By Helgi Library - May 5, 2024

MONETA Money Bank's net interest margin amounted to 1.79% in the first quarter of 2024, down from 1.92% when compared to the pre...

By Helgi Library - May 5, 2024

MONETA Money Bank's customer deposits reached CZK 399,497 mil in 2023-12-31, up 1.65% compared to the previous year. Czech bank...

By Helgi Library - February 16, 2024

MONETA Money Bank's customer loans reached CZK 268,987 mil in 2023-09-30, up 0.358% compared to the previous year. Czech bankin...

| Profit Statement | 2021 | 2022 | 2023 | |

| Net Interest Income | CZK mil | 8,609 | 9,311 | 8,577 |

| Net Fee Income | CZK mil | 2,050 | 2,298 | 2,624 |

| Other Income | CZK mil | 509 | 507 | 946 |

| Total Revenues | CZK mil | 11,168 | 12,116 | 12,147 |

| Staff Cost | CZK mil | 2,562 | 2,528 | 2,504 |

| Operating Profit | CZK mil | 5,630 | 6,522 | 6,417 |

| Provisions | CZK mil | 695 | 90.0 | 305 |

| Net Profit | CZK mil | 3,984 | 5,187 | 5,200 |

| Balance Sheet | 2021 | 2022 | 2023 | |

| Interbank Loans | CZK mil | 15,602 | 37,886 | 69,632 |

| Customer Loans | CZK mil | 255,612 | 268,752 | 263,064 |

| Investments | CZK mil | 49,200 | 57,951 | 104,353 |

| Total Assets | CZK mil | 340,222 | 387,510 | 458,184 |

| Shareholders' Equity | CZK mil | 29,481 | 31,091 | 32,203 |

| Interbank Borrowing | CZK mil | 12,580 | 5,953 | 5,423 |

| Customer Deposits | CZK mil | 285,145 | 334,251 | 399,497 |

| Issued Debt Securities | CZK mil | 7,106 | 10,207 | 11,412 |

| Ratios | 2021 | 2022 | 2023 | |

| ROE | % | 14.1 | 17.1 | 16.4 |

| ROA | % | 1.24 | 1.43 | 1.23 |

| Costs (As % Of Assets) | % | 1.73 | 1.54 | 1.36 |

| Costs (As % Of Income) | % | 49.6 | 46.2 | 47.2 |

| Capital Adequacy Ratio | % | 17.1 | 18.0 | 20.1 |

| Net Interest Margin | % | 2.69 | 2.56 | 2.03 |

| Loans (As % Of Deposits) | % | 89.6 | 80.4 | 65.8 |

| NPLs (As % Of Loans) | % | 2.20 | 1.40 | 1.40 |

| Provisions (As % Of NPLs) | % | 101 | 135 | 122 |

| Valuation | 2021 | 2022 | 2023 | |

| Market Capitalisation | USD mil | 2,182 | 1,717 | 2,138 |

| Number Of Shares | mil | 511 | 511 | 511 |

| Share Price | CZK | 93.8 | 76.0 | 93.6 |

| Price/Earnings (P/E) | 12.0 | 7.49 | 9.20 | |

| Price/Book Value (P/BV) | 1.62 | 1.25 | 1.49 | |

| Dividend Yield | % | 3.20 | 10.5 | 9.62 |

| Earnings Per Share (EPS) | CZK | 7.80 | 10.2 | 10.2 |

| Book Value Per Share | CZK | 57.7 | 60.8 | 63.0 |

| Dividend Per Share | CZK | 3.00 | 8.00 | 9.00 |

Get all company financials in excel:

| summary | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| income statement | |||||||||||||||||||||||||

| Net Interest Income | CZK mil | 7,364 | 7,409 | 7,925 | 8,282 | 8,609 | |||||||||||||||||||

| Total Revenues | CZK mil | 10,241 | 10,162 | 10,519 | 12,098 | 11,168 | |||||||||||||||||||

| Operating Profit | CZK mil | 5,388 | 5,310 | 5,500 | 6,572 | 5,630 | |||||||||||||||||||

| Net Profit | CZK mil | 3,923 | 4,200 | 4,019 | 2,601 | 3,984 | |||||||||||||||||||

| balance sheet | |||||||||||||||||||||||||

| Interbank Loans | CZK mil | 53,380 | 33,436 | 23,485 | 22,872 | 15,602 | |||||||||||||||||||

| Customer Loans | CZK mil | 123,680 | 140,123 | 156,409 | 226,072 | 255,612 | |||||||||||||||||||

| Investments | CZK mil | 11,828 | 20,780 | 25,972 | 35,917 | 49,200 | |||||||||||||||||||

| Total Assets | CZK mil | 199,734 | 206,932 | 219,053 | 300,958 | 340,222 | |||||||||||||||||||

| Shareholders' Equity | CZK mil | 25,763 | 25,237 | 24,411 | 27,050 | 29,481 | |||||||||||||||||||

| Interbank Borrowing | CZK mil | 29,643 | 10,716 | 7,091 | 1,977 | 12,580 | |||||||||||||||||||

| Customer Deposits | CZK mil | 141,469 | 168,792 | 181,523 | 258,906 | 285,145 | |||||||||||||||||||

| Issued Debt Securities | CZK mil | ... | ... | 68.0 | 0 | 2,006 | 7,393 | 7,106 | |||||||||||||||||

| ratios | |||||||||||||||||||||||||

| ROE | % | ... | 14.8 | 16.5 | 16.2 | 10.1 | 14.1 | ||||||||||||||||||

| ROA | % | ... | 2.25 | 2.07 | 1.89 | 1.00 | 1.24 | ||||||||||||||||||

| Costs (As % Of Assets) | % | ... | 2.78 | 2.39 | 2.36 | 2.13 | 1.73 | ||||||||||||||||||

| Costs (As % Of Income) | % | 47.4 | 47.7 | 47.7 | 45.7 | 49.6 | |||||||||||||||||||

| Capital Adequacy Ratio | % | 17.4 | 16.4 | 18.0 | 18.2 | 17.1 | |||||||||||||||||||

| Net Interest Margin | % | ... | 4.22 | 3.64 | 3.72 | 3.19 | 2.69 | ||||||||||||||||||

| Interest Income (As % Of Revenues) | % | 71.9 | 72.9 | 75.3 | 68.5 | 77.1 | |||||||||||||||||||

| Fee Income (As % Of Revenues) | % | 18.9 | 18.6 | 18.5 | 15.6 | 18.4 | |||||||||||||||||||

| Staff Cost (As % Of Total Cost) | % | 50.6 | 47.9 | 46.2 | 45.6 | 46.3 | |||||||||||||||||||

| Equity (As % Of Assets) | % | 12.9 | 12.2 | 11.1 | 8.99 | 8.67 | |||||||||||||||||||

| Loans (As % Of Deposits) | % | 87.4 | 83.0 | 86.2 | 87.3 | 89.6 | |||||||||||||||||||

| Loans (As % Assets) | % | 61.9 | 67.7 | 71.4 | 75.1 | 75.1 | |||||||||||||||||||

| NPLs (As % Of Loans) | % | 4.10 | 2.80 | 1.80 | 2.30 | 2.20 | |||||||||||||||||||

| Provisions (As % Of NPLs) | % | 76.8 | 99.9 | 109 | 110 | 101 | |||||||||||||||||||

| valuation | |||||||||||||||||||||||||

| Market Capitalisation | USD mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1,978 | 1,649 | 1,920 | 1,625 | 2,182 | |||

| Number Of Shares | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 511 | 511 | 511 | 511 | 511 | ||||

| Share Price | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 82.4 | 72.5 | 85.0 | 68.0 | 93.8 | |||

| Earnings Per Share (EPS) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 7.68 | 8.22 | 7.86 | 5.09 | 7.80 | ||||

| Book Value Per Share | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 50.4 | 49.4 | 47.8 | 52.9 | 57.7 | ||||

| Dividend Per Share | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 8.00 | 9.45 | 3.30 | 0 | 3.00 | ||||

| Price/Earnings (P/E) | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 10.7 | 8.82 | 10.8 | 13.4 | 12.0 | ||||

| Price/Book Value (P/BV) | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.63 | 1.47 | 1.78 | 1.28 | 1.62 | ||||

| Dividend Yield | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 9.71 | 13.0 | 3.88 | 0 | 3.20 | |||

| Earnings Per Share Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | -3.23 | 7.06 | -4.31 | -35.3 | 53.2 | |||

| Book Value Per Share Growth | % | ... | -5.52 | -2.04 | -3.27 | 10.8 | 8.99 |

| income statement | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| income statement | |||||||||||||||||||||||||

| Interest Income | CZK mil | 7,582 | 7,820 | 8,933 | 9,712 | 9,649 | |||||||||||||||||||

| Interest Cost | CZK mil | 218 | 411 | 1,008 | 1,430 | 1,040 | |||||||||||||||||||

| Net Interest Income | CZK mil | 7,364 | 7,409 | 7,925 | 8,282 | 8,609 | |||||||||||||||||||

| Net Fee Income | CZK mil | 1,933 | 1,892 | 1,950 | 1,891 | 2,050 | |||||||||||||||||||

| Fee Income | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2,528 | ||

| Fee Expense | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 478 | ||

| Other Income | CZK mil | 944 | 861 | 644 | 1,925 | 509 | |||||||||||||||||||

| Total Revenues | CZK mil | 10,241 | 10,162 | 10,519 | 12,098 | 11,168 | |||||||||||||||||||

| Staff Cost | CZK mil | 2,456 | 2,324 | 2,318 | 2,519 | 2,562 | |||||||||||||||||||

| Depreciation | CZK mil | 414 | 610 | 967 | 1,129 | 1,196 | |||||||||||||||||||

| Other Cost | CZK mil | 1,983 | 1,918 | 1,734 | 1,878 | 1,780 | |||||||||||||||||||

| Operating Cost | CZK mil | 4,853 | 4,852 | 5,019 | 5,526 | 5,538 | |||||||||||||||||||

| Operating Profit | CZK mil | 5,388 | 5,310 | 5,500 | 6,572 | 5,630 | |||||||||||||||||||

| Provisions | CZK mil | 381 | 274 | 717 | 3,562 | 695 | |||||||||||||||||||

| Extra and Other Cost | CZK mil | 104 | 0 | -200 | 0 | 0 | |||||||||||||||||||

| Pre-Tax Profit | CZK mil | 4,903 | 5,036 | 4,983 | 3,010 | 4,935 | |||||||||||||||||||

| Tax | CZK mil | 980 | 836 | 964 | 409 | 951 | |||||||||||||||||||

| Minorities | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||

| Net Profit | CZK mil | 3,923 | 4,200 | 4,019 | 2,601 | 3,984 | |||||||||||||||||||

| Net Profit Avail. to Common | CZK mil | 3,923 | 4,200 | 4,019 | 2,601 | 3,984 | |||||||||||||||||||

| Dividends | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4,088 | 4,829 | 1,686 | 0 | 1,533 | ||||

| growth rates | |||||||||||||||||||||||||

| Net Interest Income Growth | % | ... | -11.3 | 0.611 | 6.96 | 4.50 | 3.95 | ||||||||||||||||||

| Net Fee Income Growth | % | ... | -1.43 | -2.12 | 3.07 | -3.03 | 8.41 | ||||||||||||||||||

| Total Revenue Growth | % | ... | -7.39 | -0.771 | 3.51 | 15.0 | -7.69 | ||||||||||||||||||

| Operating Cost Growth | % | ... | -4.54 | -0.021 | 3.44 | 10.1 | 0.217 | ||||||||||||||||||

| Operating Profit Growth | % | ... | -9.81 | -1.45 | 3.58 | 19.5 | -14.3 | ||||||||||||||||||

| Pre-Tax Profit Growth | % | ... | -2.85 | 2.71 | -1.05 | -39.6 | 64.0 | ||||||||||||||||||

| Net Profit Growth | % | ... | -3.23 | 7.06 | -4.31 | -35.3 | 53.2 | ||||||||||||||||||

| market share | |||||||||||||||||||||||||

| Market Share in Revenues | % | 5.72 | 5.34 | 5.20 | 6.71 | 6.06 | |||||||||||||||||||

| Market Share in Net Profit | % | 5.21 | 5.16 | 4.41 | 5.48 | 5.66 | |||||||||||||||||||

| Market Share in Employees | % | 7.91 | 7.47 | 7.11 | 7.39 | 7.51 | |||||||||||||||||||

| Market Share in Bank Cards | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |||||||||||||

| Market Share in Debit Cards | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Market Share in Credit Cards | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Market Share in Branches | % | 11.7 | 10.3 | 9.43 | 9.46 | 9.65 |

| balance sheet | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| balance sheet | |||||||||||||||||||||||||

| Cash & Cash Equivalents | CZK mil | 7,127 | 8,139 | 6,697 | 7,782 | 11,204 | |||||||||||||||||||

| Interbank Loans | CZK mil | 53,380 | 33,436 | 23,485 | 22,872 | 15,602 | |||||||||||||||||||

| Customer Loans | CZK mil | 123,680 | 140,123 | 156,409 | 226,072 | 255,612 | |||||||||||||||||||

| Retail Loans | CZK mil | 61,984 | 74,799 | 89,897 | 151,128 | 174,784 | |||||||||||||||||||

| Mortgage Loans | CZK mil | 20,338 | 31,615 | 43,737 | 97,629 | 122,634 | |||||||||||||||||||

| Consumer Loans | CZK mil | 41,646 | 43,184 | 46,160 | 53,499 | 52,150 | |||||||||||||||||||

| Corporate Loans | CZK mil | 61,696 | 65,319 | 66,774 | 75,498 | 80,896 | |||||||||||||||||||

| Investments | CZK mil | 11,828 | 20,780 | 25,972 | 35,917 | 49,200 | |||||||||||||||||||

| Property and Equipment | CZK mil | ... | ... | ... | 872 | 1,296 | 2,948 | 2,696 | 2,631 | ||||||||||||||||

| Intangible Assets | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1,301 | 1,789 | 2,283 | 2,957 | 3,184 | |||

| Goodwill | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 8.00 | ... | ... | ... | ... | ... | ... | |

| Total Assets | CZK mil | 199,734 | 206,932 | 219,053 | 300,958 | 340,222 | |||||||||||||||||||

| Shareholders' Equity | CZK mil | 25,763 | 25,237 | 24,411 | 27,050 | 29,481 | |||||||||||||||||||

| Of Which Minority Interest | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||

| Liabilities | CZK mil | 173,971 | 181,695 | 194,642 | 273,908 | 310,741 | |||||||||||||||||||

| Interbank Borrowing | CZK mil | 29,643 | 10,716 | 7,091 | 1,977 | 12,580 | |||||||||||||||||||

| Customer Deposits | CZK mil | 141,469 | 168,792 | 181,523 | 258,906 | 285,145 | |||||||||||||||||||

| Retail Deposits | CZK mil | 83,021 | 94,448 | 115,863 | 193,352 | 216,915 | |||||||||||||||||||

| Corporate Deposits | CZK mil | 48,503 | 54,428 | 58,096 | 63,174 | 67,920 | |||||||||||||||||||

| Sight Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 116,907 | ||

| Term Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 168,238 | ||

| Issued Debt Securities | CZK mil | ... | ... | 68.0 | 0 | 2,006 | 7,393 | 7,106 | |||||||||||||||||

| Subordinated Debt | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2,006 | 4,681 | 4,684 | ||

| Other Liabilities | CZK mil | ... | ... | 2,791 | 2,187 | 4,022 | 5,632 | 5,910 | |||||||||||||||||

| asset quality | |||||||||||||||||||||||||

| Non-Performing Loans | CZK mil | 5,236 | 3,923 | 2,820 | 5,212 | 5,625 | |||||||||||||||||||

| Gross Loans | CZK mil | 127,700 | 140,118 | 156,671 | 226,626 | 255,680 | |||||||||||||||||||

| Risk-Weighted Assets | CZK mil | 118,547 | 122,202 | 125,629 | 154,131 | 169,241 | |||||||||||||||||||

| Total Provisions | CZK mil | 4,020 | 3,919 | 3,080 | 5,744 | 5,692 | |||||||||||||||||||

| growth rates | |||||||||||||||||||||||||

| Customer Loan Growth | % | ... | 10.6 | 13.3 | 11.6 | 44.5 | 13.1 | ||||||||||||||||||

| Retail Loan Growth | % | ... | -4.91 | 20.7 | 20.2 | 68.1 | 15.7 | ||||||||||||||||||

| Mortgage Loan Growth | % | ... | 30.6 | 55.4 | 38.3 | 123 | 25.6 | ||||||||||||||||||

| Consumer Loan Growth | % | ... | -16.1 | 3.69 | 6.89 | 15.9 | -2.52 | ||||||||||||||||||

| Corporate Loan Growth | % | ... | 32.2 | 5.87 | 2.23 | 13.1 | 7.15 | ||||||||||||||||||

| Total Asset Growth | % | ... | 33.7 | 3.60 | 5.86 | 37.4 | 13.0 | ||||||||||||||||||

| Shareholders' Equity Growth | % | ... | -5.52 | -2.04 | -3.27 | 10.8 | 8.99 | ||||||||||||||||||

| Customer Deposit Growth | % | ... | 21.7 | 19.3 | 7.54 | 42.6 | 10.1 | ||||||||||||||||||

| Retail Deposit Growth | % | ... | 13.5 | 13.8 | 22.7 | 66.9 | 12.2 | ||||||||||||||||||

| Corporate Deposit Growth | % | ... | 14.4 | 12.2 | 6.74 | 8.74 | 7.51 | ||||||||||||||||||

| market share | |||||||||||||||||||||||||

| Market Share in Customer Loans | % | 4.01 | 4.24 | 4.53 | 6.29 | 6.64 | |||||||||||||||||||

| Market Share in Corporate Loans | % | 6.04 | 6.05 | 5.96 | 6.72 | 6.81 | |||||||||||||||||||

| Market Share in Retail Loans | % | 4.06 | 4.55 | 5.15 | 8.13 | 8.55 | |||||||||||||||||||

| Market Share in Consumer Loans | % | 10.9 | 10.8 | 11.1 | 12.7 | 11.6 | |||||||||||||||||||

| Market Share in Mortgage Loans | % | 1.77 | 2.54 | 3.29 | 6.80 | 7.69 | |||||||||||||||||||

| Market Share in Total Assets | % | 2.85 | 2.84 | 2.90 | 3.78 | 3.99 | |||||||||||||||||||

| Market Share in Customer Deposits | % | 3.39 | 3.80 | 3.83 | 5.02 | 5.18 | |||||||||||||||||||

| Market Share in Retail Deposits | % | 3.50 | 3.69 | 4.25 | 6.33 | 6.64 | |||||||||||||||||||

| Market Share in Corporate Deposits | % | 4.87 | 5.23 | 5.31 | 5.19 | 5.19 |

| ratios | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| ROE | % | ... | 14.8 | 16.5 | 16.2 | 10.1 | 14.1 | ||||||||||||||||||

| ROTE | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 15.4 | 17.5 | 17.6 | 11.3 | 15.8 | ||

| ROE (@ 15% of RWA) | % | ... | 23.0 | 23.3 | 21.6 | 12.4 | 16.4 | ||||||||||||||||||

| ROA | % | ... | 2.25 | 2.07 | 1.89 | 1.00 | 1.24 | ||||||||||||||||||

| Return on Loans | % | 3.33 | 3.18 | 2.71 | 1.36 | 1.65 | |||||||||||||||||||

| Operating Profit (As % of RWA) | % | ... | 4.73 | 4.41 | 4.44 | 4.70 | 3.48 | ||||||||||||||||||

| Costs (As % Of Assets) | % | ... | 2.78 | 2.39 | 2.36 | 2.13 | 1.73 | ||||||||||||||||||

| Costs (As % Of Income) | % | 47.4 | 47.7 | 47.7 | 45.7 | 49.6 | |||||||||||||||||||

| Costs (As % Of Loans) | % | ... | 4.12 | 3.68 | 3.39 | 2.89 | 2.30 | ||||||||||||||||||

| Costs (As % Of Loans & Deposits) | % | ... | 1.97 | 1.69 | 1.55 | 1.34 | 1.08 | ||||||||||||||||||

| Capital Adequacy Ratio | % | 17.4 | 16.4 | 18.0 | 18.2 | 17.1 | |||||||||||||||||||

| Tier 1 Ratio | % | 17.4 | 16.4 | 16.4 | 15.2 | 14.4 | |||||||||||||||||||

| Net Interest Margin | % | ... | 4.22 | 3.64 | 3.72 | 3.19 | 2.69 | ||||||||||||||||||

| Interest Spread | % | ... | 4.20 | 3.61 | 3.66 | 3.12 | 2.65 | ||||||||||||||||||

| Asset Yield | % | ... | 4.34 | 3.85 | 4.19 | 3.74 | 3.01 | ||||||||||||||||||

| Revenues (As % of RWA) | % | ... | 8.99 | 8.44 | 8.49 | 8.65 | 6.91 | ||||||||||||||||||

| Cost Of Liabilities | % | ... | 0.147 | 0.231 | 0.536 | 0.610 | 0.356 | ||||||||||||||||||

| Payout Ratio | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 104 | 115 | 42.0 | 0 | 38.5 | ||||

| Interest Income (As % Of Revenues) | % | 71.9 | 72.9 | 75.3 | 68.5 | 77.1 | |||||||||||||||||||

| Fee Income (As % Of Revenues) | % | 18.9 | 18.6 | 18.5 | 15.6 | 18.4 | |||||||||||||||||||

| Other Income (As % Of Revenues) | % | 9.22 | 8.47 | 6.12 | 15.9 | 4.56 | |||||||||||||||||||

| Staff Cost (As % Of Total Cost) | % | 50.6 | 47.9 | 46.2 | 45.6 | 46.3 | |||||||||||||||||||

| Equity (As % Of Assets) | % | 12.9 | 12.2 | 11.1 | 8.99 | 8.67 | |||||||||||||||||||

| Equity (As % Of Loans) | % | 20.8 | 18.0 | 15.6 | 12.0 | 11.5 | |||||||||||||||||||

| Loans (As % Of Deposits) | % | 87.4 | 83.0 | 86.2 | 87.3 | 89.6 | |||||||||||||||||||

| Loans (As % Assets) | % | 61.9 | 67.7 | 71.4 | 75.1 | 75.1 | |||||||||||||||||||

| NPLs (As % Of Loans) | % | 4.10 | 2.80 | 1.80 | 2.30 | 2.20 | |||||||||||||||||||

| Provisions (As % Of NPLs) | % | 76.8 | 99.9 | 109 | 110 | 101 | |||||||||||||||||||

| Provisions (As % Of Loans) | % | 3.25 | 2.80 | 1.97 | 2.54 | 2.23 | |||||||||||||||||||

| Cost of Provisions (As % Of Loans) | % | ... | 0.324 | 0.208 | 0.484 | 1.86 | 0.289 |

| other data | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| Branches | 227 | 202 | 179 | 159 | 154 | ||||||||||||||||||||

| ATMs | 668 | 654 | 632 | 555 | 560 | ||||||||||||||||||||

| ATMs (As % of Bank Branches) | % | 294 | 324 | 353 | 349 | 364 | |||||||||||||||||||

| Employees | 3,312 | 3,129 | 2,959 | 3,009 | 2,981 | ||||||||||||||||||||

| Employees Per Bank Branch | 14.6 | 15.5 | 16.5 | 18.9 | 19.4 | ||||||||||||||||||||

| Cost Per Employee | USD per month | 2,634 | 2,829 | 2,896 | 3,170 | 3,305 | |||||||||||||||||||

| Cost Per Employee (Local Currency) | CZK per month | 61,795 | 61,894 | 65,281 | 69,763 | 71,620 |

| customer breakdown | Unit | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 |

| Customers | mil | 1.03 | 1.04 | 1.05 | 1.36 | 1.40 | |||||||||||||||||||

| Number of Primary Customers | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0.655 | ... | ... | ... |

| Payment Cards | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |||||||||||||

| Debit Cards | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Credit Cards | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Number of Mortgages | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0.015 | 0.022 | 0.030 | 0.068 | 0.082 | ... | |||||

| Number of Consumer Loans | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0.193 | 0.179 | 0.176 | 0.190 | 0.196 | ... | |

| Average Size of Mortgage Loan | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1,393,000 | 1,451,000 | 1,444,000 | 1,444,000 | 1,487,320 | ... | |||||

| Average Size of Consumer Loan | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 216,261 | 241,821 | 262,399 | 282,264 | 266,353 | ... | |

| Primary (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 48.3 | ... | ... | ... |

| Mortgages (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.41 | 2.10 | 2.88 | 4.98 | 5.89 | ... | |||||

| Consumer Loans (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 18.6 | 17.2 | 16.8 | 14.0 | 14.0 | ... | |

| Payments Cards (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |||||||||||||

| Debit Cards (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Credit Cards (As % of Total Clients) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||||||||||

| Market Value per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 40,761 | 35,760 | 41,367 | 25,606 | 34,243 | |||

| Revenue per Customer (Local Currency) | CZK | 9,914 | 9,809 | 10,018 | 8,915 | 7,983 | |||||||||||||||||||

| Net Profit per Customer (Local Currency) | CZK | 3,798 | 4,054 | 3,828 | 1,917 | 2,848 | |||||||||||||||||||

| Loan per Customer (Local Currency) | CZK | 119,729 | 135,254 | 148,961 | 166,597 | 182,711 | |||||||||||||||||||

| Deposit per Customer (Local Currency) | CZK | 136,950 | 162,927 | 172,879 | 190,793 | 203,821 | |||||||||||||||||||

| Market Value per Customer | USD | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1,914 | 1,592 | 1,829 | 1,197 | 1,560 | |||

| Revenue per Customer | USD | 422 | 448 | 444 | 405 | 368 | |||||||||||||||||||

| Net Profit per Customer | USD | 162 | 185 | 170 | 87.1 | 131 | |||||||||||||||||||

| Loan per Customer | USD | 5,623 | 6,020 | 6,585 | 7,790 | 8,324 | |||||||||||||||||||

| Deposit per Customer | USD | 6,432 | 7,252 | 7,642 | 8,921 | 9,285 |

Get all company financials in excel:

By Helgi Library - May 5, 2024

MONETA Money Bank made a net profit of CZK 1,286 mil in the first quarter of 2024, up 5.84% when compared to the same period of last year. This implies a return on equity of 15.7%. Historically, the bank’s net profit reached an all time high of CZK 1,582 mil in 2...

By Helgi Library - May 5, 2024

MONETA Money Bank made a net profit of CZK 1,286 mil under revenues of CZK 3,117 mil in the first quarter of 2024, up 5.84% and 9.6% respectively when compared to the same period last year. Historically, the bank’s net profit reached an all time high of CZK 1...

By Helgi Library - May 5, 2024

MONETA Money Bank's mortgage loans reached CZK 128,008 mil in 1Q2024, up 0.347% compared to the previous year. Czech banking sector provided mortgage loans of CZK 1,755 bil in 1Q2024, up 0.738% when compared to the last year. MONETA Money Bank accounted f...

By Helgi Library - May 5, 2024

MONETA Money Bank's non-performing loans reached 1.40% of total loans at the end of 2024-03-31, up from 1.30% compared to the previous year. Historically, the NPL ratio hit an all time high of 18.6% in 2011-03-31 and an all time low of 1.30% in 2023-09-30. ...

By Helgi Library - May 5, 2024

MONETA Money Bank employed 2,510 persons in 2024-03-31, down 0.040% compared to the previous year. Historically, the bank's workforce hit an all time high of 3,486 persons in 2011-12-31 and an all time low of 1,877 in 2003-06-30. The bank operated a network of...

By Helgi Library - May 5, 2024

MONETA Money Bank's retail deposits reached CZK 312,998 mil in 2023-12-31, up 5.04% compared to the previous year. Czech banking sector accepted retail deposits of CZK 3,651 bil in 2023-12-31, up 2.05% when compared to the last year. MONETA Money Bank acc...

By Helgi Library - May 5, 2024

MONETA Money Bank's retail loans reached CZK 179,535 mil in the fourth quarter of 2023, down 1.12% compared to the previous year. Czech banking sector provided retail loans of CZK 2,242 bil in 4Q2023, up 0.906% when compared to the last year. MONETA Money...

By Helgi Library - May 5, 2024

MONETA Money Bank's loans reached CZK 267,448 mil in the first quarter of 2024, up from CZK 263,897 mil when compared to the previous quarter and up from CZK 267,312 mil when compared to the same period of last year. Historically, the bank’s loans r...

By Helgi Library - May 5, 2024

MONETA Money Bank's cost to income ratio reached 47.7% in the first quarter of 2024, down from 49.7% when compared to the previous quarter. Historically, the bank’s costs reached an all time high of 59.1% of income in 4Q2010 and an all time low of 32.2% in 4...

By Helgi Library - May 5, 2024

MONETA Money Bank's corporate deposits reached CZK 86,229 mil in 2023-12-31, down 8.89% compared to the previous year. Czech banking sector accepted corporate deposits of CZK 1,470 bil in 2023-12-31, up 3.25% when compared to the last year. MONETA Money B...

MONETA Money Bank is a medium-sized bank based in Prague, the Czech Republic. Since its acquisition of the troubled Agrobanka in 1997, the Bank has developed a branch network of almost 200 branches and 600 ATMs (2019), though its focus has been shifting towards purely consumer finance in the last decade. Now, with over 1 million retail clients, the bank is primarily focused on consumer finance, ranging from instalment payments, leasing, credit cards and consumer lending to mortgage loans, although less so for the latter in recent years.

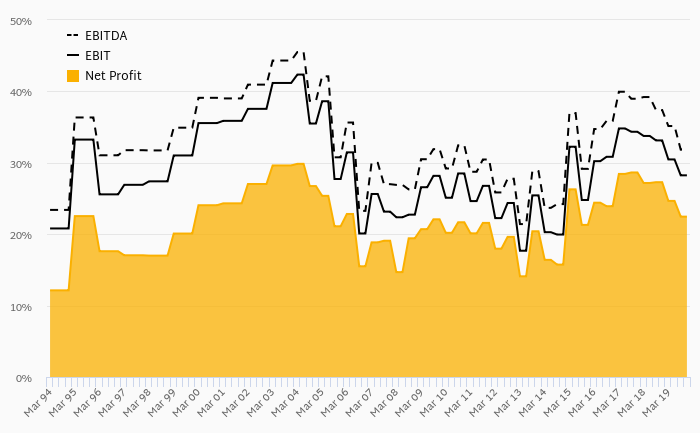

MONETA Money Bank has been growing its revenues and asset by -1.10% and 13.0% a year on average in the last 10 years. Its loans and deposits have grown by 10.4% and 15.6% a year during that time and loans to deposits ratio reached 65.8% at the end of 2023. The company achieved an average return on equity of 14.3% in the last decade with net profit growing 2.02% a year on average. In terms of operating efficiency, its cost to income ratio reached 47.2% in 2023, compared to 46.6% average in the last decade.

Equity represented 7.03% of total assets or 12.2% of loans at the end of 2023. MONETA Money Bank's non-performing loans were 1.40% of total loans while provisions covered some 122% of NPLs at the end of 2023.

MONETA Money Bank stock traded at per share at the end of 2023 resulting in a market capitalization of . Over the previous three years, stock price rose by 0% or 0% a year on average. That’s compared to an average ROE of 15.9% the bank generated for its shareholders. This closing price put stock at a 12-month trailing price to earnings (PE) of 9.20x and price to book value (PBV) of 1.49x in 2023.

Helgi Library

Helgi Library