By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka made a net profit of CZK 110 mil in the fourth quarter of 2020, up 164% when compared to the same perio...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka made a net profit of CZK 110 mil under revenues of CZK 85.6 mil in the fourth quarter of 2020, up 164% and ...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's net interest margin amounted to -0.207% in the fourth quarter of 2020, down from 0.671% when compare...

| Profit Statement | 2018 | 2019 | 2020 | |

| Net Interest Income | CZK mil | 440 | 412 | 269 |

| Net Fee Income | CZK mil | 30.0 | 22.0 | 19.0 |

| Other Income | CZK mil | -6.00 | 33.0 | 81.0 |

| Total Revenues | CZK mil | 464 | 467 | 369 |

| Staff Cost | CZK mil | 31.0 | 41.0 | 30.0 |

| Operating Profit | CZK mil | 184 | 145 | 98.0 |

| Provisions | CZK mil | 42.0 | -18.0 | -88.0 |

| Net Profit | CZK mil | 119 | 131 | 146 |

| Balance Sheet | 2018 | 2019 | 2020 | |

| Interbank Loans | CZK mil | 2,608 | 3,344 | 0 |

| Customer Loans | CZK mil | 32,983 | 37,630 | 38,658 |

| Investments | CZK mil | 1,101 | 1,104 | 0 |

| Total Assets | CZK mil | 37,199 | 42,616 | 39,552 |

| Shareholders' Equity | CZK mil | 2,269 | 2,352 | 2,462 |

| Interbank Borrowing | CZK mil | 1,041 | 680 | 4,000 |

| Customer Deposits | CZK mil | 17,048 | 23,734 | 22,740 |

| Issued Debt Securities | CZK mil | 16,638 | 15,438 | 10,018 |

| Ratios | 2018 | 2019 | 2020 | |

| ROE | % | 5.18 | 5.67 | 6.07 |

| ROA | % | 0.340 | 0.328 | 0.355 |

| Costs (As % Of Assets) | % | 0.801 | 0.807 | 0.660 |

| Costs (As % Of Income) | % | 60.3 | 69.0 | 73.4 |

| Capital Adequacy Ratio | % | 13.0 | 14.5 | 13.7 |

| Net Interest Margin | % | 1.26 | 1.03 | 0.655 |

| Loans (As % Of Deposits) | % | 193 | 159 | 170 |

| NPLs (As % Of Loans) | % | 1.85 | 1.38 | 1.26 |

| Provisions (As % Of NPLs) | % | 66.2 | 64.0 | 15.6 |

| Growth Rates | 2018 | 2019 | 2020 | |

| Total Revenue Growth | % | -2.36 | 0.647 | -21.0 |

| Operating Cost Growth | % | 32.3 | 15.0 | -15.8 |

| Operating Profit Growth | % | -30.2 | -21.2 | -32.4 |

| Net Profit Growth | % | -40.5 | 10.1 | 11.5 |

| Customer Loan Growth | % | 12.0 | 14.1 | 2.73 |

| Total Asset Growth | % | 13.7 | 14.6 | -7.19 |

| Customer Deposit Growth | % | 4.10 | 39.2 | -4.19 |

| Shareholders' Equity Growth | % | -2.32 | 3.66 | 4.68 |

| Employees | 44.0 | 45.0 | 17.0 | |

Get all company financials in excel:

| summary | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| income statement | |||||||||||||||||||

| Net Interest Income | CZK mil | ... | 449 | 508 | 446 | 436 | 440 | ||||||||||||

| Total Revenues | CZK mil | ... | 528 | 572 | 522 | 475 | 464 | ||||||||||||

| Operating Profit | CZK mil | ... | 314 | 348 | 283 | 264 | 184 | ||||||||||||

| Net Profit | CZK mil | ... | 219 | 247 | 190 | 200 | 119 | ||||||||||||

| balance sheet | |||||||||||||||||||

| Interbank Loans | CZK mil | 61.0 | 51.0 | 47.0 | 1,458 | 2,608 | |||||||||||||

| Customer Loans | CZK mil | 23,055 | 25,319 | 27,193 | 29,458 | 32,983 | |||||||||||||

| Investments | CZK mil | 1,641 | 1,284 | 1,560 | 1,306 | 1,101 | |||||||||||||

| Total Assets | CZK mil | 25,060 | 27,869 | 30,191 | 32,727 | 37,199 | |||||||||||||

| Shareholders' Equity | CZK mil | 1,636 | 1,896 | 2,076 | 2,323 | 2,269 | |||||||||||||

| Interbank Borrowing | CZK mil | 311 | 1,903 | 501 | 1,294 | 1,041 | |||||||||||||

| Customer Deposits | CZK mil | 15,407 | 15,121 | 15,967 | 16,376 | 17,048 | |||||||||||||

| Issued Debt Securities | CZK mil | 7,656 | 8,832 | 11,550 | 12,649 | 16,638 | |||||||||||||

| ratios | |||||||||||||||||||

| ROE | % | ... | 14.3 | 14.0 | 9.57 | 9.10 | 5.18 | ||||||||||||

| ROA | % | ... | 0.875 | 0.933 | 0.654 | 0.636 | 0.340 | ||||||||||||

| Costs (As % Of Assets) | % | ... | 0.855 | 0.846 | 0.823 | 0.673 | 0.801 | ||||||||||||

| Costs (As % Of Income) | % | ... | 40.5 | 39.2 | 45.8 | 44.5 | 60.3 | ||||||||||||

| Capital Adequacy Ratio | % | ... | 12.7 | 13.1 | 15.5 | 14.8 | 13.0 | ||||||||||||

| Net Interest Margin | % | ... | 1.79 | 1.92 | 1.54 | 1.39 | 1.26 | ||||||||||||

| Interest Income (As % Of Revenues) | % | ... | 85.0 | 88.8 | 85.4 | 91.7 | 94.8 | ||||||||||||

| Fee Income (As % Of Revenues) | % | ... | 10.6 | 9.62 | 8.62 | 8.50 | 6.47 | ||||||||||||

| Staff Cost (As % Of Total Cost) | % | ... | 36.0 | 41.5 | 7.95 | 14.3 | 11.1 | ||||||||||||

| Equity (As % Of Assets) | % | 6.53 | 6.80 | 6.88 | 7.10 | 6.10 | |||||||||||||

| Loans (As % Of Deposits) | % | 150 | 167 | 170 | 180 | 193 | |||||||||||||

| Loans (As % Assets) | % | 92.0 | 90.9 | 90.1 | 90.0 | 88.7 | |||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 4.62 | 3.50 | 3.77 | 2.46 | 1.85 | ||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 30.3 | 39.4 | 37.6 | 52.7 | 66.2 | ||||||||||

| valuation | |||||||||||||||||||

| Book Value Per Share Growth | % | ... | ... | 30.5 | 13.1 | -12.2 | -2.27 | 0.949 |

| income statement | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| income statement | |||||||||||||||||||

| Interest Income | CZK mil | ... | 908 | 841 | 760 | 727 | 817 | ||||||||||||

| Interest Cost | CZK mil | ... | 459 | 333 | 314 | 291 | 377 | ||||||||||||

| Net Interest Income | CZK mil | ... | 449 | 508 | 446 | 436 | 440 | ||||||||||||

| Net Fee Income | CZK mil | ... | 56.0 | 55.0 | 45.0 | 40.4 | 30.0 | ||||||||||||

| Fee Income | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||

| Fee Expense | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||

| Other Income | CZK mil | ... | 23.0 | 9.00 | 31.0 | -1.00 | -6.00 | ||||||||||||

| Total Revenues | CZK mil | ... | 528 | 572 | 522 | 475 | 464 | ||||||||||||

| Staff Cost | CZK mil | ... | 77.0 | 93.0 | 19.0 | 30.3 | 31.0 | ||||||||||||

| Depreciation | CZK mil | ... | 14.0 | 15.0 | 14.0 | 2.34 | 2.00 | ||||||||||||

| Other Cost | CZK mil | ... | 123 | 116 | 206 | 179 | 247 | ||||||||||||

| Operating Cost | CZK mil | ... | 214 | 224 | 239 | 212 | 280 | ||||||||||||

| Operating Profit | CZK mil | ... | 314 | 348 | 283 | 264 | 184 | ||||||||||||

| Provisions | CZK mil | ... | 44.0 | 40.0 | 47.0 | 16.0 | 42.0 | ||||||||||||

| Extra and Other Cost | CZK mil | ... | 0 | 0 | 0 | -0.411 | 0 | ||||||||||||

| Pre-Tax Profit | CZK mil | ... | 270 | 308 | 236 | 248 | 142 | ||||||||||||

| Tax | CZK mil | ... | 51.0 | 61.0 | 46.0 | 48.0 | 23.0 | ||||||||||||

| Minorities | CZK mil | ... | 0 | 0 | 0 | 0 | 0 | ||||||||||||

| Net Profit | CZK mil | ... | 219 | 247 | 190 | 200 | 119 | ||||||||||||

| Net Profit Avail. to Common | CZK mil | ... | 219 | 247 | 190 | 200 | 119 | ||||||||||||

| growth rates | |||||||||||||||||||

| Net Interest Income Growth | % | ... | ... | 30.5 | 13.1 | -12.2 | -2.27 | 0.949 | |||||||||||

| Net Fee Income Growth | % | ... | ... | -5.08 | -1.79 | -18.2 | -10.3 | -25.7 | |||||||||||

| Total Revenue Growth | % | ... | ... | 28.8 | 8.33 | -8.74 | -8.96 | -2.36 | |||||||||||

| Operating Cost Growth | % | ... | ... | 9.74 | 4.67 | 6.70 | -11.4 | 32.3 | |||||||||||

| Operating Profit Growth | % | ... | ... | 46.0 | 10.8 | -18.7 | -6.86 | -30.2 | |||||||||||

| Pre-Tax Profit Growth | % | ... | ... | 53.4 | 14.1 | -23.4 | 5.08 | -42.7 | |||||||||||

| Net Profit Growth | % | ... | ... | 61.0 | 12.8 | -23.1 | 5.34 | -40.5 | |||||||||||

| market share | |||||||||||||||||||

| Market Share in Revenues | % | ... | 0.314 | 0.328 | 0.290 | 0.265 | 0.244 | ||||||||||||

| Market Share in Net Profit | % | ... | 0.347 | 0.372 | 0.257 | 0.266 | 0.146 | ||||||||||||

| Market Share in Employees | % | ... | 0.087 | 0.080 | 0.098 | 0.103 | 0.105 | ||||||||||||

| Market Share in Branches | % | ... | 0.045 | 0.046 | 0.049 | 0.051 | 0.051 |

| balance sheet | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| balance sheet | |||||||||||||||||||

| Cash & Cash Equivalents | CZK mil | 260 | 1,163 | 1,357 | 343 | 315 | |||||||||||||

| Interbank Loans | CZK mil | 61.0 | 51.0 | 47.0 | 1,458 | 2,608 | |||||||||||||

| Customer Loans | CZK mil | 23,055 | 25,319 | 27,193 | 29,458 | 32,983 | |||||||||||||

| Retail Loans | CZK mil | 20,916 | 25,319 | 27,193 | 29,545 | 33,058 | |||||||||||||

| Mortgage Loans | CZK mil | 20,916 | 25,319 | 27,193 | 28,145 | 31,497 | |||||||||||||

| Consumer Loans | CZK mil | 0 | 0 | 0 | 1,400 | 1,561 | |||||||||||||

| Corporate Loans | CZK mil | 0 | 0 | 0 | 300 | 335 | |||||||||||||

| Investments | CZK mil | 1,641 | 1,284 | 1,560 | 1,306 | 1,101 | |||||||||||||

| Property and Equipment | CZK mil | 18.0 | 17.0 | 0 | 0 | 0 | |||||||||||||

| Intangible Assets | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 16.0 | 20.0 | 2.00 | 2.00 | 7.00 | ||

| Total Assets | CZK mil | 25,060 | 27,869 | 30,191 | 32,727 | 37,199 | |||||||||||||

| Shareholders' Equity | CZK mil | 1,636 | 1,896 | 2,076 | 2,323 | 2,269 | |||||||||||||

| Of Which Minority Interest | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||

| Liabilities | CZK mil | 23,424 | 25,973 | 28,115 | 30,404 | 34,930 | |||||||||||||

| Interbank Borrowing | CZK mil | 311 | 1,903 | 501 | 1,294 | 1,041 | |||||||||||||

| Customer Deposits | CZK mil | 15,407 | 15,121 | 15,967 | 16,376 | 17,048 | |||||||||||||

| Retail Deposits | CZK mil | 15,407 | 15,121 | 15,967 | 16,376 | 17,048 | |||||||||||||

| Corporate Deposits | CZK mil | 0 | 0 | 0 | 0 | 0 | |||||||||||||

| Sight Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||

| Term Deposits | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||

| Issued Debt Securities | CZK mil | 7,656 | 8,832 | 11,550 | 12,649 | 16,638 | |||||||||||||

| Other Liabilities | CZK mil | 50.0 | 117 | 97.0 | 84.8 | 203 | |||||||||||||

| asset quality | |||||||||||||||||||

| Non-Performing Loans | CZK mil | ... | ... | ... | 1,081 | 898 | 1,041 | 734 | 619 | ||||||||||

| Gross Loans | CZK mil | 23,383 | 25,673 | 27,584 | 29,845 | 33,393 | |||||||||||||

| Risk-Weighted Assets | CZK mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 11,194 | 12,605 | 12,310 | 13,567 | 15,848 | ||

| Total Provisions | CZK mil | ... | ... | ... | 328 | 354 | 391 | 387 | 410 | ||||||||||

| growth rates | |||||||||||||||||||

| Customer Loan Growth | % | ... | 6.02 | 9.82 | 7.40 | 8.33 | 12.0 | ||||||||||||

| Retail Loan Growth | % | ... | ... | 6.52 | 21.1 | 7.40 | 8.65 | 11.9 | |||||||||||

| Mortgage Loan Growth | % | ... | ... | 6.52 | 21.1 | 7.40 | 3.50 | 11.9 | |||||||||||

| Consumer Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 11.5 | ||

| Corporate Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 11.7 | ||

| Total Asset Growth | % | ... | 0.360 | 11.2 | 8.33 | 8.40 | 13.7 | ||||||||||||

| Shareholders' Equity Growth | % | ... | 14.3 | 15.9 | 9.49 | 11.9 | -2.32 | ||||||||||||

| Customer Deposit Growth | % | ... | 0.699 | -1.86 | 5.59 | 2.56 | 4.10 | ||||||||||||

| Retail Deposit Growth | % | ... | 0.699 | -1.86 | 5.59 | 2.56 | 4.10 | ||||||||||||

| market share | |||||||||||||||||||

| Market Share in Customer Loans | % | 0.875 | 0.910 | 0.922 | 0.955 | 0.998 | |||||||||||||

| Market Share in Corporate Loans | % | 0 | 0 | 0 | 0.029 | 0.031 | |||||||||||||

| Market Share in Retail Loans | % | 1.70 | 1.92 | 1.92 | 1.93 | 2.01 | |||||||||||||

| Market Share in Consumer Loans | % | 0 | 0 | 0 | 0.367 | 0.390 | |||||||||||||

| Market Share in Mortgage Loans | % | 2.32 | 2.61 | 2.58 | 2.45 | 2.53 | |||||||||||||

| Market Share in Total Assets | % | 0.472 | 0.510 | 0.507 | 0.467 | 0.511 | |||||||||||||

| Market Share in Customer Deposits | % | 0.449 | 0.429 | 0.424 | 0.393 | 0.383 | |||||||||||||

| Market Share in Retail Deposits | % | 0.801 | 0.743 | 0.723 | 0.691 | 0.666 | |||||||||||||

| Market Share in Corporate Deposits | % | 0 | 0 | 0 | 0 | 0 |

| ratios | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| ROE | % | ... | 14.3 | 14.0 | 9.57 | 9.10 | 5.18 | ||||||||||||

| ROTE | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 14.1 | 9.62 | 9.11 | 5.19 | ||

| ROE (@ 15% of RWA) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 13.8 | 10.2 | 10.3 | 5.39 | ||

| ROA | % | ... | 0.875 | 0.933 | 0.654 | 0.636 | 0.340 | ||||||||||||

| Return on Loans | % | ... | 0.978 | 1.02 | 0.724 | 0.707 | 0.381 | ||||||||||||

| Operating Profit (As % of RWA) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2.92 | 2.27 | 2.04 | 1.25 | ||

| Costs (As % Of Assets) | % | ... | 0.855 | 0.846 | 0.823 | 0.673 | 0.801 | ||||||||||||

| Costs (As % Of Income) | % | ... | 40.5 | 39.2 | 45.8 | 44.5 | 60.3 | ||||||||||||

| Costs (As % Of Loans) | % | ... | 0.955 | 0.926 | 0.910 | 0.747 | 0.897 | ||||||||||||

| Costs (As % Of Loans & Deposits) | % | ... | 0.567 | 0.568 | 0.572 | 0.476 | 0.584 | ||||||||||||

| Capital Adequacy Ratio | % | ... | 12.7 | 13.1 | 15.5 | 14.8 | 13.0 | ||||||||||||

| Tier 1 Ratio | % | ... | 12.7 | 13.1 | 15.5 | 14.8 | 13.0 | ||||||||||||

| Net Interest Margin | % | ... | 1.79 | 1.92 | 1.54 | 1.39 | 1.26 | ||||||||||||

| Interest Spread | % | ... | 1.68 | 1.83 | 1.46 | 1.32 | 1.18 | ||||||||||||

| Asset Yield | % | ... | 3.63 | 3.18 | 2.62 | 2.31 | 2.34 | ||||||||||||

| Revenues (As % of RWA) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4.81 | 4.19 | 3.67 | 3.15 | ||

| Cost Of Liabilities | % | ... | 1.95 | 1.35 | 1.16 | 0.996 | 1.15 | ||||||||||||

| Interest Income (As % Of Revenues) | % | ... | 85.0 | 88.8 | 85.4 | 91.7 | 94.8 | ||||||||||||

| Fee Income (As % Of Revenues) | % | ... | 10.6 | 9.62 | 8.62 | 8.50 | 6.47 | ||||||||||||

| Other Income (As % Of Revenues) | % | ... | 4.36 | 1.57 | 5.94 | -0.210 | -1.29 | ||||||||||||

| Staff Cost (As % Of Total Cost) | % | ... | 36.0 | 41.5 | 7.95 | 14.3 | 11.1 | ||||||||||||

| Equity (As % Of Assets) | % | 6.53 | 6.80 | 6.88 | 7.10 | 6.10 | |||||||||||||

| Equity (As % Of Loans) | % | 7.10 | 7.49 | 7.63 | 7.89 | 6.88 | |||||||||||||

| Loans (As % Of Deposits) | % | 150 | 167 | 170 | 180 | 193 | |||||||||||||

| Loans (As % Assets) | % | 92.0 | 90.9 | 90.1 | 90.0 | 88.7 | |||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 4.62 | 3.50 | 3.77 | 2.46 | 1.85 | ||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 30.3 | 39.4 | 37.6 | 52.7 | 66.2 | ||||||||||

| Provisions (As % Of Loans) | % | ... | ... | ... | 1.42 | 1.40 | 1.44 | 1.31 | 1.24 | ||||||||||

| Cost of Provisions (As % Of Loans) | % | ... | 0.196 | 0.165 | 0.179 | 0.056 | 0.135 |

| other data | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Branches | ... | 1.00 | 1.00 | 1.00 | 1.00 | 1.00 | |||||||||||||

| ATMs | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ||

| ATMs (As % of Bank Branches) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | |

| Employees | ... | 35.0 | 33.0 | 40.0 | 43.0 | 44.0 | |||||||||||||

| Employees Per Bank Branch | ... | 35.0 | 33.0 | 40.0 | 43.0 | 44.0 | |||||||||||||

| Cost Per Employee | USD per month | ... | 8,578 | 9,833 | 1,569 | 2,503 | 2,684 | ||||||||||||

| Cost Per Employee (Local Currency) | CZK per month | ... | 183,333 | 234,705 | 39,583 | 58,729 | 58,712 |

| customer breakdown | Unit | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Customers | mil | ... | ... | ... | ... | ... | 0.017 | 0.020 | 0.020 | 0.020 | 0.022 | ||||||||

| Number of Mortgages | mil | ... | ... | ... | ... | ... | 0.017 | 0.020 | 0.020 | 0.020 | 0.022 | ||||||||

| Average Size of Mortgage Loan | CZK | ... | ... | ... | ... | ... | 1,266,000 | 1,282,000 | 1,352,000 | 1,393,000 | 1,451,000 | ||||||||

| Mortgages (As % of Total Clients) | % | ... | ... | ... | ... | ... | 100 | 100 | 100 | 100 | 100 | ||||||||

| Revenue per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | 31,959 | 28,963 | 25,953 | 23,522 | 21,376 | ||||||||

| Net Profit per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | 13,256 | 12,507 | 9,447 | 9,906 | 5,482 | ||||||||

| Loan per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | 1,395,470 | 1,282,000 | 1,352,000 | 1,458,000 | 1,519,460 | ||||||||

| Deposit per Customer (Local Currency) | CZK | ... | ... | ... | ... | ... | 932,552 | 765,635 | 793,858 | 810,518 | 785,365 | ||||||||

| Revenue per Customer | USD | ... | ... | ... | ... | ... | 1,495 | 1,213 | 1,029 | 1,002 | 977 | ||||||||

| Net Profit per Customer | USD | ... | ... | ... | ... | ... | 620 | 524 | 374 | 422 | 251 | ||||||||

| Loan per Customer | USD | ... | ... | ... | ... | ... | 60,900 | 51,644 | 52,732 | 68,480 | 67,634 | ||||||||

| Deposit per Customer | USD | ... | ... | ... | ... | ... | 40,697 | 30,843 | 30,963 | 38,069 | 34,958 |

Get all company financials in excel:

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's consumer loans reached CZK 2,721 mil in 2020-12-31, down 0% compared to the previous year. Czech banking sector provided consumer loans of CZK 423 bil in 2020-12-31, up 0.348% when compared to the last year. Wustenrot Hypotecni...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka employed 17.0 persons in 2020-12-31, down 22.7% when compared to the previous year. Historically, the bank's workforce hit an all time high of 43.0 persons in 2013-03-31 and an all time low of 17.0 in 2020-12-31. Average cost reached USD ...

By Helgi Library - November 22, 2023

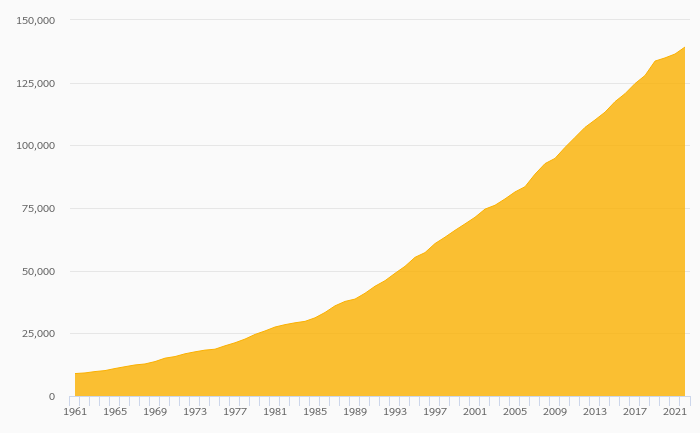

Wustenrot Hypotecni banka's mortgage loans reached CZK 35,789 mil in 4Q2020, down 8.38% compared to the previous year. Czech banking sector provided mortgage loans of CZK 1,436 in 4Q2020, up 2.30% when compared to the last year. Wustenrot Hypotecni banka ...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's non-performing loans reached 1.26% of total loans at the end of 2020-12-31, down from 1.38% compared to the previous year. Historically, the NPL ratio hit an all time high of 4.77% in 2018-09-30 and an all time low of 0.840% in 2008-03...

By Helgi Library - March 7, 2022

Wustenrot Hypotecni banka's customer deposits reached CZK 22,740 mil in 2020-12-31, down 21.3% compared to the previous year. Czech banking sector accepted customer deposits of CZK 5,162 bil in 2020-12-31, down 6.99% when compared to the last year. Wusten...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's customer loans reached CZK 38,658 mil in 2020-12-31, down 2.37% compared to the previous year. Czech banking sector provided customer loans of CZK 3,596 bil in 2020-12-31, down 0.651% when compared to the last year. Wustenrot H...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's loans reached CZK 38,734 mil in the fourth quarter of 2020, down from CZK 46,285 mil when compared to the previous quarter and up from CZK 37,966 mil when compared to the same period of last year. Historically, the bank’s...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's retail deposits reached CZK 22,740 mil in 2020-12-31, down 20.1% compared to the previous year. Czech banking sector accepted retail deposits of CZK 3,057 bil in 2020-12-31, up 3.25% when compared to the last year. Wustenrot Hy...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's retail loans reached CZK 38,510 mil in the fourth quarter of 2020, down 1.41% compared to the previous year. Czech banking sector provided retail loans of CZK 1,859 bil in 4Q2020, up 1.85% when compared to the last year. Wusten...

By Helgi Library - September 26, 2021

Wustenrot Hypotecni banka's cost to income ratio reached 57.1% in the fourth quarter of 2020, up from 20.0% when compared to the previous quarter. Historically, the bank’s costs reached an all time high of 185% of income in 4Q2009 and an all time low of 20.0...

Wüstenrot Hypoteční banka is a Czech Republic-based mortgage bank. Although Wüstenrot has been growing more than twice as fast as the overall market over the last five years, its late arrival in the mortgage business a decade ago means the bank still occupies only 2.5% of the Czech mortgage lending market. Partly because of its small size and its conservative approach, the bank is relatively little profitable with ROE in single-digit territory in the last five years. Size matters and the lack of economies of scale is also reflected in Wüstenrot’s low cost efficiency. In 2012, the bank’s operating costs accounted for over 50% of bank revenues, three times as much as the other pure mortgage bank on the Czech market - Hypoteční Banka

Wustenrot Hypotecni banka has been growing its revenues and asset by 4.58% and 12.7% a year on average in the last 10 years. Its loans and deposits have grown by 13.1% and 26.1% a year during that time and loans to deposits ratio reached 170% at the end of 2020. The company achieved an average return on equity of 8.37% in the last decade with net profit growing 6.88% a year on average. In terms of operating efficiency, its cost to income ratio reached 73.4% in 2020, compared to 52.1% average in the last decade.

Equity represented 6.22% of total assets or 6.37% of loans at the end of 2020. Wustenrot Hypotecni banka's non-performing loans were 1.26% of total loans while provisions covered some 15.6% of NPLs at the end of 2020.

Helgi Library

Helgi Library