By Helgi Library - May 22, 2018

Idea Bank's customer loans reached PLN 16,279 mil in 2017, up 49.7% compared to the previous year. Polish banking sector provid...

By Helgi Library - May 19, 2018

Idea Bank's non-performing loans reached 7.98% of total loans at the end of 2017, up from 7.86% compared to the previous year. ...

By Helgi Library - May 22, 2018

Idea Bank's customer deposits reached PLN 17,508 mil in 2017, up 16.0% compared to the previous year. Polish banking sector acc...

| Profit Statement | 2015 | 2016 | 2017 | |

| Net Interest Income | PLN mil | 384 | 624 | 681 |

| Net Fee Income | PLN mil | 388 | 342 | 311 |

| Other Income | PLN mil | 20.3 | 196 | 161 |

| Total Revenues | PLN mil | 792 | 1,162 | 1,154 |

| Staff Cost | PLN mil | 227 | 233 | 232 |

| Operating Profit | PLN mil | 105 | 451 | 321 |

| Provisions | PLN mil | 163 | 170 | 290 |

| Net Profit | PLN mil | 312 | 441 | 231 |

| Balance Sheet | 2015 | 2016 | 2017 | |

| Interbank Loans | PLN mil | 264 | 290 | 192 |

| Customer Loans | PLN mil | 8,799 | 10,873 | 16,279 |

| Total Assets | PLN mil | 18,858 | 21,517 | 23,954 |

| Shareholders' Equity | PLN mil | 2,055 | 2,457 | 2,735 |

| Interbank Borrowing | PLN mil | 529 | 2,126 | 1,990 |

| Customer Deposits | PLN mil | 13,017 | 15,091 | 17,508 |

| Issued Debt Securities | PLN mil | 669 | 482 | 522 |

| Ratios | 2015 | 2016 | 2017 | |

| ROE | % | 17.7 | 19.5 | 8.89 |

| ROA | % | 1.84 | 2.18 | 1.02 |

| Costs (As % Of Assets) | % | 3.04 | 2.68 | 2.39 |

| Costs (As % Of Income) | % | 65.1 | 46.6 | 47.0 |

| Capital Adequacy Ratio | % | 14.9 | 14.4 | 14.0 |

| Net Interest Margin | % | 2.26 | 3.09 | 3.00 |

| Loans (As % Of Deposits) | % | 67.6 | 72.1 | 93.0 |

| NPLs (As % Of Loans) | % | 6.09 | 7.86 | 7.98 |

| Provisions (As % Of NPLs) | % | 42.7 | 38.9 | 41.4 |

| Growth Rates | 2015 | 2016 | 2017 | |

| Total Revenue Growth | % | 1.51 | 46.7 | -0.691 |

| Operating Cost Growth | % | 12.9 | 4.87 | 0.360 |

| Operating Profit Growth | % | -60.1 | 331 | -28.9 |

| Net Profit Growth | % | 29.4 | 41.3 | -47.7 |

| Customer Loan Growth | % | 28.5 | 23.6 | 49.7 |

| Total Asset Growth | % | 25.2 | 14.1 | 11.3 |

| Customer Deposit Growth | % | 19.6 | 15.9 | 16.0 |

| Shareholders' Equity Growth | % | 39.2 | 19.6 | 11.3 |

Get all company financials in excel:

| summary | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | |||||||

| Net Interest Income | PLN mil | 100 | 198 | 337 | 384 | ||

| Total Revenues | PLN mil | 246 | 465 | 780 | 792 | ||

| Operating Profit | PLN mil | -22.0 | 74.1 | 263 | 105 | ||

| Net Profit | PLN mil | 23.6 | 104 | 241 | 312 | ||

| balance sheet | |||||||

| Interbank Loans | PLN mil | 228 | 99.5 | 511 | 264 | ||

| Customer Loans | PLN mil | 3,145 | 4,416 | 6,845 | 8,799 | ||

| Debt Securities | PLN mil | 651 | 968 | 2,139 | 2,895 | ||

| Total Assets | PLN mil | 5,201 | 7,393 | 15,064 | 18,858 | ||

| Shareholders' Equity | PLN mil | 676 | 771 | 1,476 | 2,055 | ||

| Interbank Borrowing | PLN mil | 358 | 634 | 660 | 529 | ||

| Customer Deposits | PLN mil | 3,890 | 5,498 | 10,881 | 13,017 | ||

| Issued Debt Securities | PLN mil | 136 | 248 | 1,055 | 669 | ||

| ratios | |||||||

| ROE | % | 3.48 | 14.4 | 21.5 | 17.7 | ||

| ROA | % | 0.453 | 1.65 | 2.15 | 1.84 | ||

| Costs (As % Of Assets) | % | 5.03 | 5.26 | 4.07 | 3.04 | ||

| Costs (As % Of Income) | % | 106 | 71.2 | 58.6 | 65.1 | ||

| Capital Adequacy Ratio | % | 11.8 | 11.9 | 13.5 | 14.9 | ||

| Net Interest Margin | % | 1.92 | 3.15 | 3.00 | 2.26 | ||

| Interest Income (As % Of Revenues) | % | 40.6 | 42.7 | 43.2 | 48.5 | ||

| Fee Income (As % Of Revenues) | % | 58.0 | 52.6 | 41.3 | 49.0 | ||

| Staff Cost (As % Of Total Cost) | % | 48.5 | 47.1 | 45.3 | 44.0 | ||

| Equity (As % Of Assets) | % | 13.0 | 10.4 | 9.80 | 10.9 | ||

| Loans (As % Of Deposits) | % | 80.8 | 80.3 | 62.9 | 67.6 | ||

| Loans (As % Assets) | % | 60.5 | 59.7 | 45.4 | 46.7 | ||

| NPLs (As % Of Loans) | % | 3.46 | 5.88 | 6.91 | 6.09 | ||

| Provisions (As % Of NPLs) | % | 79.0 | 61.5 | 57.6 | 42.7 | ||

| valuation | |||||||

| Number Of Shares (Average) | mil | 48.5 | 48.5 | 67.8 | 78.4 | ||

| Earnings Per Share (EPS) | 0.486 | 2.15 | 3.56 | 3.98 | |||

| Book Value Per Share | 14.0 | 15.9 | 21.8 | 26.2 | |||

| Earnings Per Share Growth | % | ... | 342 | 65.6 | 11.9 | ||

| Book Value Per Share Growth | % | ... | 14.0 | 36.8 | 20.4 |

| income statement | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| income statement | |||||||

| Interest Income | PLN mil | 288 | 457 | 689 | 803 | ||

| Interest Cost | PLN mil | 188 | 258 | 353 | 419 | ||

| Net Interest Income | PLN mil | 100 | 198 | 337 | 384 | ||

| Net Fee Income | PLN mil | 143 | 245 | 322 | 388 | ||

| Other Income | PLN mil | 3.30 | 22.1 | 121 | 20.3 | ||

| Total Revenues | PLN mil | 246 | 465 | 780 | 792 | ||

| Staff Cost | PLN mil | 127 | 156 | 207 | 227 | ||

| Depreciation | PLN mil | 19.6 | 34.3 | 39.2 | 49.1 | ||

| Other Cost | PLN mil | 115 | 141 | 211 | 240 | ||

| Operating Cost | PLN mil | 261 | 331 | 457 | 516 | ||

| Operating Profit | PLN mil | -22.0 | 74.1 | 263 | 105 | ||

| Provisions | PLN mil | 6.84 | 60.0 | 103 | 163 | ||

| Extra and Other Cost | PLN mil | -6.84 | -60.0 | -70.0 | -163 | ||

| Pre-Tax Profit | PLN mil | -22.0 | 74.1 | 230 | 105 | ||

| Tax | PLN mil | -48.9 | -30.1 | 15.5 | -89.3 | ||

| Minorities | PLN mil | 3.28 | 0 | 0 | 0 | ||

| Net Profit | PLN mil | 23.6 | 104 | 241 | 312 | ||

| growth rates | |||||||

| Net Interest Income Growth | % | ... | 98.4 | 69.7 | 14.0 | ||

| Net Fee Income Growth | % | ... | 71.1 | 31.7 | 20.4 | ||

| Total Revenue Growth | % | ... | 88.9 | 67.8 | 1.51 | ||

| Operating Cost Growth | % | ... | 26.6 | 38.0 | 12.9 | ||

| Operating Profit Growth | % | ... | -436 | 254 | -60.1 | ||

| Pre-Tax Profit Growth | % | ... | -436 | 210 | -54.4 | ||

| Net Profit Growth | % | ... | 342 | 132 | 29.4 | ||

| market share | |||||||

| Market Share in Revenues | % | 0.421 | 0.839 | 1.35 | 1.42 | ||

| Market Share in Net Profit | % | 0.152 | 0.686 | 1.52 | 2.79 |

| balance sheet | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| balance sheet | |||||||

| Cash | PLN mil | 91.4 | 170 | 436 | 600 | ||

| Interbank Loans | PLN mil | 228 | 99.5 | 511 | 264 | ||

| Customer Loans | PLN mil | 3,145 | 4,416 | 6,845 | 8,799 | ||

| Debt Securities | PLN mil | 651 | 968 | 2,139 | 2,895 | ||

| Fixed Assets | PLN mil | 286 | 319 | 1,046 | 778 | ||

| Total Assets | PLN mil | 5,201 | 7,393 | 15,064 | 18,858 | ||

| Shareholders' Equity | PLN mil | 676 | 771 | 1,476 | 2,055 | ||

| Of Which Minority Interest | PLN mil | 0 | 0 | 0 | 0 | ||

| Liabilities | PLN mil | 4,525 | 6,622 | 13,588 | 16,803 | ||

| Interbank Borrowing | PLN mil | 358 | 634 | 660 | 529 | ||

| Customer Deposits | PLN mil | 3,890 | 5,498 | 10,881 | 13,017 | ||

| Issued Debt Securities | PLN mil | 136 | 248 | 1,055 | 669 | ||

| Other Liabilities | PLN mil | 141 | 242 | 991 | 2,587 | ||

| asset quality | |||||||

| Non-Performing Loans | PLN mil | 112 | 269 | 493 | 551 | ||

| Gross Loans | PLN mil | 3,233 | 4,582 | 7,129 | 9,034 | ||

| Total Provisions | PLN mil | 88.5 | 166 | 284 | 235 | ||

| growth rates | |||||||

| Customer Loan Growth | % | ... | 40.4 | 55.0 | 28.5 | ||

| Total Asset Growth | % | ... | 42.1 | 104 | 25.2 | ||

| Shareholders' Equity Growth | % | ... | 14.0 | 91.4 | 39.2 | ||

| Customer Deposit Growth | % | ... | 41.3 | 97.9 | 19.6 | ||

| market share | |||||||

| Market Share in Customer Loans | % | 0.337 | 0.455 | 0.658 | 0.790 | ||

| Market Share in Total Assets | % | 0.395 | 0.539 | 1.01 | 1.21 | ||

| Market Share in Customer Deposits | % | 0.420 | 0.564 | 1.05 | 1.17 |

| ratios | Unit | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 |

| ratios | |||||||

| ROE | % | 3.48 | 14.4 | 21.5 | 17.7 | ||

| ROA | % | 0.453 | 1.65 | 2.15 | 1.84 | ||

| Costs (As % Of Assets) | % | 5.03 | 5.26 | 4.07 | 3.04 | ||

| Costs (As % Of Income) | % | 106 | 71.2 | 58.6 | 65.1 | ||

| Capital Adequacy Ratio | % | 11.8 | 11.9 | 13.5 | 14.9 | ||

| Tier 1 Ratio | % | 11.8 | 11.9 | 13.5 | 11.1 | ||

| Net Interest Margin | % | 1.92 | 3.15 | 3.00 | 2.26 | ||

| Interest Spread | % | ... | 2.62 | 2.65 | 1.98 | ||

| Asset Yield | % | 5.53 | 7.25 | 6.14 | 4.74 | ||

| Cost Of Liabilities | % | ... | 4.64 | 3.49 | 2.76 | ||

| Interest Income (As % Of Revenues) | % | 40.6 | 42.7 | 43.2 | 48.5 | ||

| Fee Income (As % Of Revenues) | % | 58.0 | 52.6 | 41.3 | 49.0 | ||

| Other Income (As % Of Revenues) | % | 1.34 | 4.76 | 15.5 | 2.56 | ||

| Staff Cost (As % Of Total Cost) | % | 48.5 | 47.1 | 45.3 | 44.0 | ||

| Equity (As % Of Assets) | % | 13.0 | 10.4 | 9.80 | 10.9 | ||

| Loans (As % Of Deposits) | % | 80.8 | 80.3 | 62.9 | 67.6 | ||

| Loans (As % Assets) | % | 60.5 | 59.7 | 45.4 | 46.7 | ||

| NPLs (As % Of Loans) | % | 3.46 | 5.88 | 6.91 | 6.09 | ||

| Provisions (As % Of NPLs) | % | 79.0 | 61.5 | 57.6 | 42.7 | ||

| Provisions (As % Of Loans) | % | 2.81 | 3.75 | 4.15 | 2.67 | ||

| Cost of Provisions (As % Of Loans) | % | 0.218 | 1.59 | 1.83 | 2.08 |

Get all company financials in excel:

By Helgi Library - May 22, 2018

Idea Bank generated total banking revenues of PLN 1,154 mil in 2017, down 0.691% compared to the previous year. Polish banking sector banking sector generated total revenues of PLN 61,763 mil in 2017, up 4.13% when compared to the last year. As ...

By Helgi Library - May 19, 2018

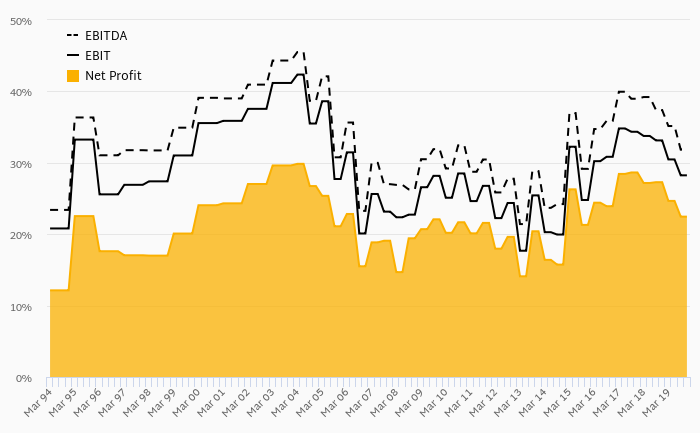

Idea Bank made a net profit of PLN 231 mil in 2017, down 47.7% compared to the previous year. This implies a return on equity of 8.89%. Historically, the bank’s net profit reached an all time high of PLN 441 mil in 2016 and an all time low of PLN 23.6 mil i...

By Helgi Library - May 19, 2018

Idea Bank's net interest margin amounted to 3.00% in 2017, down from 3.09% compared to the previous year. Historically, the bank’s net interest margin reached an all time high of 3.15% in 2013 and an all time low of 2.26% in 2015. The average margin in ...

By Helgi Library - May 19, 2018

Idea Bank generated total banking revenues of PLN 1,154 mil in 2017, down 0.691% compared to the previous year. Historically, the bank’s revenues containing of interest, fee and other non-interest income reached an all time high of PLN 1,162 mil in 2016 and an ...

By Helgi Library - May 19, 2018

Idea Bank's capital adequacy ratio reached 14.0% at the end of 2017, down from 14.4% compared to the previous year. Historically, the bank’s capital ratio hit an all time high of 14.9% in 2015 and an all time low of 11.8% in 2012. The Tier 1 ratio amounted to...

By Helgi Library - May 19, 2018

Idea Bank's customer loan growth reached 49.7% in 2017, up from 23.6% compared to the previous year. Historically, the bank’s loans growth reached an all time high of 55.0% in 2014 and an all time low of 23.6% in 2016. In the last decade, the average annu...

Idea Bank has been growing its revenues and asset by 36.2% and 35.7% a year on average in the last 5 years. Its loans and deposits have grown by 38.9% and 35.1% a year during that time and loans to deposits ratio reached 93.0% at the end of 2017. The company achieved an average return on equity of 16.4% in the last five years with net profit growing 57.8% a year on average. In terms of operating efficiency, its cost to income ratio reached 47.0% in 2017, compared to 57.7% average in the last five years.

Equity represented 11.4% of total assets or 16.8% of loans at the end of 2017. Idea Bank's non-performing loans were 7.98% of total loans while provisions covered some 41.4% of NPLs at the end of 2017.

Helgi Library

Helgi Library