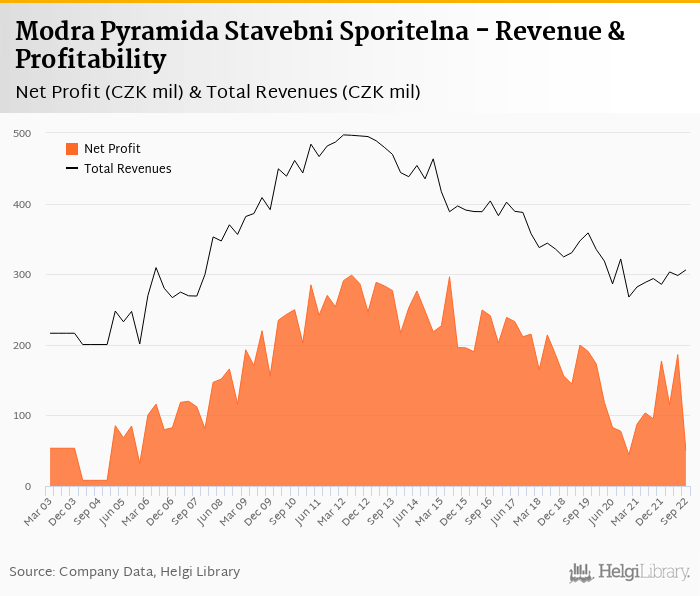

Modra Pyramida decreased its net profit 48% to CZK 49.5 mil in 3Q22 and generated ROE of 3.0%.

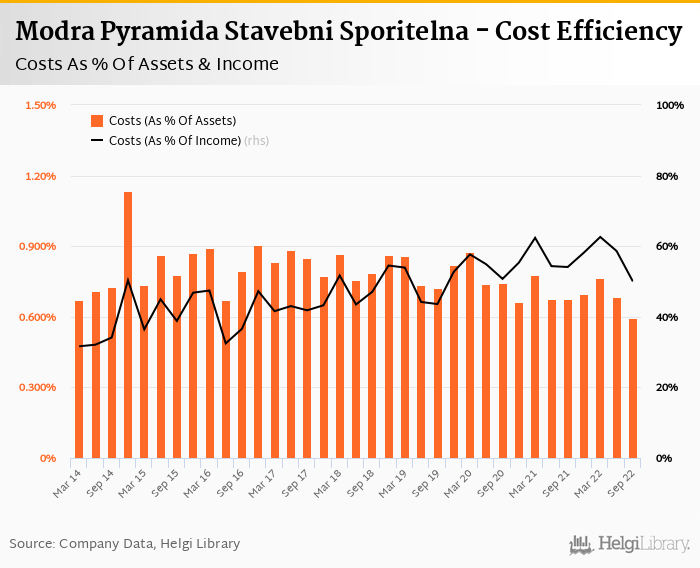

Revenues increased 4.18% yoy and cost fell 3.67%, so cost to income decreased to 50.0%

Cost of risk amounted 0.46% and loan to deposit ratio increased to 150%

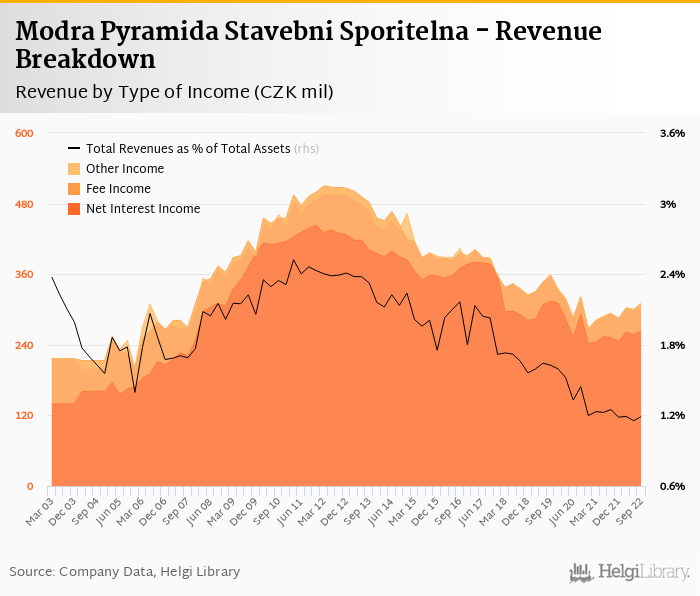

Revenues increased 4.2% yoy to CZK 306 mil in the third quarter of 2022. Net interest income rose 4.3% yoy in spite of net interest margin decreasing 0.051 pp to 1.02% of total assets. Fee income grew 14.5% yoy and added a further 15.3% to total revenue. When compared to three years ago, revenues were down 14.6%:

Average asset yield was 4.03% in the third quarter of 2022 (up from 2.57% a year ago) while cost of funding amounted to 3.21% in 3Q2022 (up from 1.60%).

Costs decreased by 3.67% yoy and the bank operated with cost to income of 50.0% in the last quarter. Staff cost rose 4.68% as the bank employed 356 persons (up 9.54% yoy) and the Bank paid CZK 82,169 per person per month in staff cost:

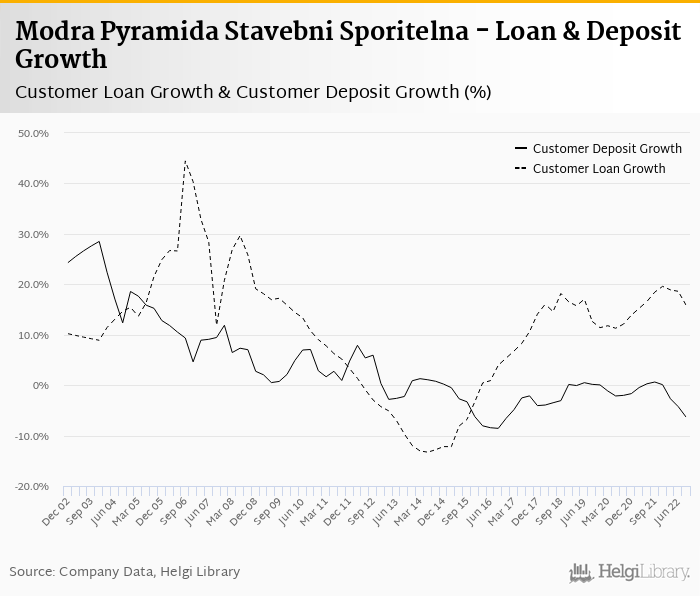

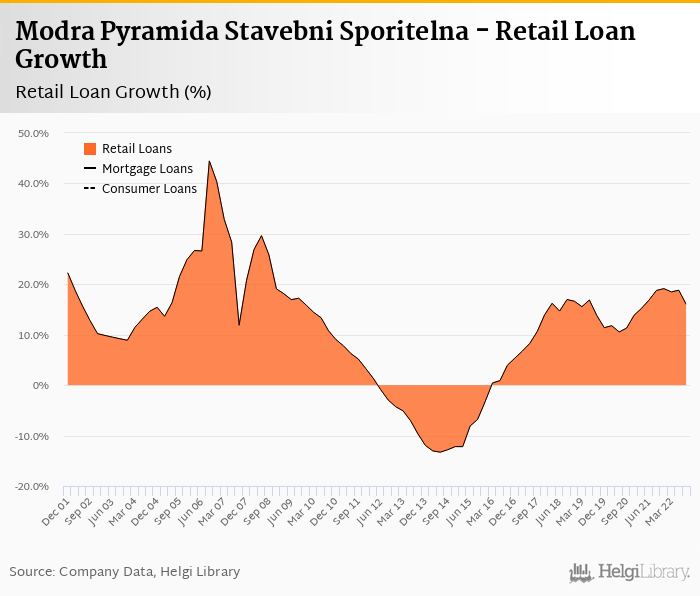

Customer loans grew relatively strong 2.59% qoq and 15.9% yoy in the third quarter of 2022 while customer deposit fell 2.36% qoq and 6.33% yoy. That’s compared to average of 15.3% and -1.65% average annual growth seen in the last three years.

At the end of third quarter of 2022, Modra Pyramida Stavebni Sporitelna's loans accounted for 150% of total deposits and 82.4% of total assets.

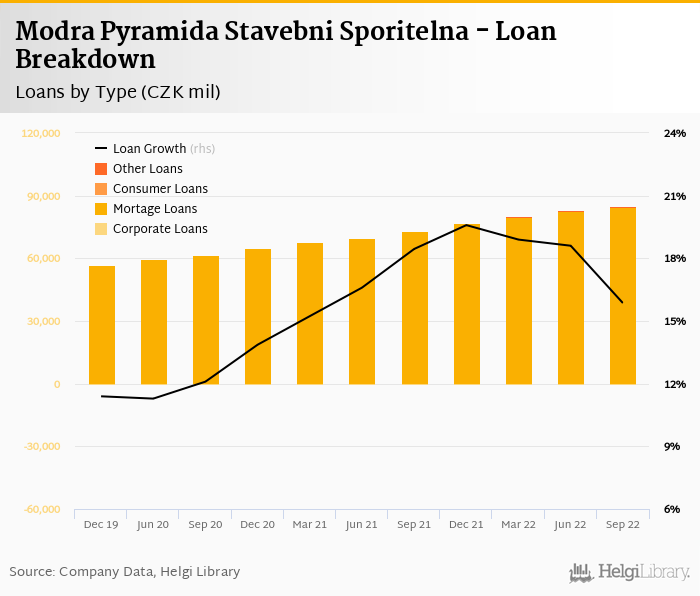

Retail loans grew 2.62% qoq and were 16.0% up yoy. They accounted for 99.7% of the loan book at the end of the third quarter of 2022 while corporate loans decreased 5.62% qoq and -18.5% yoy, respectively. Mortgages represented 99.7% of the Modra Pyramida Stavebni Sporitelna's loan book, consumer loans added a further 0% and corporate loans formed 0.293% of total loans:

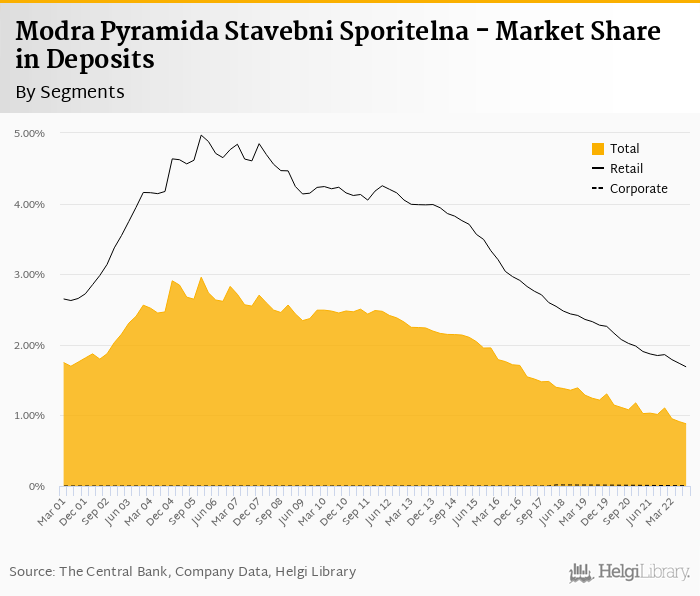

We estimate that Modra Pyramida Stavebni Sporitelna has gained 0.149 pp market share in the last twelve months in terms of loans (holding 2.09% of the market at the end of 3Q2022). On the funding side, the bank seems to have lost 0.133 pp and held 0.880% of the deposit market:

Cost of risk reached 0.462% of average loans as the Bank set aside CZK 96.6 mil in provisons. Provisions have "eaten" some 63.2% of operating profit in the third quarter of 2022, which is a high number. Full-year numbers might show more details if loan portfolio deterioration or debt securities revaluation are to blame.

We estimate that bank's NPL ratio of amounted to around 1.5% and some 40% of that was covered by provisions at the end of September:

We estimate that Modra Pyramida Stavebni Sporitelna's capital adequacy ratio reached approximately 20.0% in the third quarter of 2022 while bank equity accounted for 7.73% of loans:

Modra Pyramida Stavebni Sporitelna's net profit fell 48% yoy to CZK 49.5 mil in the third quarter of 2022, though operating profit grew solid 13.4% yoy. This means an annualized return on equity of 3.03%, or 12.9% when equity "adjusted" to 15% of risk-weighted assets:

Solid operating performance vs. significant increase in cost of risk, something to look at in the Bank's full-year results. Given the relatively high loan to deposit ratio and increased cost of funding, development in net interest margin will be interesting to watch in the near future.

Helgi Library

Helgi Library