14.2 | 0.947 | ||||||||||||

| Shareholders' Equity Growth | % | ... | 16.0 | 5.44 | 4.28 | 20.9 | 9.70 | ||||||||||||

| Customer Deposit Growth | % | ... | 31.5 | 9.61 | 35.3 | 19.9 | 11.5 | ||||||||||||

| Retail Deposit Growth | % | ... | 37.4 | 17.6 | 19.6 | 20.6 | 38.5 | ||||||||||||

| Corporate Deposit Growth | % | ... | 28.1 | 4.66 | 46.3 | 19.5 | -3.95 | ||||||||||||

| market share | |||||||||||||||||||

| Market Share in Customer Loans | % | 1.55 | 1.53 | 1.66 | 1.63 | 1.68 | ... | ||||||||||||

| Market Share in Corporate Loans | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.91 | 1.97 | 2.30 | 2.45 | 2.84 | ... | |||

| Market Share in Retail Loans | % | ... | ... | ... | ... | ... | ... | ... | 0.717 | 0.714 | 0.763 | 0.727 | 0.753 | ... | |||||

| Market Share in Consumer Loans | % | ... | ... | ... | 0.705 | 0.682 | 0.720 | 0.680 | 0.664 | ... | |||||||||

| Market Share in Mortgage Loans | % | ... | ... | ... | ... | ... | ... | ... | 0.420 | 0.364 | 0.467 | 0.433 | 0.540 | ... | |||||

| Market Share in Total Assets | % | ... | ... | ... | 1.48 | 1.36 | 1.45 | 1.58 | 1.66 | ... | |||||||||

| Market Share in Customer Deposits | % | ... | ... | ... | 2.17 | 2.05 | 2.10 | 2.11 | 2.51 | ... | |||||||||

| Market Share in Retail Deposits | % | ... | ... | ... | 1.20 | 1.18 | 1.29 | 1.25 | 1.65 | ... | |||||||||

| Market Share in Corporate Deposits | % | ... | ... | ... | 2.86 | 2.65 | 2.47 | 2.64 | 2.95 | ... |

| ratios | Unit | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| ratios | |||||||||||||||||||

| ROE | % | 14.0 | 6.14 | 3.47 | -21.6 | 2.61 | |||||||||||||

| ROA | % | 1.30 | 0.554 | 0.260 | -1.45 | 0.187 | |||||||||||||

| Costs (As % Of Assets) | % | 3.20 | 2.96 | 2.35 | 1.73 | 1.73 | |||||||||||||

| Costs (As % Of Income) | % | 58.4 | 51.9 | 41.5 | 41.9 | 37.7 | |||||||||||||

| Capital Adequacy Ratio | % | ... | ... | ... | 16.0 | 14.4 | 13.5 | 14.4 | 13.4 | ... | |||||||||

| Tier 1 Ratio | % | ... | ... | ... | 10.3 | 9.40 | 8.01 | 8.23 | 8.24 | ... | |||||||||

| Net Interest Margin | % | 4.12 | 4.15 | 3.64 | 2.40 | 2.27 | |||||||||||||

| Interest Spread | % | ... | 3.65 | 3.64 | 3.22 | 1.92 | 1.79 | ||||||||||||

| Asset Yield | % | 8.74 | 9.26 | 8.83 | 9.09 | 8.45 | |||||||||||||

| Cost Of Liabilities | % | ... | 5.09 | 5.62 | 5.60 | 7.17 | 6.67 | ||||||||||||

| Interest Income (As % Of Revenues) | % | 75.3 | 72.6 | 64.3 | 58.3 | 49.4 | |||||||||||||

| Fee Income (As % Of Revenues) | % | 22.0 | 22.4 | 26.1 | 28.4 | 31.7 | |||||||||||||

| Other Income (As % Of Revenues) | % | 2.69 | 4.98 | 9.61 | 13.3 | 18.9 | |||||||||||||

| Cost Per Employee | USD per month | ... | ... | ... | ... | ... | ... | 3,326 | 2,336 | 1,804 | 1,688 | ||||||||

| Cost Per Employee (Local Currency) | RUB per month | ... | ... | ... | ... | ... | ... | 105,966 | 109,328 | 120,496 | 112,693 | ||||||||

| Staff Cost (As % Of Total Cost) | % | 63.6 | 65.7 | 66.9 | 63.7 | 60.1 | |||||||||||||

| Equity (As % Of Assets) | % | 9.09 | 8.95 | 6.50 | 6.88 | 7.48 | |||||||||||||

| Loans (As % Of Deposits) | % | 104 | 112 | 114 | 101 | 88.7 | |||||||||||||

| Loans (As % Assets) | % | 66.9 | 73.8 | 70.9 | 65.9 | 64.0 | |||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 4.35 | 3.61 | 2.90 | 4.03 | 19.3 | ||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 110 | 125 | 165 | 200 | 41.4 | ||||||||||

| Provisions (As % Of Loans) | % | ... | ... | ... | 5.01 | 4.74 | 5.03 | 8.79 | 8.70 | ||||||||||

| Cost of Provisions (As % Of Loans) | % | 1.01 | 2.81 | 4.10 | 6.10 | 4.05 |

| other data | Unit | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

| other data | |||||||||||||||||||

| Branches | ... | ... | ... | ... | ... | ... | 306 | 322 | 300 | 306 | 303 | ||||||||

| Employees | ... | ... | ... | ... | ... | ... | 10,939 | 10,810 | 8,649 | 9,358 | |||||||||

| ATMs | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |||

| Clients | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |

| Sight (As % Of Customer Deposits) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 26.3 | 28.3 | 25.4 |

Get all company financials in excel:

By Helgi Library - August 20, 2019

Promsvyazbank made a net profit of RUB 1.70 bil under revenues of RUB 39.0 bil in 2018, up 100% and -5.86% respectively compared to the previous year. Historically, the bank’s net profit reached an all time high of RUB 8.17 bil in 2012 and an all time low of RUB -406...

By Helgi Library - August 20, 2019

Promsvyazbank's loans reached RUB 792 bil in the 2018, up from RUB 780 bil compared to the previous year. Historically, the bank’s loans reached an all time high of RUB 870 bil in 2015 and an all time low of RUB 214 bil in 2007. In the last decade, the ...

By Helgi Library - August 20, 2019

Promsvyazbank's capital adequacy ratio reached 13.5% at the end of 2018, up from compared to the previous year. Historically, the bank’s capital ratio hit an all time high of 16.8% in 2004 and an all time low of 13.1% in 2008. The Tier 1 ratio amounted to ...

By Helgi Library - August 20, 2019

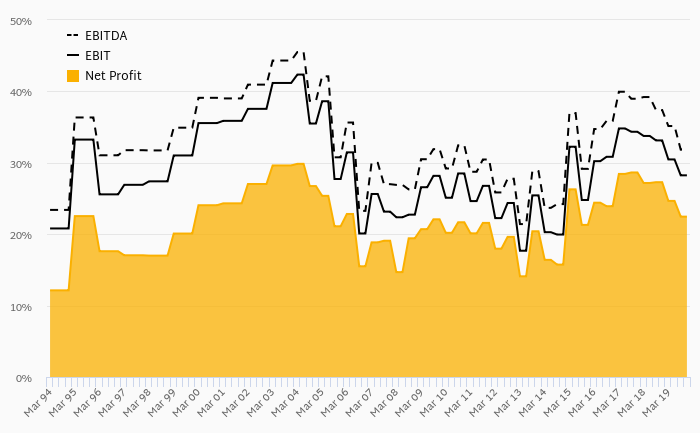

Promsvyazbank's cost to income ratio reached 75.6% in 2018, up from 60.4% compared to the previous year. Historically, the bank’s costs reached an all time high of 75.6% of income in 2018 and an all time low of 37.7% in 2016. When compared to total assets,...

By Helgi Library - August 20, 2019

Promsvyazbank generated total banking revenues of RUB 39.0 bil in 2018, down 5.86% compared to the previous year. Historically, the bank’s revenues containing of interest, fee and other non-interest income reached an all time high of RUB 55.9 bil in 2016 and an...

By Helgi Library - August 20, 2019

Promsvyazbank's retail loans reached RUB 101 bil at the end of 2018, up 37.0% compared to the previous year. In the last decade, the average annual loan growth amounted to 7.17%. Overall, retail loans accounted for 18.3% of the bank's loan book at the end o...

By Helgi Library - August 20, 2019

Promsvyazbank's customer loan growth reached 17.5% in 2018, up from -40.1% compared to the previous year. Historically, the bank’s loans growth reached an all time high of 87.5% in 2005 and an all time low of -40.1% in 2017. In the last decade, the averag...

By Helgi Library - November 29, 2018

Promsvyazbank's mortgage loans reached RUB 29.6 bil in 2017, up 22.0% compared to the previous year. Russian banking sector provided mortgage loans of RUB 5,187 bil in 2017, up 15.5% when compared to the last year. Promsvyazbank accounted for 0.570% of al...

By Helgi Library - September 8, 2018

Promsvyazbank's customer deposits reached RUB 575 bil in 2017, down 34.9% compared to the previous year. Russian banking sector accepted customer deposits of RUB 37,471 bil in 2017, up 6.51% when compared to the last year. Promsvyazbank accounted for 1.53...

By Helgi Library - September 27, 2018

Promsvyazbank's retail deposits reached RUB 357 bil in 2017, down 10.8% compared to the previous year. Russian banking sector accepted retail deposits of RUB 25,987 bil in 2017, up 7.38% when compared to the last year. Promsvyazbank accounted for 1.38% of...

Promsvyazbank (PSB) is Russia-based commercial bank. The Bank was ranked as the 10th largest in Russia in 2012. The PSB provides financial services such as commercial banking, retail banking, private baking, SME banking or investment banking. At the end of 2013, the Bank had serviced 1.2 million retail clients and over 93,000 corporate clients to whom it offered its services throughout 302 branches in more than 90 communities across Russia. The Bank was founded in 1995 by the Ananyev brothers, the owners of Tekhnoserv, the largest systems integrator in the CIS. The Bank is headquartered in Moscow, Russia

Promsvyazbank has been growing its revenues and asset by 3.27% and 10.7% a year on average in the last 10 years. Its loans and deposits have grown by 6.25% and 16.0% a year during that time and loans to deposits ratio reached 54.4% at the end of 2018. The company achieved an average return on equity of -40.3% in the last decade with net profit growing 0.829% a year on average. In terms of operating efficiency, its cost to income ratio reached 75.6% in 2018, compared to 51.7% average in the last decade.

Equity represented 11.7% of total assets or 27.1% of loans at the end of 2018. Promsvyazbank's non-performing loans were 35.2% of total loans while provisions covered some 86.5% of NPLs at the end of 2018.

Helgi Library

Helgi Library