By Helgi Library - November 23, 2023

Hypotecni Banka's customer deposits reached CZK 5,233 mil in 2023-06-30, up 1.00% compared to the previous year. Czech banking ...

By Helgi Library - November 23, 2023

Hypotecni Banka employed 69.5 persons in 2023-09-30, down 0% when compared to the previous year. Historically, the bank's workfo...

By Helgi Library - November 23, 2023

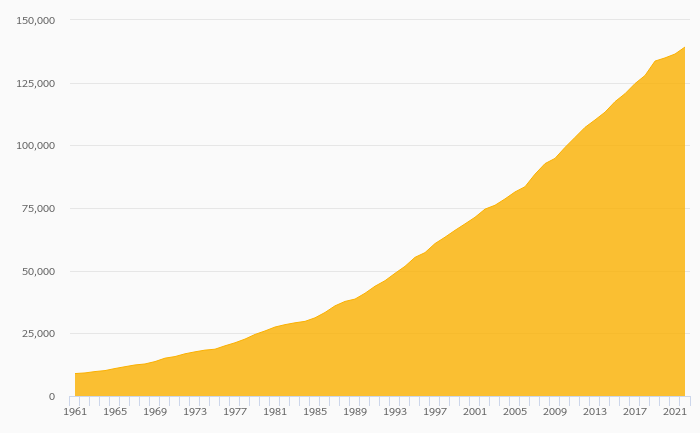

Hypotecni Banka's mortgage loans reached CZK 389,546 mil in 3Q2023, up 0.988% compared to the previous year. Czech banking sect...

| Profit Statement | 2020 | 2021 | 2022 | |

| Net Interest Income | CZK mil | 2,922 | 2,226 | 3,873 |

| Net Fee Income | CZK mil | 189 | 84.0 | 165 |

| Other Income | CZK mil | 160 | -210 | -187 |

| Total Revenues | CZK mil | 3,271 | 2,100 | 3,851 |

| Staff Cost | CZK mil | 465 | 188 | 113 |

| Operating Profit | CZK mil | 2,295 | 1,268 | 3,079 |

| Provisions | CZK mil | 358 | -549 | 12.0 |

| Net Profit | CZK mil | 1,566 | 1,478 | 2,483 |

| Balance Sheet | 2020 | 2021 | 2022 | |

| Interbank Loans | CZK mil | 6,623 | 6,625 | 8,094 |

| Customer Loans | CZK mil | 333,835 | 361,321 | 380,894 |

| Investments | CZK mil | 0 | 0 | 0 |

| Total Assets | CZK mil | 346,505 | 368,462 | 389,591 |

| Shareholders' Equity | CZK mil | 47,077 | 53,585 | 57,078 |

| Interbank Borrowing | CZK mil | 141 | 112 | 182 |

| Customer Deposits | CZK mil | 2.00 | 2.00 | 2.00 |

| Issued Debt Securities | CZK mil | 295,325 | 311,157 | 329,004 |

| Ratios | 2020 | 2021 | 2022 | |

| ROE | % | 3.42 | 2.94 | 4.49 |

| ROA | % | 0.467 | 0.413 | 0.655 |

| Costs (As % Of Assets) | % | 0.291 | 0.233 | 0.204 |

| Costs (As % Of Income) | % | 29.8 | 39.6 | 20.0 |

| Capital Adequacy Ratio | % | 45.9 | 45.2 | 49.9 |

| Net Interest Margin | % | 0.872 | 0.623 | 1.02 |

| Loans (As % Of Deposits) | % | 113 | 116 | 116 |

| NPLs (As % Of Loans) | % | 0.342 | 0.723 | 0.584 |

| Provisions (As % Of NPLs) | % | 117 | 30.1 | 34.4 |

| Growth Rates | 2020 | 2021 | 2022 | |

| Total Revenue Growth | % | -13.0 | -35.8 | 83.4 |

| Operating Cost Growth | % | -1.41 | -14.8 | -7.21 |

| Operating Profit Growth | % | -17.1 | -44.7 | 143 |

| Net Profit Growth | % | -36.0 | -5.62 | 68.0 |

| Customer Loan Growth | % | 5.79 | 8.23 | 5.42 |

| Total Asset Growth | % | 6.93 | 6.34 | 5.73 |

| Customer Deposit Growth | % | -93.5 | 0 | 0 |

| Shareholders' Equity Growth | % | 5.55 | 13.8 | 6.52 |

| Employees | 419 | 144 | 72.0 | |

Get all company financials in excel:

| summary | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| income statement | |||||||||||||||||||||||||||

| Net Interest Income | CZK mil | 4,497 | 3,939 | 3,507 | 3,448 | 2,922 | |||||||||||||||||||||

| Total Revenues | CZK mil | 5,061 | 4,439 | 3,845 | 3,760 | 3,271 | |||||||||||||||||||||

| Operating Profit | CZK mil | 3,992 | 3,458 | 2,853 | 2,770 | 2,295 | |||||||||||||||||||||

| Net Profit | CZK mil | 3,206 | 2,828 | 2,354 | 2,446 | 1,566 | |||||||||||||||||||||

| balance sheet | |||||||||||||||||||||||||||

| Interbank Loans | CZK mil | 6,622 | 6,621 | 6,622 | 6,623 | 6,623 | |||||||||||||||||||||

| Customer Loans | CZK mil | 254,078 | 280,409 | 299,439 | 315,556 | 333,835 | |||||||||||||||||||||

| Investments | CZK mil | 68.0 | 1,829 | 1,883 | 0 | 0 | |||||||||||||||||||||

| Total Assets | CZK mil | 262,513 | 288,314 | 308,765 | 324,053 | 346,505 | |||||||||||||||||||||

| Shareholders' Equity | CZK mil | 34,172 | 39,391 | 42,203 | 44,600 | 47,077 | |||||||||||||||||||||

| Interbank Borrowing | CZK mil | 2.00 | 2.00 | 2.00 | 9.00 | 141 | |||||||||||||||||||||

| Customer Deposits | CZK mil | 402 | 398 | 57.0 | 31.0 | 2.00 | |||||||||||||||||||||

| Issued Debt Securities | CZK mil | 226,579 | 247,011 | 264,165 | 277,396 | 295,325 | |||||||||||||||||||||

| ratios | |||||||||||||||||||||||||||

| ROE | % | ... | 9.45 | 7.69 | 5.77 | 5.64 | 3.42 | ||||||||||||||||||||

| ROA | % | ... | 1.29 | 1.03 | 0.789 | 0.773 | 0.467 | ||||||||||||||||||||

| Costs (As % Of Assets) | % | ... | 0.429 | 0.356 | 0.332 | 0.313 | 0.291 | ||||||||||||||||||||

| Costs (As % Of Income) | % | 21.1 | 22.1 | 25.8 | 26.3 | 29.8 | |||||||||||||||||||||

| Capital Adequacy Ratio | % | ... | 33.5 | 37.3 | 36.5 | 42.6 | 45.9 | ||||||||||||||||||||

| Net Interest Margin | % | ... | 1.80 | 1.43 | 1.17 | 1.09 | 0.872 | ||||||||||||||||||||

| Interest Income (As % Of Revenues) | % | 88.9 | 88.7 | 91.2 | 91.7 | 89.3 | |||||||||||||||||||||

| Fee Income (As % Of Revenues) | % | 10.3 | 12.6 | 11.5 | 6.62 | 5.78 | |||||||||||||||||||||

| Staff Cost (As % Of Total Cost) | % | 50.5 | 55.5 | 54.9 | 54.2 | 47.6 | |||||||||||||||||||||

| Equity (As % Of Assets) | % | 13.0 | 13.7 | 13.7 | 13.8 | 13.6 | |||||||||||||||||||||

| Loans (As % Of Deposits) | % | 112 | 114 | 113 | 114 | 113 | |||||||||||||||||||||

| Loans (As % Assets) | % | 96.8 | 97.3 | 97.0 | 97.4 | 96.3 | |||||||||||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 2.32 | 1.66 | 1.27 | 0.420 | 0.342 | ||||||||||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 43.1 | 45.1 | 43.0 | 91.8 | 117 | ||||||||||||||||||

| valuation | |||||||||||||||||||||||||||

| Book Value Per Share Growth | % | ... | 1.58 | -12.4 | -11.0 | -1.68 | -15.3 |

| income statement | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| income statement | |||||||||||||||||||||||||||

| Interest Income | CZK mil | 7,140 | 6,811 | 7,201 | 8,142 | 7,355 | |||||||||||||||||||||

| Interest Cost | CZK mil | 2,643 | 2,872 | 3,694 | 4,694 | 4,433 | |||||||||||||||||||||

| Net Interest Income | CZK mil | 4,497 | 3,939 | 3,507 | 3,448 | 2,922 | |||||||||||||||||||||

| Net Fee Income | CZK mil | 523 | 559 | 443 | 249 | 189 | |||||||||||||||||||||

| Fee Income | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 302 | 269 | ||

| Fee Expense | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 53.0 | 80.0 | ||

| Other Income | CZK mil | 41.0 | -59.0 | -105 | 63.0 | 160 | |||||||||||||||||||||

| Total Revenues | CZK mil | 5,061 | 4,439 | 3,845 | 3,760 | 3,271 | |||||||||||||||||||||

| Staff Cost | CZK mil | 540 | 544 | 545 | 536 | 465 | |||||||||||||||||||||

| Depreciation | CZK mil | 85.0 | 64.0 | 77.0 | 131 | 132 | |||||||||||||||||||||

| Other Cost | CZK mil | 444 | 373 | 370 | 323 | 379 | |||||||||||||||||||||

| Operating Cost | CZK mil | 1,069 | 981 | 992 | 990 | 976 | |||||||||||||||||||||

| Operating Profit | CZK mil | 3,992 | 3,458 | 2,853 | 2,770 | 2,295 | |||||||||||||||||||||

| Provisions | CZK mil | 47.0 | -21.0 | -140 | -252 | 358 | |||||||||||||||||||||

| Extra and Other Cost | CZK mil | 0 | 0 | 0 | 0.201 | 0 | |||||||||||||||||||||

| Pre-Tax Profit | CZK mil | 3,945 | 3,479 | 2,993 | 3,022 | 1,937 | |||||||||||||||||||||

| Tax | CZK mil | 739 | 651 | 639 | 576 | 371 | |||||||||||||||||||||

| Minorities | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

| Net Profit | CZK mil | 3,206 | 2,828 | 2,354 | 2,446 | 1,566 | |||||||||||||||||||||

| Net Profit Avail. to Common | CZK mil | 3,206 | 2,828 | 2,354 | 2,446 | 1,566 | |||||||||||||||||||||

| Dividends | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1,800 | 2,828 | 3,554 | 2,446 | 1,568 | ... | ||||||||||

| growth rates | |||||||||||||||||||||||||||

| Net Interest Income Growth | % | ... | 1.58 | -12.4 | -11.0 | -1.68 | -15.3 | ||||||||||||||||||||

| Net Fee Income Growth | % | ... | 3.77 | 6.88 | -20.8 | -43.8 | -24.1 | ||||||||||||||||||||

| Total Revenue Growth | % | ... | 1.52 | -12.3 | -13.4 | -2.21 | -13.0 | ||||||||||||||||||||

| Operating Cost Growth | % | ... | 22.3 | -8.23 | 1.12 | -0.202 | -1.41 | ||||||||||||||||||||

| Operating Profit Growth | % | ... | -2.89 | -13.4 | -17.5 | -2.91 | -17.1 | ||||||||||||||||||||

| Pre-Tax Profit Growth | % | ... | 6.85 | -11.8 | -14.0 | 0.969 | -35.9 | ||||||||||||||||||||

| Net Profit Growth | % | ... | 7.22 | -11.8 | -16.8 | 3.91 | -36.0 | ||||||||||||||||||||

| market share | |||||||||||||||||||||||||||

| Market Share in Revenues | % | 2.81 | 2.48 | 2.02 | 1.86 | 1.81 | |||||||||||||||||||||

| Market Share in Net Profit | % | 4.34 | 3.75 | 2.89 | 2.68 | 3.30 | |||||||||||||||||||||

| Market Share in Employees | % | ... | 1.33 | 1.31 | 1.26 | 1.19 | 1.03 | ||||||||||||||||||||

| Market Share in Branches | % | ... | 1.42 | 1.54 | 1.53 | 1.53 | 1.73 |

| balance sheet | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| balance sheet | |||||||||||||||||||||||||||

| Cash & Cash Equivalents | CZK mil | 1,150 | 725 | 1,619 | 632 | 1,864 | |||||||||||||||||||||

| Interbank Loans | CZK mil | 6,622 | 6,621 | 6,622 | 6,623 | 6,623 | |||||||||||||||||||||

| Customer Loans | CZK mil | 254,078 | 280,409 | 299,439 | 315,556 | 333,835 | |||||||||||||||||||||

| Retail Loans | CZK mil | 254,078 | 280,409 | 299,439 | 315,556 | 333,835 | |||||||||||||||||||||

| Mortgage Loans | CZK mil | 254,078 | 280,409 | 299,439 | 315,556 | 333,835 | |||||||||||||||||||||

| Consumer Loans | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

| Investments | CZK mil | 68.0 | 1,829 | 1,883 | 0 | 0 | |||||||||||||||||||||

| Property and Equipment | CZK mil | 296 | 369 | 458 | 393 | 304 | |||||||||||||||||||||

| Intangible Assets | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 468 | 536 | ||

| Total Assets | CZK mil | 262,513 | 288,314 | 308,765 | 324,053 | 346,505 | |||||||||||||||||||||

| Shareholders' Equity | CZK mil | 34,172 | 39,391 | 42,203 | 44,600 | 47,077 | |||||||||||||||||||||

| Of Which Minority Interest | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

| Liabilities | CZK mil | 228,341 | 248,923 | 266,562 | 279,453 | 299,428 | |||||||||||||||||||||

| Interbank Borrowing | CZK mil | 2.00 | 2.00 | 2.00 | 9.00 | 141 | |||||||||||||||||||||

| Customer Deposits | CZK mil | 402 | 398 | 57.0 | 31.0 | 2.00 | |||||||||||||||||||||

| Retail Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 283 | 298 | 0 | 0 | 0 | ||||||

| Corporate Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 119 | 100 | 57.0 | 0 | 0 | ||||||

| Issued Debt Securities | CZK mil | 226,579 | 247,011 | 264,165 | 277,396 | 295,325 | |||||||||||||||||||||

| Other Liabilities | CZK mil | 1,358 | 1,512 | 2,338 | 2,017 | 3,960 | |||||||||||||||||||||

| asset quality | |||||||||||||||||||||||||||

| Non-Performing Loans | CZK mil | ... | ... | ... | 5,945 | 4,700 | 3,815 | 1,357 | 1,182 | ||||||||||||||||||

| Gross Loans | CZK mil | ... | ... | ... | 256,639 | 282,531 | 301,081 | 323,124 | 345,584 | ||||||||||||||||||

| Risk-Weighted Assets | CZK mil | ... | ... | ... | 101,697 | 95,221 | 106,331 | 95,758 | 97,177 | ||||||||||||||||||

| Total Provisions | CZK mil | ... | ... | ... | 2,561 | 2,122 | 1,642 | 1,246 | 1,383 | ||||||||||||||||||

| growth rates | |||||||||||||||||||||||||||

| Customer Loan Growth | % | ... | 11.3 | 10.4 | 6.79 | 5.38 | 5.79 | ||||||||||||||||||||

| Retail Loan Growth | % | ... | 11.3 | 10.4 | 6.79 | 5.38 | 5.79 | ||||||||||||||||||||

| Mortgage Loan Growth | % | ... | 11.3 | 10.4 | 6.79 | 5.38 | 5.79 | ||||||||||||||||||||

| Total Asset Growth | % | ... | 11.1 | 9.83 | 7.09 | 4.95 | 6.93 | ||||||||||||||||||||

| Shareholders' Equity Growth | % | ... | 1.56 | 15.3 | 7.14 | 5.68 | 5.55 | ||||||||||||||||||||

| Customer Deposit Growth | % | ... | -11.1 | -0.995 | -85.7 | -45.6 | -93.5 | ||||||||||||||||||||

| Retail Deposit Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | -6.29 | 5.30 | -100 | ... | ... | ... | ... | |||

| Corporate Deposit Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | -20.7 | -16.0 | -43.0 | -100 | ... | ... | ... | |||

| market share | |||||||||||||||||||||||||||

| Market Share in Customer Loans | % | 8.61 | 9.09 | 9.06 | 9.15 | 9.28 | |||||||||||||||||||||

| Market Share in Retail Loans | % | 17.9 | 18.4 | 18.2 | 18.1 | 18.0 | |||||||||||||||||||||

| Market Share in Consumer Loans | % | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

| Market Share in Mortgage Loans | % | 24.1 | 24.4 | 24.0 | 23.7 | 23.3 | |||||||||||||||||||||

| Market Share in Total Assets | % | 4.40 | 4.12 | 4.24 | 4.28 | 4.35 | |||||||||||||||||||||

| Market Share in Customer Deposits | % | 0.011 | 0.010 | 0.001 | < 0.001 | < 0.001 | |||||||||||||||||||||

| Market Share in Retail Deposits | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0.013 | 0.013 | 0 | 0 | 0 | ||||||

| Market Share in Corporate Deposits | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0.013 | 0.010 | 0.005 | 0 | 0 |

| ratios | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| ROE | % | ... | 9.45 | 7.69 | 5.77 | 5.64 | 3.42 | ||||||||||||||||||||

| ROTE | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 3.45 | ||

| ROE (@ 15% of RWA) | % | ... | ... | ... | ... | 22.1 | 19.1 | 15.6 | 16.1 | 10.8 | |||||||||||||||||

| ROA | % | ... | 1.29 | 1.03 | 0.789 | 0.773 | 0.467 | ||||||||||||||||||||

| Return on Loans | % | 1.33 | 1.06 | 0.812 | 0.795 | 0.482 | |||||||||||||||||||||

| Operating Profit (As % of RWA) | % | ... | ... | ... | ... | 4.13 | 3.51 | 2.83 | 2.74 | 2.38 | |||||||||||||||||

| Costs (As % Of Assets) | % | ... | 0.429 | 0.356 | 0.332 | 0.313 | 0.291 | ||||||||||||||||||||

| Costs (As % Of Income) | % | 21.1 | 22.1 | 25.8 | 26.3 | 29.8 | |||||||||||||||||||||

| Costs (As % Of Loans) | % | ... | 0.443 | 0.367 | 0.342 | 0.322 | 0.301 | ||||||||||||||||||||

| Costs (As % Of Loans & Deposits) | % | ... | 0.442 | 0.367 | 0.342 | 0.322 | 0.301 | ||||||||||||||||||||

| Capital Adequacy Ratio | % | ... | 33.5 | 37.3 | 36.5 | 42.6 | 45.9 | ||||||||||||||||||||

| Tier 1 Ratio | % | ... | 32.9 | 37.3 | 36.5 | 42.6 | 45.9 | ||||||||||||||||||||

| Net Interest Margin | % | ... | 1.80 | 1.43 | 1.17 | 1.09 | 0.872 | ||||||||||||||||||||

| Interest Spread | % | ... | 1.64 | 1.27 | 0.979 | 0.854 | 0.662 | ||||||||||||||||||||

| Asset Yield | % | ... | 2.86 | 2.47 | 2.41 | 2.57 | 2.19 | ||||||||||||||||||||

| Revenues (As % of RWA) | % | ... | ... | ... | ... | 5.24 | 4.51 | 3.82 | 3.72 | 3.39 | |||||||||||||||||

| Cost Of Liabilities | % | ... | 1.23 | 1.20 | 1.43 | 1.72 | 1.53 | ||||||||||||||||||||

| Payout Ratio | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 56.1 | 100 | 151 | 100 | 100 | ... | ||||||||||

| Interest Income (As % Of Revenues) | % | 88.9 | 88.7 | 91.2 | 91.7 | 89.3 | |||||||||||||||||||||

| Fee Income (As % Of Revenues) | % | 10.3 | 12.6 | 11.5 | 6.62 | 5.78 | |||||||||||||||||||||

| Other Income (As % Of Revenues) | % | 0.810 | -1.33 | -2.73 | 1.68 | 4.89 | |||||||||||||||||||||

| Staff Cost (As % Of Total Cost) | % | 50.5 | 55.5 | 54.9 | 54.2 | 47.6 | |||||||||||||||||||||

| Equity (As % Of Assets) | % | 13.0 | 13.7 | 13.7 | 13.8 | 13.6 | |||||||||||||||||||||

| Equity (As % Of Loans) | % | 13.4 | 14.0 | 14.1 | 14.1 | 14.1 | |||||||||||||||||||||

| Loans (As % Of Deposits) | % | 112 | 114 | 113 | 114 | 113 | |||||||||||||||||||||

| Loans (As % Assets) | % | 96.8 | 97.3 | 97.0 | 97.4 | 96.3 | |||||||||||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 2.32 | 1.66 | 1.27 | 0.420 | 0.342 | ||||||||||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 43.1 | 45.1 | 43.0 | 91.8 | 117 | ||||||||||||||||||

| Provisions (As % Of Loans) | % | ... | ... | ... | 1.01 | 0.757 | 0.548 | 0.395 | 0.414 | ||||||||||||||||||

| Cost of Provisions (As % Of Loans) | % | ... | 0.019 | -0.008 | -0.048 | -0.082 | 0.110 |

| other data | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Branches | ... | 29.0 | 30.0 | 30.0 | 29.0 | 29.0 | |||||||||||||||||||||

| Employees | ... | 545 | 548 | 526 | 497 | 419 | |||||||||||||||||||||

| Employees Per Bank Branch | ... | 18.8 | 18.3 | 17.5 | 17.1 | 14.4 | |||||||||||||||||||||

| Cost Per Employee | USD per month | ... | 3,272 | 3,525 | 3,946 | 3,990 | 4,203 | ||||||||||||||||||||

| Cost Per Employee (Local Currency) | CZK per month | ... | 82,569 | 82,725 | 86,343 | 89,944 | 92,482 |

| customer breakdown | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Customers | mil | ... | ... | ... | ... | ... | ... | ... | ... | 0.188 | 0.201 | 0.206 | 0.223 | 0.230 | |||||||||||||

| Number of Mortgages | mil | ... | ... | ... | ... | ... | ... | ... | ... | 0.188 | 0.201 | 0.206 | 0.223 | ... | ... | ... | |||||||||||

| Average Size of Mortgage Loan | CZK | ... | ... | ... | ... | ... | ... | ... | ... | 1,352,000 | 1,393,000 | 1,451,000 | 1,414,230 | ... | ... | ... | |||||||||||

| Mortgages (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | 100 | 100 | 100 | 100 | ... | ... | ... | |||||||||||

| Revenue per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | 26,931 | 22,052 | 18,632 | 16,851 | 14,222 | |||||||||||||

| Net Profit per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | 17,060 | 14,049 | 11,407 | 10,962 | 6,809 | |||||||||||||

| Loan per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | 1,352,000 | 1,393,000 | 1,451,000 | 1,414,230 | 1,451,457 | |||||||||||||

| Deposit per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | 2,139 | 1,977 | 276 | 139 | 8.70 | |||||||||||||

| Revenue per Customer | USD | ... | ... | ... | ... | ... | ... | ... | ... | 1,067 | 940 | 852 | 747 | 646 | |||||||||||||

| Net Profit per Customer | USD | ... | ... | ... | ... | ... | ... | ... | ... | 676 | 599 | 521 | 486 | 309 | |||||||||||||

| Loan per Customer | USD | ... | ... | ... | ... | ... | ... | ... | ... | 52,732 | 65,427 | 64,586 | 62,518 | 67,866 | |||||||||||||

| Deposit per Customer | USD | ... | ... | ... | ... | ... | ... | ... | ... | 83.4 | 92.9 | 12.3 | 6.14 | 0.407 |

Get all company financials in excel:

By Helgi Library - November 23, 2023

Hypotecni Banka's non-performing loans reached 0.581% of total loans at the end of 2023-09-30, down from 0.675% compared to the previous year. Historically, the NPL ratio hit an all time high of 6.72% in 2000-06-30 and an all time low of 0.572% in 2023-06-30. ...

By Helgi Library - September 30, 2023

Hypotecni Banka's customer loans reached CZK 385,733 mil in 2023-06-30, up 0.516% compared to the previous year. Czech banking sector provided customer loans of CZK 4,206 in 2023-06-30, up 2.15% when compared to the last year. Hypotecni Banka accounted fo...

By Helgi Library - November 23, 2023

Hypotecni Banka's capital adequacy ratio reached 52.1% at the end of third quarter of 2023, down from 52.2% when compared to the previous quarter. Historically, the bank’s capital ratio hit an all time high of 56.4% in 2Q2008 and an all time low of 8.16% in 4Q2002....

By Helgi Library - September 30, 2023

Hypotecni Banka's retail loans reached CZK 385,733 mil in the second quarter of 2023, up 0.843% compared to the previous year. Czech banking sector provided retail loans of CZK 2,203 bil in 2Q2023, up 2.19% when compared to the last year. Hypotecni Banka ...

By Helgi Library - November 23, 2023

Hypotecni Banka made a net profit of CZK 500 mil in the third quarter of 2023, down 32.1% when compared to the same period of last year. This implies a return on equity of 3.50%. Historically, the bank’s net profit reached an all time high of CZK 973 mil in 4Q202...

By Helgi Library - November 23, 2023

Hypotecni Banka made a net profit of CZK 500 mil under revenues of CZK 894 mil in the third quarter of 2023, down 32.1% and 22.4% respectively when compared to the same period last year. Historically, the bank’s net profit reached an all time high of CZK 973 ...

By Helgi Library - November 23, 2023

Hypotecni Banka's net interest margin amounted to 0.815% in the third quarter of 2023, down from 0.925% when compared to the previous quarter. Historically, the bank’s net interest margin reached an all time high of 9.76% in 4Q2000 and an all time low of ...

By Helgi Library - September 30, 2023

Hypotecni Banka generated total banking revenues of CZK 1,069 mil in 2023-06-30, up 0.231% compared to the previous year. Czech banking sector banking sector generated total revenues of CZK 67,123 mil in 2023-06-30, up 20.3% when compared to the last ...

By Helgi Library - November 23, 2023

Hypotecni Banka's cost to income ratio reached 35.7% in the third quarter of 2023, up from 30.3% when compared to the previous quarter. Historically, the bank’s costs reached an all time high of 65.9% of income in 4Q2021 and an all time low of 7.70% in 4Q202...

By Helgi Library - November 23, 2023

Hypotecni Banka's loans reached in the first quarter of 1970, down from when compared to the previous quarter and down from when compared to the same period of last year. Historically, the bank’s loans reached an all time high of CZK mil in ...

Hypoteční Banka is the Czech Republic's largest mortgage lender with a market share of around 25%. Despite being a 100% subsidiary of ČSOB, Hypoteční has kept its distinctive brand name and relatively high level of independence. The numbers suggest that the bank possesses all the right ingredients for success; it is exposed to the fastest-growing area of banking (mortgage lending), it is extremely cost-efficient and its asset quality remains under good control. When adjusted for hefty overcapitalisation, Hypoteční Banka’s ROE jumps to impressive 20's% being on eof the most profitable banks on the Czech market in the last decade.

Hypotecni Banka has been growing its revenues and asset by -2.53% and 6.83% a year on average in the last 10 years. Its loans and deposits have grown by 7.74% and -41.6% a year during that time and loans to deposits ratio reached 116% at the end of 2022. The company achieved an average return on equity of 6.95% in the last decade with net profit growing -1.18% a year on average. In terms of operating efficiency, its cost to income ratio reached 20.0% in 2022, compared to 23.7% average in the last decade.

Equity represented 14.7% of total assets or 15.0% of loans at the end of 2022. Hypotecni Banka's non-performing loans were 0.584% of total loans while provisions covered some 34.4% of NPLs at the end of 2022.

Helgi Library

Helgi Library