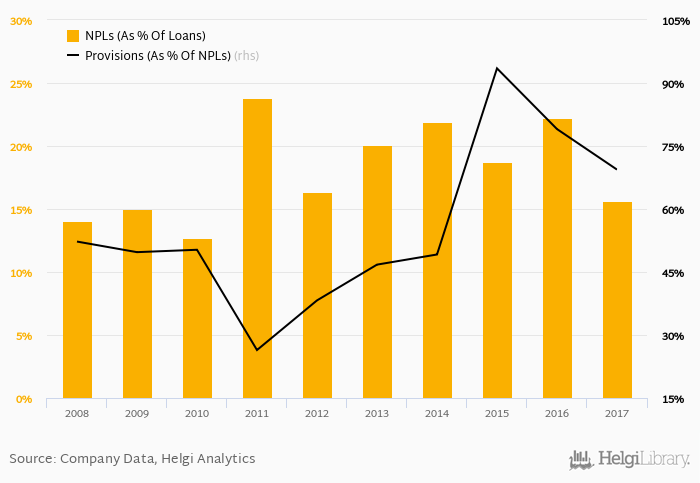

Komercijalna Banka Beograd's non-performing loans reached 15.7% of total loans at the end of 2017, down from 22.2% compared to the previous year. Historically, the NPL ratio hit an all time high of 23.8% in 2011 and an all time low of 12.7% in 2010.

Provision coverage amounted to 69.4% at the end of 2017, down from 79.0% compared to a year earlier.

The bank created loan loss provisions worth of 0% of average loans in 2017. That's compared to 3.57% of loans the bank put aside to its cost on average in the last five years.

Comparing Komercijalna Banka Beograd with its closest peers, Societe Generale Serbia operated at the end of 2017 with NPL ratio of 10.2% and provision coverage of 85.6%, Bank Intesa Serbia with 9.25% and 51.5% respectively and Raiffeisenbank Serbia had 4.74% of bad loans covered with 95.5% by provisions at the end of 2017.

You can see all the bank’s data at Komercijalna Banka Beograd Profile, or you can download a report on the bank in the report section.

Helgi Library

Helgi Library