By Helgi Library - June 25, 2018

Odea Bank's non-performing loans reached 17.6% of total loans at the end of 2017, up from 9.07% compared to the previous year. ...

By Helgi Library - June 25, 2018

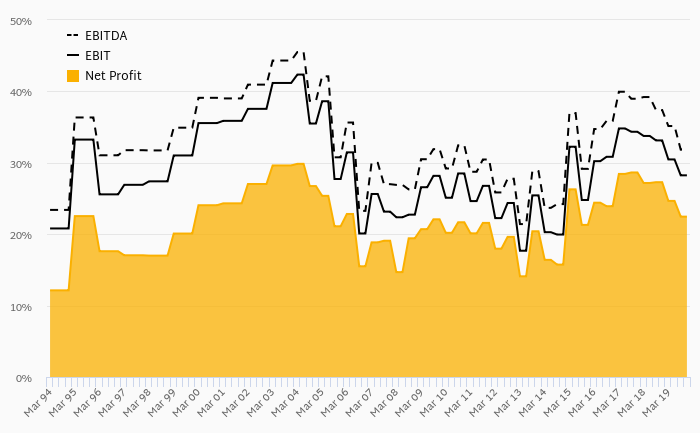

Odea Bank made a net profit of TRY 310 mil in 2017, up 69.5% compared to the previous year. This implies a return on equity of 8...

By Helgi Library - June 25, 2018

Odea Bank's net interest margin amounted to 3.69% in 2017, up from 2.99% compared to the previous year. Historically, the ...

| Profit Statement | 2015 | 2016 | 2017 | |

| Net Interest Income | TRY mil | 878 | 1,052 | 1,316 |

| Net Fee Income | TRY mil | 88.7 | 96.2 | 151 |

| Other Income | TRY mil | -189 | 179 | -21.4 |

| Total Revenues | TRY mil | 778 | 1,327 | 1,445 |

| Staff Cost | TRY mil | 226 | 259 | 297 |

| Operating Profit | TRY mil | 299 | 727 | 731 |

| Provisions | TRY mil | 233 | 485 | 342 |

| Net Profit | TRY mil | 45.2 | 183 | 310 |

| Balance Sheet | 2015 | 2016 | 2017 | |

| Interbank Loans | TRY mil | 4,097 | 4,531 | 3,030 |

| Customer Loans | TRY mil | 21,807 | 26,448 | 22,632 |

| Total Assets | TRY mil | 32,083 | 38,278 | 33,104 |

| Shareholders' Equity | TRY mil | 1,347 | 3,443 | 3,758 |

| Interbank Borrowing | TRY mil | 156 | 232 | 0 |

| Customer Deposits | TRY mil | 25,334 | 29,254 | 23,910 |

| Issued Debt Securities | TRY mil | 1,465 | 528 | 1,175 |

| Ratios | 2015 | 2016 | 2017 | |

| ROE | % | 3.37 | 7.64 | 8.62 |

| ROA | % | 0.157 | 0.520 | 0.870 |

| Costs (As % Of Assets) | % | 1.66 | 1.71 | 2.00 |

| Costs (As % Of Income) | % | 61.6 | 45.2 | 49.4 |

| Capital Adequacy Ratio | % | 12.2 | 15.0 | 20.3 |

| Net Interest Margin | % | 3.04 | 2.99 | 3.69 |

| Loans (As % Of Deposits) | % | 86.1 | 90.4 | 94.7 |

| NPLs (As % Of Loans) | % | 6.46 | 9.07 | 17.6 |

| Provisions (As % Of NPLs) | % | 38.6 | 43.8 | 41.4 |

| Growth Rates | 2015 | 2016 | 2017 | |

| Total Revenue Growth | % | 36.8 | 70.6 | 8.91 |

| Operating Cost Growth | % | 22.7 | 25.3 | 19.0 |

| Operating Profit Growth | % | 67.5 | 143 | 0.559 |

| Net Profit Growth | % | 13,415 | 305 | 69.5 |

| Customer Loan Growth | % | 21.1 | 21.3 | -14.4 |

| Total Asset Growth | % | 25.2 | 19.3 | -13.5 |

| Customer Deposit Growth | % | 20.3 | 15.5 | -18.3 |

| Shareholders' Equity Growth | % | 0.739 | 156 | 9.14 |

| Employees | 1,538 | 1,681 | 1,800 | |

Get all company financials in excel:

| summary | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | |||||||

| Net Interest Income | TRY mil | 32.0 | 124 | 559 | 878 | ||

| Total Revenues | TRY mil | 62.6 | 170 | 569 | 778 | ||

| Operating Profit | TRY mil | -1.26 | -63.4 | 178 | 299 | ||

| Net Profit | TRY mil | -19.8 | -123 | 0.335 | 45.2 | ||

| balance sheet | |||||||

| Interbank Loans | TRY mil | 389 | 1,160 | 3,248 | 4,097 | ||

| Customer Loans | TRY mil | 1,732 | 11,345 | 18,012 | 21,807 | ||

| Debt Securities | TRY mil | 1,023 | 1,518 | 1,166 | 1,486 | ||

| Total Assets | TRY mil | 3,634 | 16,110 | 25,622 | 32,083 | ||

| Shareholders' Equity | TRY mil | 514 | 1,331 | 1,337 | 1,347 | ||

| Interbank Borrowing | TRY mil | 0 | 223 | 139 | 156 | ||

| Customer Deposits | TRY mil | 2,517 | 12,372 | 21,061 | 25,334 | ||

| Issued Debt Securities | TRY mil | 725 | 2,580 | 1,190 | 1,465 | ||

| ratios | |||||||

| ROE | % | -3.86 | -13.3 | 0.025 | 3.37 | ||

| ROA | % | -0.545 | -1.24 | 0.002 | 0.157 | ||

| Costs (As % Of Assets) | % | 1.76 | 2.36 | 1.87 | 1.66 | ||

| Costs (As % Of Income) | % | 102 | 137 | 68.6 | 61.6 | ||

| Capital Adequacy Ratio | % | 36.4 | 15.6 | 13.7 | 12.2 | ||

| Net Interest Margin | % | 0.881 | 1.25 | 2.68 | 3.04 | ||

| Interest Income (As % Of Revenues) | % | 51.2 | 72.8 | 98.3 | 113 | ||

| Fee Income (As % Of Revenues) | % | 8.54 | 3.75 | 7.18 | 11.4 | ||

| Staff Cost (As % Of Total Cost) | % | 43.5 | 35.9 | 36.5 | 47.3 | ||

| Equity (As % Of Assets) | % | 14.1 | 8.26 | 5.22 | 4.20 | ||

| Loans (As % Of Deposits) | % | 68.8 | 91.7 | 85.5 | 86.1 | ||

| Loans (As % Assets) | % | 47.7 | 70.4 | 70.3 | 68.0 | ||

| NPLs (As % Of Loans) | % | 0 | 0.875 | 3.41 | 6.46 | ||

| Provisions (As % Of NPLs) | % | ... | 19.0 | 40.7 | 38.6 | ||

| valuation | |||||||

| Book Value Per Share Growth | % | ... | 287 | 352 | 57.0 |

| income statement | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | |||||||

| Interest Income | TRY mil | 44.7 | 603 | 1,579 | 2,115 | ||

| Interest Cost | TRY mil | 12.7 | 479 | 1,020 | 1,237 | ||

| Net Interest Income | TRY mil | 32.0 | 124 | 559 | 878 | ||

| Net Fee Income | TRY mil | 5.35 | 6.37 | 40.8 | 88.7 | ||

| Other Income | TRY mil | 25.2 | 39.9 | -31.3 | -189 | ||

| Total Revenues | TRY mil | 62.6 | 170 | 569 | 778 | ||

| Staff Cost | TRY mil | 27.8 | 83.7 | 142 | 226 | ||

| Operating Cost | TRY mil | 63.9 | 233 | 390 | 479 | ||

| Operating Profit | TRY mil | -1.26 | -63.4 | 178 | 299 | ||

| Provisions | TRY mil | 18.7 | 73.6 | 162 | 233 | ||

| Extra and Other Cost | TRY mil | 0 | 0 | < -0.001 | < -0.001 | ||

| Pre-Tax Profit | TRY mil | -20.0 | -137 | 16.7 | 66.5 | ||

| Tax | TRY mil | -0.163 | -14.3 | 16.3 | 21.3 | ||

| Net Profit | TRY mil | -19.8 | -123 | 0.335 | 45.2 | ||

| growth rates | |||||||

| Net Interest Income Growth | % | ... | 287 | 352 | 57.0 | ||

| Net Fee Income Growth | % | ... | 19.1 | 541 | 117 | ||

| Total Revenue Growth | % | ... | 172 | 234 | 36.8 | ||

| Operating Cost Growth | % | ... | 265 | 67.2 | 22.7 | ||

| Operating Profit Growth | % | ... | 4,930 | -382 | 67.5 | ||

| Pre-Tax Profit Growth | % | ... | 585 | -112 | 299 | ||

| Net Profit Growth | % | ... | 519 | -100 | 13,415 | ||

| market share | |||||||

| Market Share in Revenues | % | 0.086 | 0.211 | 0.639 | 0.784 | ... | |

| Market Share in Net Profit | % | ... | ... | 0.001 | 0.176 | ... | |

| Market Share in Employees | % | 0.213 | 0.560 | 0.691 | 0.764 | ||

| Market Share in Branches | % | 0.059 | 0.336 | 0.428 | 0.491 | ... |

| balance sheet | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| balance sheet | |||||||

| Cash | TRY mil | 411 | 1,794 | 2,831 | 4,075 | ||

| Interbank Loans | TRY mil | 389 | 1,160 | 3,248 | 4,097 | ||

| Customer Loans | TRY mil | 1,732 | 11,345 | 18,012 | 21,807 | ||

| Debt Securities | TRY mil | 1,023 | 1,518 | 1,166 | 1,486 | ||

| Fixed Assets | TRY mil | ... | ... | 174 | 242 | ||

| Total Assets | TRY mil | 3,634 | 16,110 | 25,622 | 32,083 | ||

| Shareholders' Equity | TRY mil | 514 | 1,331 | 1,337 | 1,347 | ||

| Liabilities | TRY mil | 3,120 | 14,779 | 24,285 | 30,736 | ||

| Interbank Borrowing | TRY mil | 0 | 223 | 139 | 156 | ||

| Customer Deposits | TRY mil | 2,517 | 12,372 | 21,061 | 25,334 | ||

| Issued Debt Securities | TRY mil | 725 | 2,580 | 1,190 | 1,465 | ||

| Other Liabilities | TRY mil | -121 | -396 | 1,894 | 3,781 | ||

| asset quality | |||||||

| Non-Performing Loans | TRY mil | 0 | 46.6 | 265 | 487 | ||

| Gross Loans | TRY mil | 974 | 5,329 | 7,787 | 7,538 | ||

| Total Provisions | TRY mil | 0 | 8.84 | 108 | 188 | ||

| growth rates | |||||||

| Customer Loan Growth | % | ... | 555 | 58.8 | 21.1 | ||

| Total Asset Growth | % | ... | 343 | 59.0 | 25.2 | ||

| Shareholders' Equity Growth | % | ... | 159 | 0.468 | 0.739 | ||

| Customer Deposit Growth | % | ... | 392 | 70.2 | 20.3 | ||

| market share | |||||||

| Market Share in Customer Loans | % | 0.236 | 1.17 | 1.57 | 1.58 | ||

| Market Share in Total Assets | % | 0.280 | 0.985 | 1.36 | 1.43 | ||

| Market Share in Customer Deposits | % | 0.347 | 1.38 | 2.11 | 2.16 |

| ratios | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| ratios | |||||||

| ROE | % | -3.86 | -13.3 | 0.025 | 3.37 | ||

| ROA | % | -0.545 | -1.24 | 0.002 | 0.157 | ||

| Costs (As % Of Assets) | % | 1.76 | 2.36 | 1.87 | 1.66 | ||

| Costs (As % Of Income) | % | 102 | 137 | 68.6 | 61.6 | ||

| Capital Adequacy Ratio | % | 36.4 | 15.6 | 13.7 | 12.2 | ||

| Tier 1 Ratio | % | ... | ... | ... | ... | ||

| Net Interest Margin | % | 0.881 | 1.25 | 2.68 | 3.04 | ||

| Interest Spread | % | ... | 0.754 | 2.35 | 2.83 | ||

| Asset Yield | % | 1.23 | 6.10 | 7.57 | 7.33 | ||

| Cost Of Liabilities | % | ... | 5.35 | 5.22 | 4.50 | ||

| Interest Income (As % Of Revenues) | % | 51.2 | 72.8 | 98.3 | 113 | ||

| Fee Income (As % Of Revenues) | % | 8.54 | 3.75 | 7.18 | 11.4 | ||

| Other Income (As % Of Revenues) | % | 40.3 | 23.4 | -5.50 | -24.2 | ||

| Cost Per Employee | USD per month | 3,251 | 3,312 | 3,807 | 4,674 | ||

| Cost Per Employee (Local Currency) | TRY per month | 5,852 | 6,315 | 8,541 | 12,262 | ||

| Staff Cost (As % Of Total Cost) | % | 43.5 | 35.9 | 36.5 | 47.3 | ||

| Equity (As % Of Assets) | % | 14.1 | 8.26 | 5.22 | 4.20 | ||

| Loans (As % Of Deposits) | % | 68.8 | 91.7 | 85.5 | 86.1 | ||

| Loans (As % Assets) | % | 47.7 | 70.4 | 70.3 | 68.0 | ||

| NPLs (As % Of Loans) | % | 0 | 0.875 | 3.41 | 6.46 | ||

| Provisions (As % Of NPLs) | % | ... | 19.0 | 40.7 | 38.6 | ||

| Provisions (As % Of Loans) | % | 0 | 0.078 | 0.600 | 0.862 | ||

| Cost of Provisions (As % Of Loans) | % | 1.08 | 1.13 | 1.10 | 1.17 |

Get all company financials in excel:

By Helgi Library - December 12, 2019

Odea Bank's customer loans reached TRY 22,632 mil in 2017, down 14.4% compared to the previous year. Turkish banking sector provided customer loans of TRY 2,209 bil in 2017, up 20.6% when compared to the last year. Odea Bank accounted for 1.16% of all cus...

By Helgi Library - December 12, 2019

Odea Bank's customer deposits reached TRY 23,910 mil in 2017, down 18.3% compared to the previous year. Turkish banking sector accepted customer deposits of TRY 1,670 bil in 2017, up 17.8% when compared to the last year. Odea Bank accounted for 1.48% of a...

By Helgi Library - June 25, 2018

Odea Bank generated total banking revenues of TRY 1,445 mil in 2017, up 8.91% compared to the previous year. Historically, the bank’s revenues containing of interest, fee and other non-interest income reached an all time high of TRY 1,445 mil in 2017 and an all...

By Helgi Library - June 25, 2018

Odea Bank's customer loan growth reached -14.4% in 2017, down from 21.3% compared to the previous year. Historically, the bank’s loans growth reached an all time high of 555% in 2013 and an all time low of -14.4% in 2017. In the last decade, the average a...

By Helgi Library - July 16, 2018

Odea Bank generated total banking revenues of TRY 1,327 mil in 2016, up 70.6% compared to the previous year. Turkish banking sector banking sector generated total revenues of TRY 121,108 mil in 2016, up 22.1% when compared to the last year. As a...

By Helgi Library - June 25, 2018

Odea Bank employed 1,681 persons in 2016, up 9.30% when compared to the previous year. Historically, the bank's workforce hit an all time high of 1,681 persons in 2016 and an all time low of 396 in 2012. Average cost reached USD 3,993 per month per employee, ...

By Helgi Library - June 25, 2018

Odea Bank's cost to income ratio reached 45.2% in 2016, down from 61.6% compared to the previous year. Historically, the bank’s costs reached an all time high of 137% of income in 2013 and an all time low of 45.2% in 2016. When compared to total assets, ba...

Odea Bank has been growing its revenues and asset by 36.5% and 8.92% a year on average in the last 3 years. Its loans and deposits have grown by 7.91% and 4.32% a year during that time and loans to deposits ratio reached 94.7% at the end of 2017. The company achieved an average return on equity of 6.54% in the last three years with net profit growing 875% a year on average. In terms of operating efficiency, its cost to income ratio reached 49.4% in 2017, compared to 52.1% average in the last three years.

Equity represented 11.4% of total assets or 16.6% of loans at the end of 2017. Odea Bank's non-performing loans were 17.6% of total loans while provisions covered some 41.4% of NPLs at the end of 2017.

Helgi Library

Helgi Library