By Helgi Library - June 25, 2018

DenizBank made a net profit of TRY 1,902 mil under revenues of TRY 7,651 mil in 2017, up 35.9% and 16.7% respectively compared to the...

By Helgi Library - December 12, 2019

DenizBank's customer loans reached TRY 110,381 mil in 2017, up 21.1% compared to the previous year. Turkish banking sector prov...

By Helgi Library - December 12, 2019

DenizBank's customer deposits reached TRY 111,410 mil in 2017, up 20.8% compared to the previous year. Turkish banking sector a...

| Profit Statement | 2015 | 2016 | 2017 | |

| Net Interest Income | TRY mil | 4,084 | 5,102 | 6,281 |

| Net Fee Income | TRY mil | 1,084 | 1,254 | 1,605 |

| Other Income | TRY mil | 614 | 199 | -235 |

| Total Revenues | TRY mil | 5,782 | 6,555 | 7,651 |

| Staff Cost | TRY mil | 1,247 | 1,359 | 1,458 |

| Operating Profit | TRY mil | 2,504 | 3,628 | 4,436 |

| Provisions | TRY mil | 1,361 | 1,803 | 1,944 |

| Net Profit | TRY mil | 858 | 1,400 | 1,902 |

| Balance Sheet | 2015 | 2016 | 2017 | |

| Interbank Loans | TRY mil | 7,437 | 5,573 | 10,658 |

| Customer Loans | TRY mil | 74,687 | 91,151 | 110,381 |

| Total Assets | TRY mil | 112,886 | 135,554 | 160,423 |

| Shareholders' Equity | TRY mil | 8,294 | 10,590 | 12,853 |

| Interbank Borrowing | TRY mil | 586 | 5,398 | 4,007 |

| Customer Deposits | TRY mil | 72,659 | 92,196 | 111,410 |

| Issued Debt Securities | TRY mil | 19,828 | 20,233 | 23,615 |

| Ratios | 2015 | 2016 | 2017 | |

| ROE | % | 11.1 | 14.8 | 16.2 |

| ROA | % | 0.828 | 1.13 | 1.29 |

| Costs (As % Of Assets) | % | 3.16 | 2.36 | 2.17 |

| Costs (As % Of Income) | % | 56.7 | 44.6 | 42.0 |

| Capital Adequacy Ratio | % | 12.9 | 14.2 | 15.3 |

| Net Interest Margin | % | 3.94 | 4.11 | 4.24 |

| Loans (As % Of Deposits) | % | 103 | 98.9 | 99.1 |

| NPLs (As % Of Loans) | % | 4.08 | 3.89 | 3.55 |

| Provisions (As % Of NPLs) | % | 95.2 | 72.5 | 77.7 |

| Valuation | 2015 | 2016 | 2017 | |

| Price/Earnings (P/E) | 6.50 | 11.3 | 6.40 | |

| Price/Book Value (P/BV) | 0.672 | 1.49 | 0.947 | |

| Dividend Yield | % | 0 | 0 | 0 |

| Earnings Per Share (EPS) | TRY | 0.473 | 0.422 | 0.574 |

| Book Value Per Share | TRY | 4.57 | 3.19 | 3.88 |

| Dividend Per Share | 0 | 0 | 0 | |

Get all company financials in excel:

| summary | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | ||||||||||||||||||||||

| Net Interest Income | TRY mil | ... | ... | ... | 1,880 | 2,470 | 3,010 | 3,627 | 4,084 | |||||||||||||

| Total Revenues | TRY mil | ... | ... | ... | 2,706 | 4,029 | 4,374 | 5,202 | 5,782 | |||||||||||||

| Operating Profit | TRY mil | ... | ... | ... | 1,369 | 1,683 | 2,296 | 2,167 | 2,504 | |||||||||||||

| Net Profit | TRY mil | ... | ... | ... | 1,062 | 717 | 1,011 | 937 | 858 | |||||||||||||

| balance sheet | ||||||||||||||||||||||

| Interbank Loans | TRY mil | ... | ... | ... | 2,164 | 2,128 | 3,867 | 5,622 | 7,437 | |||||||||||||

| Customer Loans | TRY mil | 28,066 | 35,316 | 55,294 | 60,838 | 74,687 | ||||||||||||||||

| Debt Securities | TRY mil | ... | ... | ... | 9,126 | 12,379 | 13,623 | 12,440 | 14,523 | |||||||||||||

| Total Assets | TRY mil | 44,756 | 56,495 | 79,667 | 94,403 | 112,886 | ||||||||||||||||

| Shareholders' Equity | TRY mil | 4,641 | 5,665 | 6,088 | 7,161 | 8,294 | ||||||||||||||||

| Interbank Borrowing | TRY mil | ... | ... | ... | 45.7 | 40.9 | 690 | 489 | 586 | |||||||||||||

| Customer Deposits | TRY mil | 26,876 | 36,552 | 49,835 | 64,119 | 72,659 | ||||||||||||||||

| Issued Debt Securities | TRY mil | ... | ... | ... | 10,600 | 11,248 | 17,223 | 16,037 | 19,828 | |||||||||||||

| ratios | ||||||||||||||||||||||

| ROE | % | ... | ... | ... | 25.6 | 13.9 | 17.2 | 14.2 | 11.1 | |||||||||||||

| ROA | % | ... | ... | ... | 2.70 | 1.42 | 1.49 | 1.08 | 0.828 | |||||||||||||

| Costs (As % Of Assets) | % | ... | ... | ... | 3.40 | 4.63 | 3.05 | 3.49 | 3.16 | |||||||||||||

| Costs (As % Of Income) | % | ... | ... | ... | 49.4 | 58.2 | 47.5 | 58.4 | 56.7 | |||||||||||||

| Capital Adequacy Ratio | % | ... | ... | ... | 14.7 | 13.1 | 12.1 | 12.9 | 12.9 | |||||||||||||

| Net Interest Margin | % | ... | ... | ... | 4.78 | 4.88 | 4.42 | 4.17 | 3.94 | |||||||||||||

| Interest Income (As % Of Revenues) | % | ... | ... | ... | 69.5 | 61.3 | 68.8 | 69.7 | 70.6 | |||||||||||||

| Fee Income (As % Of Revenues) | % | ... | ... | ... | 15.7 | 12.0 | 14.2 | 19.0 | 18.7 | |||||||||||||

| Staff Cost (As % Of Total Cost) | % | ... | ... | ... | 50.1 | 30.9 | 44.7 | 37.5 | 38.1 | |||||||||||||

| Equity (As % Of Assets) | % | 10.4 | 10.0 | 7.64 | 7.59 | 7.35 | ||||||||||||||||

| Loans (As % Of Deposits) | % | 104 | 96.6 | 111 | 94.9 | 103 | ||||||||||||||||

| Loans (As % Assets) | % | 62.7 | 62.5 | 69.4 | 64.4 | 66.2 | ||||||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 3.12 | 3.85 | 2.85 | 3.07 | 4.08 | |||||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 68.1 | 59.5 | 72.8 | 188 | 95.2 | |||||||||||||

| valuation | ||||||||||||||||||||||

| Market Capitalisation (End Of Period) | USD mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4,674 | 4,516 | 2,545 | 2,354 | 1,916 | |||||

| Number Of Shares (Average) | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 716 | 716 | 716 | 716 | 1,816 | |||||

| Share Price (End Of Period) | TRY | ... | ... | ... | ... | ... | ... | ... | ... | ... | 12.3 | 11.3 | 7.64 | 7.68 | 3.07 | |||||||

| Earnings Per Share (EPS) | TRY | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.48 | 1.00 | 1.41 | 1.31 | 0.473 | |||||

| Book Value Per Share | TRY | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 6.48 | 7.91 | 8.50 | 10.0 | 4.57 | |||||

| Dividend Per Share | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0 | 0 | 0 | 0 | 0 | ||||

| Price/Earnings (P/E) | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 8.30 | 11.2 | 5.41 | 5.87 | 6.50 | ||||||

| Price/Book Value (P/BV) | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.90 | 1.42 | 0.899 | 0.768 | 0.672 | ||||||

| Dividend Yield | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0 | 0 | 0 | 0 | 0 | |||

| Earnings Per Share Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 72.8 | -32.4 | 40.9 | -7.29 | -63.9 | ||||

| Book Value Per Share Growth | % | ... | ... | ... | ... | 26.8 | 22.0 | 7.48 | 17.6 | -54.3 |

| income statement | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | ||||||||||||||||||||||

| Interest Income | TRY mil | ... | ... | ... | 3,536 | 4,806 | 5,454 | 7,080 | 8,395 | |||||||||||||

| Interest Cost | TRY mil | ... | ... | ... | 1,655 | 2,337 | 2,443 | 3,453 | 4,311 | |||||||||||||

| Net Interest Income | TRY mil | ... | ... | ... | 1,880 | 2,470 | 3,010 | 3,627 | 4,084 | |||||||||||||

| Net Fee Income | TRY mil | ... | ... | ... | 425 | 482 | 622 | 989 | 1,084 | |||||||||||||

| Other Income | TRY mil | ... | ... | ... | 400 | 1,077 | 742 | 587 | 614 | |||||||||||||

| Total Revenues | TRY mil | ... | ... | ... | 2,706 | 4,029 | 4,374 | 5,202 | 5,782 | |||||||||||||

| Staff Cost | TRY mil | ... | ... | ... | 670 | 725 | 928 | 1,139 | 1,247 | |||||||||||||

| Depreciation | TRY mil | ... | ... | ... | 101 | 124 | 149 | 174 | 199 | |||||||||||||

| Other Cost | TRY mil | ... | ... | ... | 565 | 1,498 | 1,000 | 1,722 | 1,831 | |||||||||||||

| Operating Cost | TRY mil | ... | ... | ... | 1,336 | 2,346 | 2,078 | 3,035 | 3,278 | |||||||||||||

| Operating Profit | TRY mil | ... | ... | ... | 1,369 | 1,683 | 2,296 | 2,167 | 2,504 | |||||||||||||

| Provisions | TRY mil | ... | ... | ... | 453 | 728 | 1,027 | 952 | 1,361 | |||||||||||||

| Extra and Other Cost | TRY mil | ... | ... | ... | 0 | 0 | 0 | 0 | 0 | |||||||||||||

| Pre-Tax Profit | TRY mil | ... | ... | ... | 917 | 956 | 1,269 | 1,215 | 1,143 | |||||||||||||

| Tax | TRY mil | ... | ... | ... | 200 | 236 | 257 | 276 | 284 | |||||||||||||

| Minorities | TRY mil | ... | ... | ... | -0.737 | 2.25 | -0.145 | 1.14 | 0.892 | |||||||||||||

| Net Profit | TRY mil | ... | ... | ... | 1,062 | 717 | 1,011 | 937 | 858 | |||||||||||||

| Dividends | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0 | 0 | 0 | 0 | 0 | |||

| growth rates | ||||||||||||||||||||||

| Net Interest Income Growth | % | ... | ... | ... | ... | 5.83 | 31.4 | 21.9 | 20.5 | 12.6 | ||||||||||||

| Net Fee Income Growth | % | ... | ... | ... | ... | 29.3 | 13.4 | 28.9 | 59.0 | 9.62 | ||||||||||||

| Total Revenue Growth | % | ... | ... | ... | ... | 16.8 | 48.9 | 8.54 | 18.9 | 11.2 | ||||||||||||

| Operating Cost Growth | % | ... | ... | ... | ... | 26.2 | 75.6 | -11.4 | 46.1 | 7.98 | ||||||||||||

| Operating Profit Growth | % | ... | ... | ... | ... | 8.91 | 22.9 | 36.4 | -5.64 | 15.6 | ||||||||||||

| Pre-Tax Profit Growth | % | ... | ... | ... | ... | 22.1 | 4.22 | 32.7 | -4.24 | -5.91 | ||||||||||||

| Net Profit Growth | % | ... | ... | ... | ... | 72.8 | -32.4 | 40.9 | -7.29 | -8.43 | ||||||||||||

| market share | ||||||||||||||||||||||

| Market Share in Revenues | % | ... | ... | ... | 4.61 | 5.54 | 5.42 | 5.85 | 5.83 | ... | ||||||||||||

| Market Share in Net Profit | % | ... | ... | ... | ... | ... | 5.57 | 3.17 | 4.28 | 3.83 | 3.35 | ... | ||||||||||

| Market Share in Employees | % | 5.97 | 6.24 | 7.30 | 7.46 | 7.38 | ||||||||||||||||

| Market Share in Bank Cards | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.73 | 1.91 | 1.93 | ||

| Market Share in Branches | % | 5.98 | 5.96 | 6.47 | 6.75 | 6.57 |

| balance sheet | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| balance sheet | ||||||||||||||||||||||

| Cash | TRY mil | ... | ... | ... | 4,156 | 5,250 | 8,815 | 9,458 | 10,823 | |||||||||||||

| Interbank Loans | TRY mil | ... | ... | ... | 2,164 | 2,128 | 3,867 | 5,622 | 7,437 | |||||||||||||

| Customer Loans | TRY mil | 28,066 | 35,316 | 55,294 | 60,838 | 74,687 | ||||||||||||||||

| Retail Loans | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | 8,648 | 10,065 | 14,349 | 11,904 | 13,230 | |||||||

| Mortgage Loans | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4,774 | 5,099 | ||

| Consumer Loans | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 6,174 | 7,150 | ||

| Corporate Loans | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | 19,418 | 25,251 | 40,945 | 48,934 | 61,457 | |||||||

| Debt Securities | TRY mil | ... | ... | ... | 9,126 | 12,379 | 13,623 | 12,440 | 14,523 | |||||||||||||

| Fixed Assets | TRY mil | ... | ... | ... | 416 | 456 | 573 | 662 | 726 | |||||||||||||

| Total Assets | TRY mil | 44,756 | 56,495 | 79,667 | 94,403 | 112,886 | ||||||||||||||||

| Shareholders' Equity | TRY mil | 4,641 | 5,665 | 6,088 | 7,161 | 8,294 | ||||||||||||||||

| Of Which Minority Interest | TRY mil | ... | ... | ... | 13.5 | 15.8 | 37.3 | 6.31 | 7.20 | |||||||||||||

| Liabilities | TRY mil | 40,115 | 50,830 | 73,578 | 87,242 | 104,592 | ||||||||||||||||

| Interbank Borrowing | TRY mil | ... | ... | ... | 45.7 | 40.9 | 690 | 489 | 586 | |||||||||||||

| Customer Deposits | TRY mil | 26,876 | 36,552 | 49,835 | 64,119 | 72,659 | ||||||||||||||||

| Retail Deposits | TRY mil | ... | ... | ... | ... | ... | 8,319 | 10,046 | 13,758 | 33,041 | 40,642 | |||||||||||

| Corporate Deposits | TRY mil | ... | ... | ... | ... | ... | 18,556 | 26,505 | 36,077 | 31,078 | 32,017 | |||||||||||

| Sight Deposits | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 10,744 | 13,657 | 15,710 | ||

| Term Deposits | TRY mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 39,091 | 50,462 | 56,949 | ||

| Issued Debt Securities | TRY mil | ... | ... | ... | 10,600 | 11,248 | 17,223 | 16,037 | 19,828 | |||||||||||||

| Other Liabilities | TRY mil | ... | ... | ... | 2,593 | 2,990 | 5,831 | 6,596 | 11,519 | |||||||||||||

| asset quality | ||||||||||||||||||||||

| Non-Performing Loans | TRY mil | ... | ... | ... | 894 | 1,392 | 1,610 | 1,982 | 3,169 | |||||||||||||

| Gross Loans | TRY mil | ... | ... | ... | 28,674 | 36,144 | 56,466 | 64,564 | 77,705 | |||||||||||||

| Total Provisions | TRY mil | ... | ... | ... | 609 | 828 | 1,172 | 3,726 | 3,018 | |||||||||||||

| growth rates | ||||||||||||||||||||||

| Customer Loan Growth | % | ... | 73.6 | 25.8 | 56.6 | 10.0 | 22.8 | |||||||||||||||

| Retail Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 41.0 | 16.4 | 42.6 | -17.0 | 11.1 | ||||||

| Mortgage Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 6.81 | ||

| Consumer Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 15.8 | ||

| Corporate Loan Growth | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 93.6 | 30.0 | 62.2 | 19.5 | 25.6 | ||||||

| Total Asset Growth | % | ... | 32.2 | 26.2 | 41.0 | 18.5 | 19.6 | |||||||||||||||

| Shareholders' Equity Growth | % | ... | 26.8 | 22.0 | 7.48 | 17.6 | 15.8 | |||||||||||||||

| Customer Deposit Growth | % | ... | 34.2 | 36.0 | 36.3 | 28.7 | 13.3 | |||||||||||||||

| Retail Deposit Growth | % | ... | ... | ... | ... | ... | ... | 27.9 | 20.8 | 36.9 | 140 | 23.0 | ||||||||||

| Corporate Deposit Growth | % | ... | ... | ... | ... | ... | ... | 37.2 | 42.8 | 36.1 | -13.9 | 3.02 | ||||||||||

| market share | ||||||||||||||||||||||

| Market Share in Customer Loans | % | 4.42 | 4.82 | 5.71 | 5.30 | 5.41 | ||||||||||||||||

| Market Share in Corporate Loans | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | 4.77 | 5.48 | 6.65 | 6.33 | 6.20 | |||||||

| Market Share in Retail Loans | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 2.47 | 2.90 | ||

| Market Share in Consumer Loans | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | 3.79 | 3.71 | 4.06 | 3.17 | 3.39 | |||||||

| Market Share in Mortgage Loans | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 3.81 | 3.55 | ||

| Market Share in Total Assets | % | 3.86 | 4.35 | 4.87 | 5.00 | 5.05 | ||||||||||||||||

| Market Share in Customer Deposits | % | 4.10 | 5.04 | 5.57 | 6.43 | 6.20 | ||||||||||||||||

| Market Share in Retail Deposits | % | ... | ... | ... | ... | ... | ... | 2.13 | 2.33 | 2.70 | 5.71 | 5.88 | ||||||||||

| Market Share in Corporate Deposits | % | ... | ... | ... | ... | ... | ... | 9.23 | 11.9 | 12.2 | 9.64 | 8.53 |

| ratios | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| ratios | ||||||||||||||||||||||

| ROE | % | ... | ... | ... | 25.6 | 13.9 | 17.2 | 14.2 | 11.1 | |||||||||||||

| ROA | % | ... | ... | ... | 2.70 | 1.42 | 1.49 | 1.08 | 0.828 | |||||||||||||

| Costs (As % Of Assets) | % | ... | ... | ... | 3.40 | 4.63 | 3.05 | 3.49 | 3.16 | |||||||||||||

| Costs (As % Of Income) | % | ... | ... | ... | 49.4 | 58.2 | 47.5 | 58.4 | 56.7 | |||||||||||||

| Capital Adequacy Ratio | % | ... | ... | ... | 14.7 | 13.1 | 12.1 | 12.9 | 12.9 | |||||||||||||

| Net Interest Margin | % | ... | ... | ... | 4.78 | 4.88 | 4.42 | 4.17 | 3.94 | |||||||||||||

| Interest Spread | % | ... | ... | ... | 4.29 | 4.36 | 4.08 | 3.84 | 3.61 | |||||||||||||

| Asset Yield | % | ... | ... | ... | 9.00 | 9.49 | 8.01 | 8.13 | 8.10 | |||||||||||||

| Cost Of Liabilities | % | ... | ... | ... | 4.71 | 5.14 | 3.93 | 4.29 | 4.49 | |||||||||||||

| Payout Ratio | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 0 | 0 | 0 | 0 | 0 | |||

| Interest Income (As % Of Revenues) | % | ... | ... | ... | 69.5 | 61.3 | 68.8 | 69.7 | 70.6 | |||||||||||||

| Fee Income (As % Of Revenues) | % | ... | ... | ... | 15.7 | 12.0 | 14.2 | 19.0 | 18.7 | |||||||||||||

| Other Income (As % Of Revenues) | % | ... | ... | ... | 14.8 | 26.7 | 17.0 | 11.3 | 10.6 | |||||||||||||

| Cost Per Employee | USD per month | ... | ... | ... | 3,070 | 2,889 | 2,815 | 2,825 | 2,668 | |||||||||||||

| Cost Per Employee (Local Currency) | TRY per month | ... | ... | ... | 5,158 | 5,200 | 5,367 | 6,337 | 6,998 | |||||||||||||

| Staff Cost (As % Of Total Cost) | % | ... | ... | ... | 50.1 | 30.9 | 44.7 | 37.5 | 38.1 | |||||||||||||

| Equity (As % Of Assets) | % | 10.4 | 10.0 | 7.64 | 7.59 | 7.35 | ||||||||||||||||

| Loans (As % Of Deposits) | % | 104 | 96.6 | 111 | 94.9 | 103 | ||||||||||||||||

| Loans (As % Assets) | % | 62.7 | 62.5 | 69.4 | 64.4 | 66.2 | ||||||||||||||||

| NPLs (As % Of Loans) | % | ... | ... | ... | 3.12 | 3.85 | 2.85 | 3.07 | 4.08 | |||||||||||||

| Provisions (As % Of NPLs) | % | ... | ... | ... | 68.1 | 59.5 | 72.8 | 188 | 95.2 | |||||||||||||

| Provisions (As % Of Loans) | % | ... | ... | ... | 2.17 | 2.34 | 2.12 | 6.13 | 4.04 | |||||||||||||

| Cost of Provisions (As % Of Loans) | % | ... | ... | ... | 2.05 | 2.30 | 2.27 | 1.64 | 2.01 |

| other data | Unit | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| other data | ||||||||||||||||||||||

| Branches | 588 | 610 | 713 | 758 | 735 | |||||||||||||||||

| Employees | 10,826 | 11,618 | 14,413 | 14,979 | 14,853 | |||||||||||||||||

| ATMs | ... | ... | ... | ... | ... | ... | ... | ... | 2,370 | 3,180 | 3,749 | 3,989 | 4,355 | |||||||||

| Clients | mil | ... | ... | ... | ... | ... | ... | ... | ... | ... | 1.60 | ... | ... | ... | 9.10 | ... | ... | |||||

| Payment Cards | '000 | ... | ... | ... | ... | ... | ... | 1,967 | 2,192 | 2,718 | 3,099 | 3,284 | ||||||||||

| Sight (As % Of Customer Deposits) | % | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | 21.6 | 21.3 | 21.6 |

Get all company financials in excel:

By Helgi Library - September 23, 2018

DenizBank has issued total of 3,999 '000 payment cards at the end of 2017, up 11.9% compared to the previous year. Turkish banking sector banking sector issued total of 194,047 thous. of bank cards in 2017, up 10.4% when compared to the last year....

By Helgi Library - June 25, 2018

DenizBank's retail deposits reached TRY 65,719 mil in 2017, up 29.6% compared to the previous year. Turkish banking sector accepted retail deposits of TRY 945 bil in 2017, up 17.2% when compared to the last year. DenizBank accounted for 6.95% of all retai...

By Helgi Library - June 25, 2018

DenizBank employed 14,136 persons in 2017, down 4.69% when compared to the previous year. Historically, the bank's workforce hit an all time high of 14,979 persons in 2014 and an all time low of 956 in 2000. Average cost reached USD 2,353 per month per employee, ...

By Helgi Library - December 12, 2019

DenizBank's corporate loans reached TRY 88,364 mil in 2017, up 21.1% compared to the previous year. Turkish banking sector provided corporate loans of TRY 1,571 bil in 2017, up 22.5% when compared to the last year. DenizBank accounted for 5.94% of all cor...

By Helgi Library - June 25, 2018

DenizBank's corporate deposits reached TRY 45,692 mil in 2017, up 10.1% compared to the previous year. Turkish banking sector accepted corporate deposits of TRY 535 bil in 2017, up 18.4% when compared to the last year. DenizBank accounted for 8.54% of all...

By Helgi Library - June 25, 2018

DenizBank employed 14,136 persons in 2017, down 4.69% compared to the previous year. Historically, the bank's workforce hit an all time high of 14,979 persons in 2014 and an all time low of 5,059 in 2005. The bank operated a network of 740 branches and 5,6...

By Helgi Library - June 25, 2018

DenizBank's non-performing loans reached 3.55% of total loans at the end of 2017, down from 3.89% compared to the previous year. Historically, the NPL ratio hit an all time high of 12.3% in 2001 and an all time low of 2.17% in 2005. Provision coverage amoun...

By Helgi Library - June 25, 2018

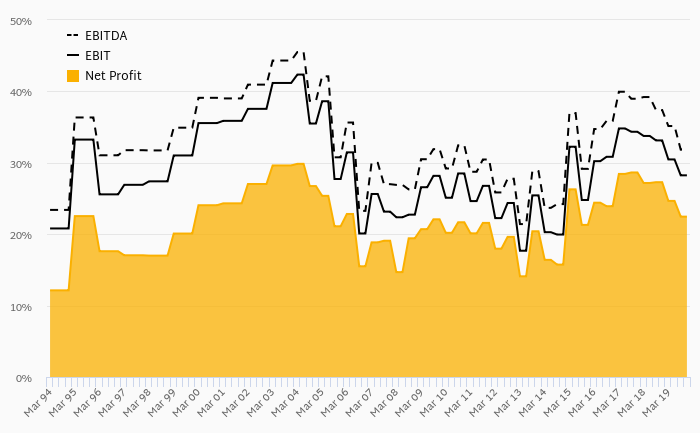

DenizBank generated total banking revenues of TRY 7,651 mil in 2017, up 16.7% compared to the previous year. Historically, the bank’s revenues containing of interest, fee and other non-interest income reached an all time high of TRY 7,651 mil in 2017 and an all...

By Helgi Library - June 25, 2018

DenizBank stock traded at TRY 3.67 per share at the end of 2017 implying a market capitalization of USD 3,217 mil. Since the end of 2012, the stock has depreciated by -67.4 % implying an annual average growth of -20.1 %. In absolute terms, the value of the company ...

By Helgi Library - June 25, 2018

DenizBank stock traded at TRY 3.67 per share at the end 2017 implying a market capitalization of USD 3,217 mil. Since the end of 2012, the stock has depreciated by -67.4 % implying an annual average growth of -20.1 %. In absolute terms, the value of the company f...

Denizbank AS (Denizbank) is a Turkey-based commercial bank. The Bank offers retail and commercial banking products and services, such as credit and debit cards, private and commercial loans, savings and checking accounts and money transfers, issuing letters of guarantee, foreign currency and non-cash loans and commercial loan deposit accounts, as well as portfolio management, mutual and pension fund management, international trade finance and securities brokerage. At the end of 2015, Denizbank Anonim Sirketi operated 734 branches in Turkey and 1 branch internationally. DenizBank was established in 1938 as a state-owned bank (Denizcilik Bankasi) to help finance the then emerging Turkish maritime industry. It is based in Istanbul, Turkey. Denizbank Anonim Sirketi operates as a subsidiary of Sberbank of Russia OJSC.

DenizBank has been growing its revenues and asset by 16.7% and 26.8% a year on average in the last 10 years. Its loans and deposits have grown by 26.9% and 29.2% a year during that time and loans to deposits ratio reached 99.1% at the end of 2017. The company achieved an average return on equity of 17.3% in the last decade with net profit growing 24.6% a year on average. In terms of operating efficiency, its cost to income ratio reached 42.0% in 2017, compared to 49.3% average in the last decade.

Equity represented 8.01% of total assets or 11.6% of loans at the end of 2017. DenizBank's non-performing loans were 3.55% of total loans while provisions covered some 77.7% of NPLs at the end of 2017.

DenizBank stock traded at TRY 3.67 per share at the end of 2017 resulting in a market capitalization of USD 3,217 mil. Over the previous five years, stock price fell by 67.40000000000001% or 20.1% a year on average. That’s compared to an average ROE of 14.7% the bank generated for its shareholders. This closing price put stock at a 12-month trailing price to earnings (PE) of 6.40x and price to book value (PBV) of 0.947x in 2017.

Helgi Library

Helgi Library